- Competitive Indonesian imports and possible ADD reduction support market stability

- Firm coking coal costs keep coke prices supported

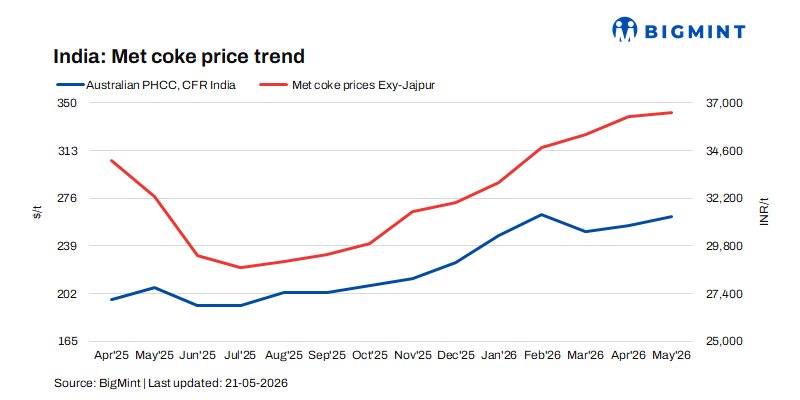

India’s blast furnace (BF)-grade metallurgical coke prices remained largely stable week-on-week as of 21 May 2026, supported by balanced supply-demand dynamics, firm import parity, and steady downstream steel production. Domestic suppliers continued to maintain price discipline amid stable procurement activity from integrated steel mills and sponge iron producers.

In the eastern region, BF-grade coke prices increased marginally by INR 300/t to INR 36,700/t ex-Jajpur, reflecting improved buying interest and higher logistics costs. Meanwhile, prices in western India remained stable at INR 33,500/t ex-Gandhidham, indicating sufficient material availability and steady trade flow. Foundry-grade (+90 mm) coke prices also remained unchanged at INR 36,400/t ex-Rajkot, suggesting stable demand conditions from the casting and foundry segment.

In the spot market, a bulk trade for 15,000 t was reportedly concluded by a trader at INR 37,000/t ex-warehouse, indicating sustained procurement interest from consumers seeking cost-effective imported material amid firm domestic pricing.

Market participants highlighted that freight charges have increased in line with the recent rise in global crude oil prices, leading to elevated transportation and landed costs across the supply chain. However, the market impact of the prevailing anti-dumping duty (ADD) remains uncertain and continues to await further policy clarity.

Imported coke offers remain competitive

Following the Directorate General of Trade Remedies’ (DGTR) proposal to reduce anti-dumping duty on imported metallurgical coke, market sentiment toward imports has improved further. As per BigMint’s assessment, Indonesian-origin BF-grade coke (65/63 CSR) was assessed at around $302/t CFR India, stable w-o-w.

Coking coal market continues to support coke costs

The global coking coal market remained firm, continuing to provide cost support to coke prices. As of 6 May 2026, Australian premium hard coking coal (PHCC) prices increased by $8/t w-o-w to $241/t FOB Australia amid tight availability of high-quality coal and improved buying interest.

Simultaneously, China’s domestic coke market remained stable w-o-w, supported by steady coking coal supply and firm steel mill demand amid sustained pig iron production. Coke producers maintained stable operating rates following the third round of coke price hikes, while inventories remained low due to smooth dispatches.

Several major coking plants have initiated a fourth round of coke price increases by Yuan 50-55/t, although steel mills are yet to formally respond. Overall, the Chinese coke market is expected to remain stable to slightly firm in the near term, lending further support to global coke sentiment.

Pig iron market reflects cautious buying sentiment

On the downstream side, pig iron market indicators reflected relatively cautious sentiment despite stable steel production levels. Steel-grade pig iron prices in Durgapur increased marginally by INR 150/t w-o-w to INR 38,450/t ex-works, supported by firm raw material costs.

However, buying sentiment appeared comparatively restrained in recent auctions. Steel Authority of India Limited Rourkela auctioned 4,500 t of steel-grade pig iron on 21 May 2026, with the entire quantity booked at an average price of INR 37,750/t ex-works. The auction price declined by INR 2,250/t compared with the previous auction held on 8 May 2026, where 500 t were sold at INR 40,000/t ex-works, indicating cautious procurement strategies among buyers amid fluctuating finished steel market conditions.

Outlook

India’s met coke market is expected to remain stable to slightly firm, supported by elevated coking coal costs, steady steel production, and competitive Indonesian imports. Any reduction in ADD may further improve import viability and increase inflows.

However, market sentiment will continue to depend on freight trends, ADD clarity, and demand from competing markets such as China and Vietnam. Firm raw material costs are likely to limit any major downside in coke prices.

Leave a Reply