- Softer Atlantic demand, weaker Australian loadings pressure exports

- Chinese restocking, firmer logistics support Indonesian cargo flows

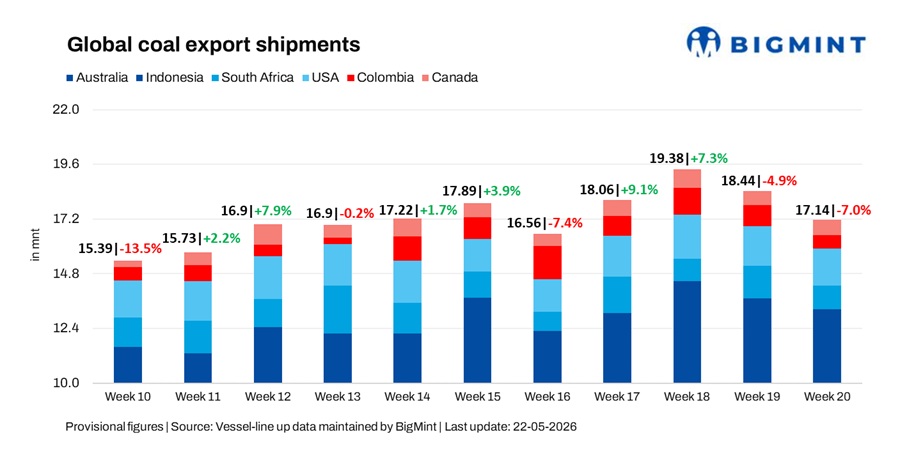

Global seaborne coal shipments fell 7% w-o-w to 17.14 million tonnes (mnt) in the week ended 15 May 2026, from 18.44 mnt a week earlier, according to BigMint data.

Lower exports from Australia, South Africa, Colombia and the USA weighed on overall volumes amid softer Atlantic demand and logistical constraints. However, stronger Indonesian and Canadian shipments partly offset the decline, supported by improved Asian enquiries, firmer terminal activity and better rail movements.

Country-wise trends

Port & shipper-wise trends

Pacific flows

- Australian shipments fell to 6.79 mnt, amid softer loadings at Newcastle (3.10 mnt), Gladstone (1.28 mnt) and DBCT (1.13 mnt). Japan (1.35 mnt) and China (1.06 mnt) remained the key destinations, while Glencore (0.64 mnt), Yancoal (0.55 mnt) and BHP (0.53 mnt) led shipments.

- Indonesian shipments rose to 6.44 mnt, supported by stronger Chinese demand and improved cargo flows. Taboneo (1.25 mnt) and Bunati (0.94 mnt) led exports, while China (1.78 mnt) and India (0.99 mnt) remained the key buyers.

- Canadian shipments increased to 0.67 mnt, supported by stronger west coast terminal activity and improved rail arrivals. Roberts Bank (0.51 mnt) dominated exports, while Japan (0.19 mnt) remained the key destination.

Atlantic flows

- South African shipments fell to 1.04 mnt amid lower RBCT throughput and rail constraints. Richards Bay dominated exports, while China (0.17 mnt) and Pakistan (0.12 mnt) remained key destinations.

- US shipments eased to 1.63 mnt amid cautious Atlantic enquiries and softer steel-sector demand. Norfolk (0.70 mnt), Baltimore (0.33 mnt) and Mobile (0.31 mnt) led exports, while Brazil (0.25 mnt) emerged as the key destination.

- Colombian shipments declined to 0.60 mnt. Puerto Nuevo (0.47 mnt) and Puerto Bolivar (0.13 mnt) led exports, while Carbosan (0.47 mnt) and Cerrejon Mines (0.13 mnt) supported supply. Brazil (0.14 mnt) remained the key destination.

Coal freights to India remain mixed

Coal freight rates to India remained mixed w-o-w. Pacific Panamax sentiment stayed firm on tighter prompt tonnage and steady cargo enquiries, while Atlantic sentiment remained subdued amid weak spot enquiries. Supramax rates were largely stable, though ample vessel availability capped upside on select routes.

Outlook

Global coal export flows are expected to remain mixed in the near term. Australian cargoes may stay under pressure amid cautious Asian buying and terminal maintenance, while Indonesian exports could remain supported by steady Chinese demand. South African shipments may continue facing rail and throughput constraints, though any recovery in Atlantic demand could support flows.

Leave a Reply