- Petcoke demand remains largely opportunistic

- Freight volatility increases procurement caution

The global fuel-grade petroleum coke (petcoke) market remains under pressure, with prices extending losses for a fourth consecutive week as weakening demand from India’s cement sector weighs on buying sentiment.

Competitive thermal coal pricing, rising availability of US-origin coal and cautious procurement ahead of the monsoon have increasingly shifted the fuel preference of Indian cement producers away from petcoke, forcing suppliers to lower offers in an effort to revive demand.

The correction has become particularly visible in the Atlantic Basin, where increased spot availability from the US Gulf Coast (USGC), coupled with slower buying from India – the world’s largest petcoke importer – has pushed benchmark prices steadily lower.

USGC petcoke prices extend declines

Fuel-grade petcoke prices continued to soften during the week, with both high- and medium-sulphur grades under pressure as buyers resisted fresh bookings.

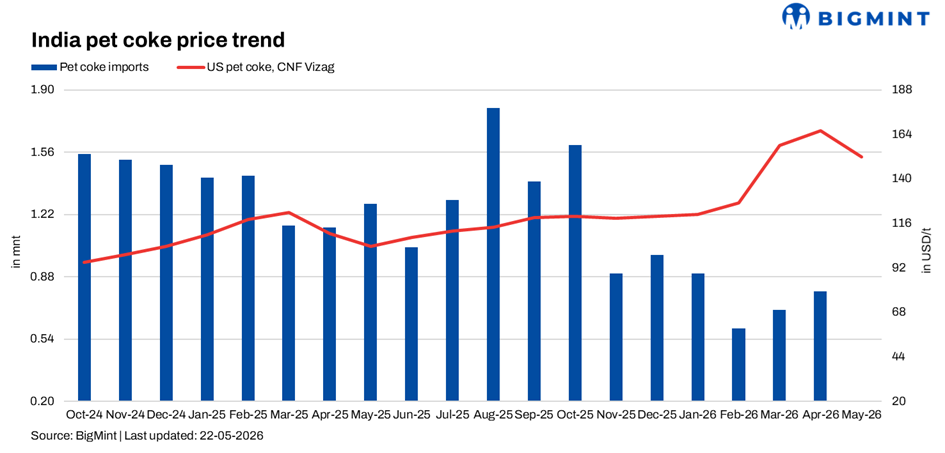

Global price snapshot

The weakness has been driven largely by muted Indian buying interest, with market participants noting that cement producers have increasingly shifted focus toward lower-cost thermal coal alternatives rather than replenishing petcoke inventories.

An increase in spot cargo availability from US refiners has further amplified bearish sentiment. The resumption of production at Valero’s Port Arthur refinery, following operational disruptions earlier this year, has brought additional material into the market, contributing to a softer supply-demand balance at a time when buying appetite remains subdued.

India emerges as key pressure point

India remains the single most important demand centre for fuel-grade petcoke, particularly from the cement sector. However, demand has become increasingly selective as buyers reassess fuel economics amid softening coal prices and growing availability of imported high-CV thermal coal.

Market participants indicated that Indian cement producers are no longer evaluating petcoke purely on headline pricing but on delivered calorific cost, where imported coal has begun to gain a measurable advantage.

At present, US Northern Appalachian (NAPP) thermal coal of around 6,900 NAR was heard trading in the mid-$130s/t CFR east coast India, with offers to west coast India in the low-to-mid $130s/t CFR range. By comparison, imported petcoke remains priced in the mid-to-high $140s/t CFR range, reducing its historical cost competitiveness.

Indicative delivered fuel economics

US NAPP coal continued offering comparatively better fuel economics for cement producers, with indicative CFR prices heard around $135-140/t for 6,900 NAR material, translating to nearly $19.4-19.8/GCal. In comparison, imported petcoke prices for 6.5-8.5% sulphur material were heard around $147-152/t CFR, with energy economics estimated near $20.2-20.6/GCal.

Although the overall cost difference remained relatively narrow, cement producers consuming large fuel volumes increasingly prioritised even marginal savings, especially where operational flexibility allowed substitution between coal and petcoke. Market participants reported that buying interest in petcoke largely shifted towards opportunistic purchases rather than systematic restocking. Several buyers maintained bids in the low-$140s/t CFR west coast India range, while sellers continued testing offers in the low-to-mid $150s/t range for US-origin material.

Cement producers become increasingly selective

Demand from Indian cement producers is present but highly price-sensitive.

Market participants said some buying activity continues for Oman-origin high-sulphur petcoke, with cargoes reportedly discussed in the $140-143/t CFR west coast India range, although trading activity remains sporadic rather than sustained.

At the same time, several cement producers are increasingly favouring thermal coal, particularly US NAPP coal and domestic Indian coal, as part of a broader strategy to contain fuel costs.

Domestic coal availability has also become a meaningful competitive factor, especially for inland cement plants where transportation economics often favour local supply over imported fuels. Buyers indicated that domestic coal remains available at relatively stable pricing, reducing urgency for imported petcoke procurement.

Market participants noted that there were at least four to five enquiries for NAPP coal during the week, particularly along India’s east coast, underscoring growing interest in imported thermal coal as an alternative fuel source.

Coal competition reshapes fuel landscape

The competitive challenge facing petcoke is no longer limited to price alone. Availability, logistics, freight predictability and blending flexibility are increasingly influencing procurement decisions.

Competing fuels in India’s cement sector

US NAPP coal continued gaining traction in India’s cement sector due to comparatively better calorific economics and rising enquiries from cement producers. Domestic coal also remained competitive for inland plants because of stable availability and lower pricing compared with imported fuels. Meanwhile, South African and Russian coal continued serving as alternative imported options, although volatile freight rates and fluctuating arbitrage opportunities kept buying activity cautious.

Petcoke was preferred for certain kiln configurations; however, its relative cost advantage weakened against imported and domestic coal. Market participants stated that volatility in shipping costs and broader geopolitical uncertainty increasingly influenced delivered fuel economics, making buyers more cautious towards imported fuel procurement and long-term commitments.

Petcoke to remain under pressure

The near-term outlook for petcoke remains cautious. With the southwest monsoon approaching and cement demand expected to moderate seasonally, buyers are likely to remain conservative in fresh procurement.

At the same time, comfortable fuel availability, competitive imported coal pricing and growing optionality between fuels are expected to limit any sharp rebound in petcoke demand over the coming weeks.

Suppliers may therefore face continued pressure to adjust offers lower in order to stimulate buying interest, particularly for 6.5% sulphur grades, which remain most exposed to competition from imported thermal coal.

For now, India’s cement sector appears increasingly focused on maintaining procurement flexibility, with coal – particularly US-origin high-CV material – steadily strengthening its position in the industrial fuel mix at petcoke’s expense.

Leave a Reply