- Soft demand drags steel, scrap prices lower

- Higher dollar limits import scrap bookings

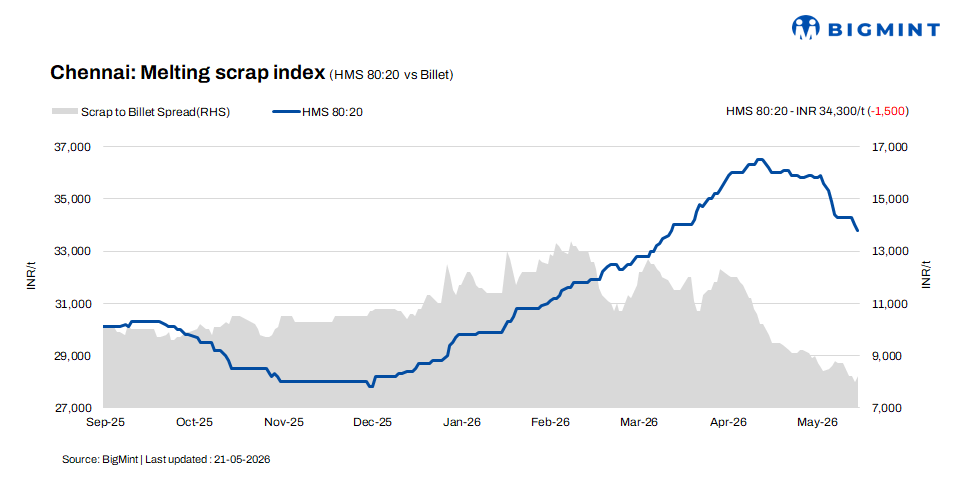

According to BigMint assessment, HMS (80:20) scrap prices in Chennai declined by INR 200/t d-o-d to INR 33,800/t, registering a weekly decrease of INR 500/t. In the semi-finished segment, billet prices remained stable d-o-d at INR 42,000/t, though they recorded a weekly decline of INR 1,000/t.

Similarly, in the finished steel segment, rebar prices fell by INR 500/t w-o-w to INR 49,000/t, while remaining unchanged on a daily basis. The continuous correction in steel prices suggests subdued demand from end-users and cautious market sentiment, which continues to weigh on overall pricing trends.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $385-390/t CFR Chennai, while HMS (80:20) was quoted at $365-370/t CFR. Despite the ongoing shortage of scrap in the domestic market, buying interest for imported material remained subdued.

Market sources attributed the cautious sentiment to the higher dollar-to-INR exchange rate, with the dollar currently trading around INR 96.30-96.40, significantly increasing the landed cost of imported scrap. As a result, buyers remained hesitant to place fresh import bookings, preferring domestic material despite tight availability, as it remains relatively more cost-effective under current market conditions.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 33,500-34,000/t for spot deals with immediate payment. Meanwhile, transactions on extended credit terms were concluded at higher levels of INR 34,000-34,500/t.

Overall, trading activity remained largely concentrated within the INR 33,500-34,500/t range, with price variations primarily influenced by payment terms and mill-specific volume requirements. Market participants continued to adopt a need-based procurement approach, while cautious sentiment in the steel segment kept trading activity controlled.

Buyer-supplier sentiments

According to sources, the south Indian steel industry is currently under pressure amid weak demand conditions. Despite production cuts and lower operating rates of around 60-70%, inventory levels continue to rise, with mills currently holding nearly 15-20 days of stock. Weak demand in the finished steel segment has limited material offtake, adding pressure on producers.

Additionally, steel plants are facing higher operating costs due to constrained availability of industrial gases and fuels, impacting production economics. Labour shortages, driven by workers returning to their hometowns during the summer season, have further disrupted operations. Market participants believe these challenges may force mills to further reduce operating capacities in the near term.

A market participant noted that HMS (80:20) scrap prices are currently ranging between INR 33,500-34,500/t, depending on payment terms and procurement volumes. Labour shortages caused by extreme summer conditions continue to disrupt scrap processing activities, resulting in limited material availability in the market.

In addition, higher imported scrap prices, driven by the elevated dollar-to-INR exchange rate, are further tightening supply conditions. The increased landed cost of imported scrap has discouraged fresh bookings, adding pressure on domestic availability.

Regional comparison

In the western India based Jalna market, billet and rebar prices remained stable at INR 41,400/t and INR 46,400/t, respectively, while HMS (80:20) scrap prices declined by INR 100/t to INR 34,000/t.

Market participants highlighted that the ongoing fuel supply shortage is creating transportation-related disruptions, as reduced vehicle availability has affected material movement across the region. The logistical constraints are exerting pressure on supply chains and market operations, influencing trading activity in both scrap and steel segments.

Outlook

The Chennai scrap market is expected to remain range-bound in the near term, as weak billet and rebar demand continues to weigh on sentiment. However, tight scrap availability due to labour shortages and higher imported scrap costs amid elevated USD-INR levels may restrict any sharp downside. Mills are likely to continue need-based procurement, while cautious buying sentiment may limit upside momentum. Price movements are expected to remain within INR +/- 200-500/t.

Leave a Reply