- Prices reclaim $2,000/t amid cautious downstream demand

- Inventories jump sharply mid-week, limiting bullish momentum

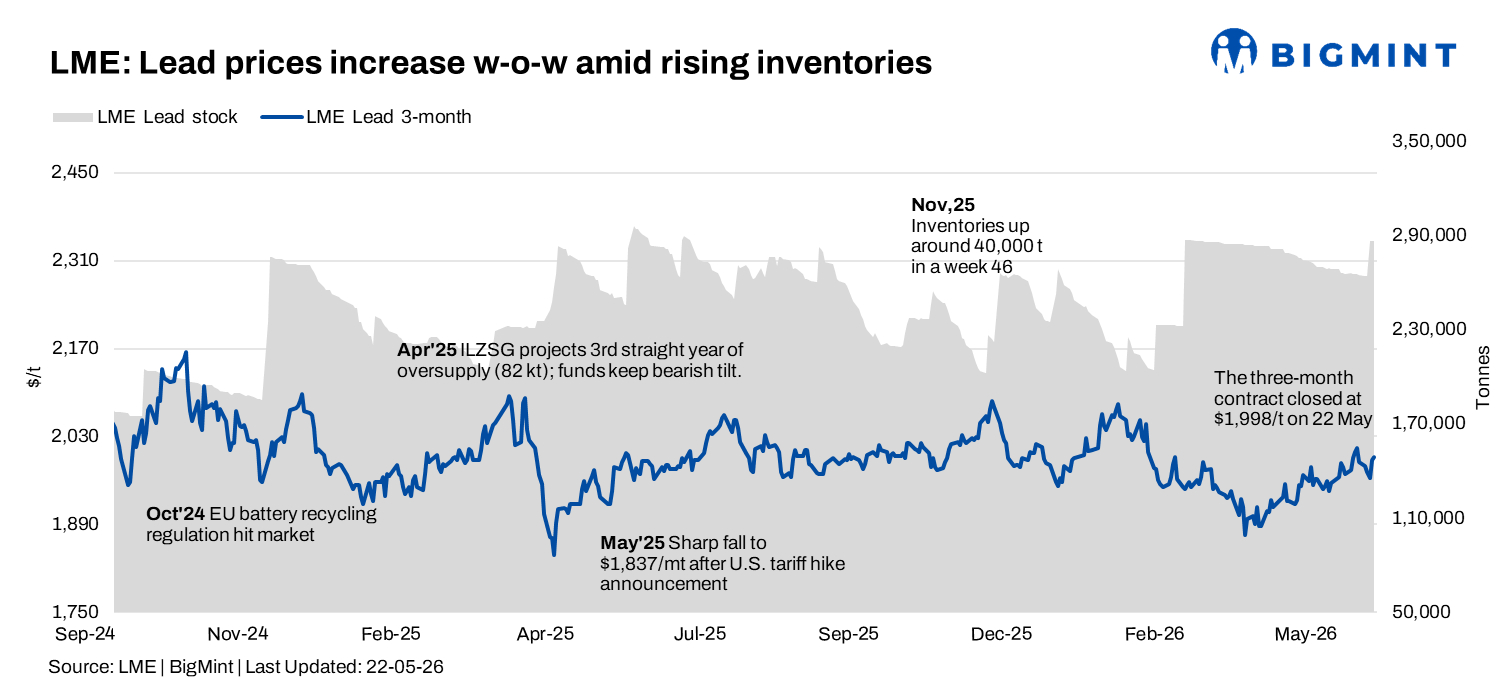

Lead prices on the London Metal Exchange (LME) moved higher during the week ended 22 May 2026, supported by improved sentiment across the broader base metals complex and renewed buying interest near lower levels. However, gains remained limited as a sharp increase in exchange inventories and cautious downstream demand weighed on overall market confidence.

Prices witnessed volatility during the week, initially weakening amid softer macro sentiment before recovering strongly towards the close as the market attempted to stabilise above the key $2,000/t mark.

Price trends

The LME three-month lead contract opened the week at $1,983/t on 18 May and traded under pressure during the first half of the week.

Prices declined to a weekly low of $1,964/t on 20 May amid cautious market sentiment and weaker buying activity. However, the contract recovered sharply in the latter half of the week, climbing to a high of $1,998/t on 22 May before closing near weekly highs.

LME cash lead prices also strengthened towards the weekend, rising from $1,995/t on 18 May to $2,006/t on 22 May, indicating improved spot market sentiment.

On a w-o-w basis, LME lead prices recorded marginal gains, although the broader market structure remained range-bound. Immediate resistance was observed near the psychological $2,000/t level, while support was seen around $1,960-1,965/t.

Inventory analysis

LME lead inventories remained largely stable during the initial part of the week before witnessing a sharp increase on 20 May.

Stocks rose significantly from 264,200 t on 19 May to 286,475 t on 20 May and remained unchanged through the rest of the week.

The substantial inventory build-up indicates improved material availability in exchange warehouses and may limit the scope for any aggressive upside in prices despite firmer market sentiment.

The sharp increase in inventories offset some of the supportive impact from recovering prices and highlighted that the global lead market remains adequately supplied overall.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices remained under pressure throughout the week, reflecting cautious sentiment in the Chinese market and subdued downstream demand.

SHFE lead prices declined from around $2,480/t on 18 May to $2,359/t on 22 May, marking a steady downward trend across the week.

The persistent weakness in Chinese lead prices suggests limited physical demand recovery and continued cautious buying activity despite fluctuations in global base metal sentiment.

MCX price movements

On the Multi Commodity Exchange (MCX), lead futures traded within a narrow range during the week and ended marginally higher.

The May 2026 lead contract opened at INR 202,450/t on 18 May and moved between a weekly low of INR 201,150/t on 20 May and a weekly high of INR 204,100/t on 22 May. The contract eventually closed at INR 202,750/t on 22 May.

Trading activity improved moderately towards the latter half of the week, while open interest continued to decline and stood at 116 lots on 22 May compared with 183 lots at the beginning of the week, indicating ongoing long unwinding and profit booking at higher levels.

Market participation remained cautious amid mixed global cues and inventory-related concerns.

Outlook

Lead prices are expected to remain range-bound in the near term, with immediate resistance seen around $2,000-2,010/t and support near $1,960/t.

While firmer sentiment across the broader base metals complex may continue to support prices, the sharp increase in LME inventories and subdued downstream demand are likely to cap significant upside momentum.

The overall trend is expected to remain stable to mildly positive, with market participants closely monitoring inventory movements, macroeconomic developments and demand recovery trends across key consuming regions.

Leave a Reply