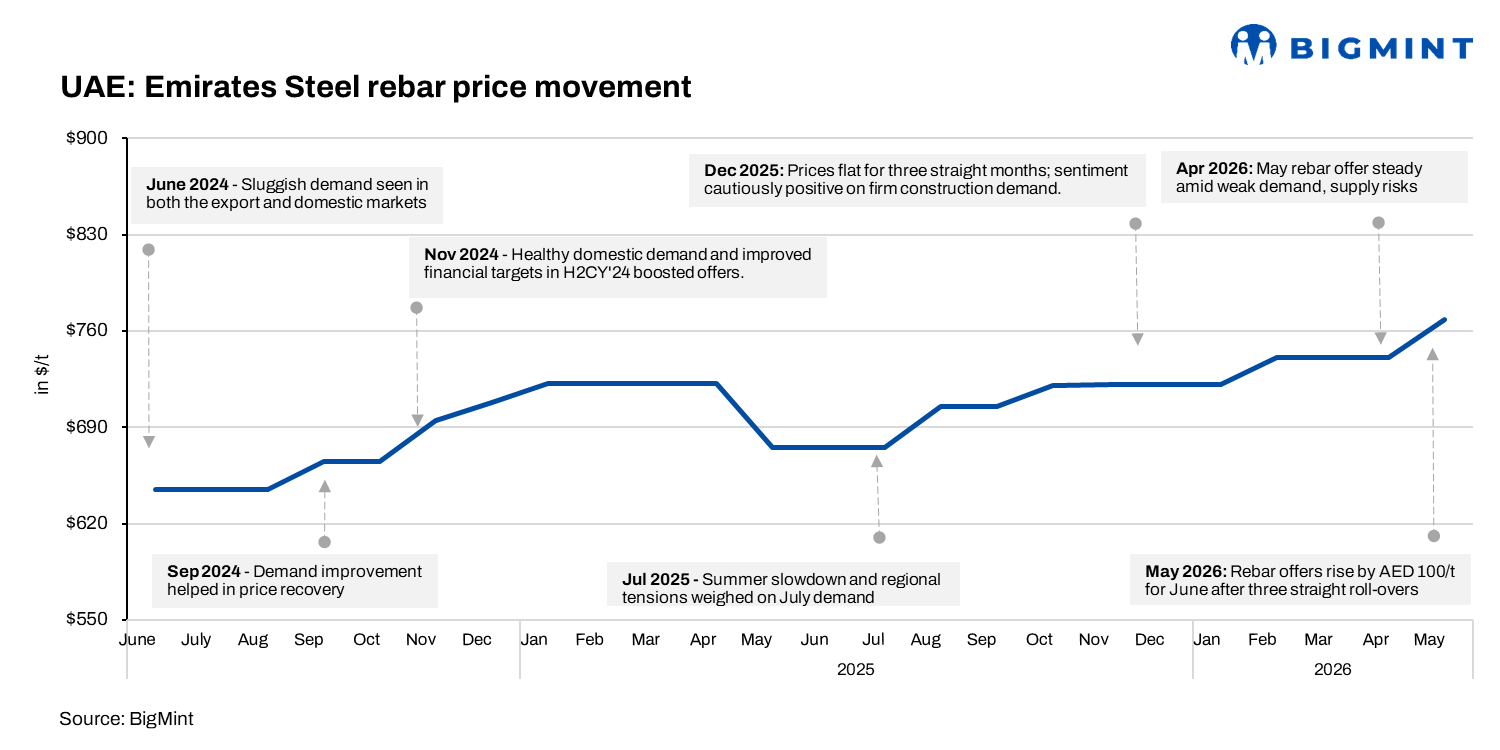

- Rebar offers rise after three consecutive monthly roll-overs

- Billet shortages and logistics disruptions tighten Gulf steel supply

EMSTEEL, one of the UAE’s leading steel and building materials producers, has increased its June 2026 domestic rebar prices by over AED 100/t ($27/t) after maintaining stable levels for three consecutive months between March and May. The benchmark producer’s latest rebar offers are now at AED 2,821/t ($768/t) exw under 90-day LC terms, while additional discounts of around AED 65-75/t ($18-20/t) are still reportedly available for large-volume buyers under memorandum arrangements.

Market participants linked the upward revision to tightening imported raw material availability, billet shortages, and growing logistical uncertainties across the Gulf region. However, the latest increase was viewed as relatively moderate compared with earlier market expectations despite ongoing supply chain disruptions across the GCC.

Billet shortages and logistics disruptions pressure market

The increase in UAE rebar offers comes amid rising freight costs, delayed cargo movements, and continued uncertainty surrounding imported billet supplies across the Gulf region. Market sentiment has strengthened in recent weeks as buyers increasingly build precautionary inventories to counter potential disruptions.

Industry sources said the rally is being driven by semis shortages and logistics bottlenecks amid ongoing geopolitical tensions in the Middle East. “We are trying to keep inventories high because nobody knows how long the Strait of Hormuz disruption will continue,” a Gulf market participant said.

Sources added that many UAE re-rollers continue to face billet shortages for June rolling schedules, while truck shortages and freight disruptions across the GCC are further pressuring regional steel flows. “Most mills do not have enough billet for rolling,” a Gulf-based industry insider said.

EMSTEEL reports stronger Q1 profitability

Despite weaker steel sales volumes, EMSTEEL reported stronger Q1 2026 earnings, supported by lower raw material costs and operational efficiencies. Group revenue remained stable y-o-y at AED 2.2 billion ($590 million), while operating profit surged 185% to AED 329.3 million ($89.7 million) and net profit rose 246% to AED 298.7 million ($81.3 million).

“EMSTEEL has delivered a strong start to 2026, driven by disciplined cost optimisation and operational efficiency,” group CEO Saeed Ghumran Al Remeithi said.

Saudi mills continue raising prices

Saudi Arabia’s long steel market had already moved upward earlier in May, with Saudi Iron and Steel Company (Hadeed) increasing rebar and wire rod offers amid persistent cost inflation and supply-side pressure.

Hadeed raised May rebar prices by SAR 100/t ($27/t) w-o-w to SAR 2,900/t ($774/t) DAP, while 6.5-14 mm wire rod offers increased to SAR 2,950/t ($787/t) DAP. Later in the month, the producer implemented another SAR 30/t ($8/t) increase, taking rebar prices to SAR 2,930/t ($781/t) DAP and wire rod to SAR 2,980/t ($795/t) DAP.

Market participants attributed the increases to raw material shortages, elevated inland transportation costs, and ongoing regional instability. “Big mills are not making money because they don’t have raw materials and logistics cost from Jeddah to the Eastern Province is extremely high, specifically for Hadeed and Al Ittefaq Steel. Small mills are enjoying,” a Saudi-based trader source said.

According to market participants, large mills continue to face operational pressure linked to metallics availability, freight expenses, and supply chain disruptions, while some smaller producers are reportedly benefiting from higher market prices and lower exposure to complex logistics chains.

Discounts persist despite higher official offers

Despite repeated increases in official offers, workable transaction prices in Saudi Arabia continue to trail published levels due to subdued construction demand. Producers in the western and central regions are reportedly offering discounts to secure volumes, while buyers continue limiting purchases to immediate requirements.

“Despite the announced prices, actual deals are still being concluded lower,” a regional market source noted.

Before the latest increases, Saudi rebar indications were largely heard at SAR 2,750-2,900/t DAP, while smaller regional mills were offering at SAR 2,620-2,700/t DAP.

Outlook

Middle East long steel prices are expected to remain firm in the coming weeks, supported by elevated freight costs, billet shortages, and geopolitical uncertainty. However, subdued construction activity and widening gaps between official and workable transaction levels may continue limiting aggressive price gains unless downstream demand improves materially.

Leave a Reply