- High energy costs reduce smelter operating rates

- Maintenance activities constrain Brazilian aluminium facilities

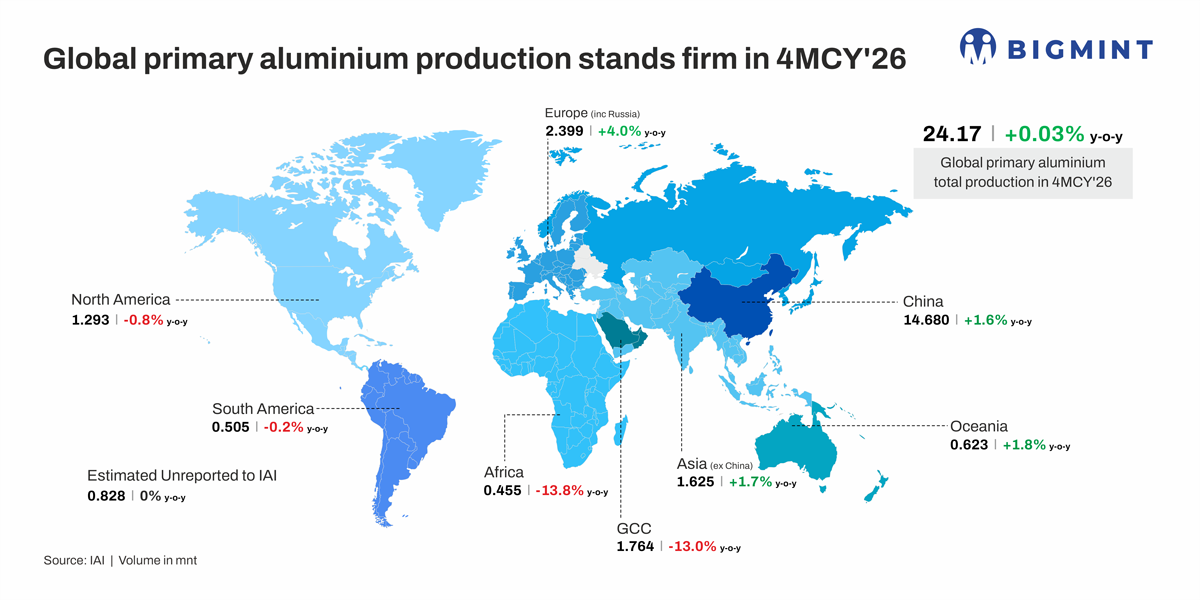

Global primary aluminium production stood at 24.17 mnt in 4MCY’26, marking a marginal 0.03% y-o-y increase from 24.16 mnt in 4MCY’25 according to data from the International Aluminium Institute. The stable production trend reflects generally balanced operating conditions across major smelting regions, supported by resilient output in China and improved production levels in parts of Europe, which offset declines in select regions. Overall, production levels remained firm, indicating continued operational stability across key global aluminium-producing hubs and supporting a broadly steady near-term supply outlook.

Regional drivers shaping global primary aluminium output in 4MCY’26

Global primary aluminium production in 4MCY’26 exhibited mixed regional trends, reflecting a combination of energy availability, geopolitical disruptions, raw material supply adjustments, and shifting trade dynamics across major producing regions, with the Middle East emerging as a key factor influencing near-term global aluminium supply conditions.

China, the world’s largest aluminium producer, increased output by 1.6% y-o-y, supported by resilient smelter operating rates, steady domestic demand, and policy-controlled capacity limits near 45 million tonnes. However, production momentum remained constrained as the country continued operating close to its de facto production ceiling, leaving limited room for further capacity expansion. Following the Lunar New Year, downstream demand softened while exchange ingot stocks increased, prompting smelters to moderately ease run rates and operate slightly below full capacity instead of pushing additional supply into an already saturated market. China also continued benefiting from improving export opportunities amid supply disruptions in the Middle East, helping maintain relatively stable production momentum despite broader global uncertainties.

In Africa, production declined sharply by 13.8% y-o-y, primarily due to operational disruptions, power supply concerns, and continued uncertainty surrounding key regional smelting assets, which weighed heavily on overall output stability across the continent. The decline was largely attributed to Mozambique’s Mozal smelter being placed under care and maintenance after South32 failed to secure an affordable electricity tariff agreement. As operations at the facility gradually wound down, saleable aluminium production reportedly declined by nearly 28%, significantly impacting regional supply conditions.

North America recorded a marginal 0.8% y-o-y decline in aluminium production, as elevated energy costs, competitiveness pressures, and slower progress in expanding domestic smelting capacity continued to limit operating rates across the region. The decline was mainly linked to reduced operating rates at several major US smelters rather than permanent capacity closures, reflecting cautious production management amid uncertain market conditions and persistently high operating costs.

South America’s aluminium output remained broadly stable, edging down by 0.2% y-o-y amid lingering operational constraints and uneven utilization levels across older production facilities, although improving investment activity offered some medium-term support to the regional outlook. Brazilian operations including Albras, Alunorte, and Alupar operated below capacity due to planned maintenance activities, persistent power cost pressures, and infrastructure-related constraints.

Conversely, Asia excluding China posted a 1.7% y-o-y increase, supported by steady downstream demand, improving industrial activity, and rising regional competitiveness as global buyers diversified supply chains outside China. However, some operational challenges persisted across key producing nations, particularly in Indonesia, where smelters operated below full capacity due to grid availability issues, coal supply disruptions, and routine maintenance activities, especially anode-change cycles.

Europe, including Russia, registered the strongest regional growth at 4% y-o-y, supported by easing energy-related pressures, improved smelter economics, and stronger regional demand amid tightening supply conditions following Middle East disruptions. However, some smelters across Russia and Europe continued to face temporary maintenance shutdowns, routine anode-change cycles, and mild grid-related curbs at alpine and Balkan production facilities.

Oceania’s aluminium production rose by 1.8% y-o-y, supported by stable hydropower-linked smelting operations and improved operational efficiency across key regional facilities, helping maintain consistent output levels. However, production growth remained partially constrained by scheduled maintenance activities and tighter alumina supply availability at major Australian smelting operations.

Meanwhile, aluminium production in the Gulf Cooperation Council (GCC) region declined significantly by 13% y-o-y, reflecting the impact of geopolitical tensions, supply-chain disruptions, and operational setbacks at major smelters following the escalation of the Iran-Israel conflict. The blockage of the Strait of Hormuz created immediate shipping and logistics constraints across the region, disrupting the movement of both raw materials and finished aluminium products. Aluminium Bahrain (Alba) invoked force majeure on certain product deliveries and subsequently implemented controlled shutdowns of potlines 1, 2, and 3, removing approximately 308,369 tonnes, or nearly 19% of its 1.62 million tonnes annual production capacity.

Simultaneously, Qatar’s Qatalum smelter shut operations due to gas supply disruptions and later resumed production at only around 60% capacity, effectively reducing output by nearly 256,000 tonnes. The situation further escalated following drone and missile attacks targeting Emirates Global Aluminium (EGA) and Alba facilities, with EGA reporting significant operational damage while Alba continued assessing the impact on production infrastructure. Disruptions to logistics through the Strait of Hormuz and pressure on raw material flows continued to weigh on regional aluminium supply conditions, intensifying concerns over global supply tightness.

Finally, estimated unreported production to the International Aluminium Institute remained unchanged y-o-y, indicating relatively stable output from producers or regions outside the formal reporting framework.

Impact of pricing

On a 4MCY basis, LME aluminium prices averaged $3,283/t in 4MCY’26, marking a sharp 27.7% y-o-y increase from $2,570/t in 4MCY’25. Meanwhile, LME aluminium inventories declined by 14.1% y-o-y, averaging 453,944 t compared with 528,646 t during the same period last year, reflecting tightening exchange availability and growing concerns over global supply disruptions.

In Jan’26, LME aluminium cash prices remained above $3,000/t, supported by continued inventory drawdowns and firm physical market premiums, while exchange stocks declined below 510,000 t, supporting positive market sentiment.

In Feb’26, aluminium prices strengthened further, with LME cash offers rising above $3,200/t amid declining exchange inventories and increasing concerns over supply-chain disruptions in the Gulf region. Tight physical availability and firm Asian market premiums continued to support upward price momentum.

Moreover, in Mar’26, LME aluminium prices surged sharply, with cash offers crossing $3,500/t and touching multi-year highs following escalating Middle East tensions that disrupted Gulf smelting operations and shipping routes through the Strait of Hormuz. LME inventories also continued to decline during the month, reinforcing bullish market sentiment.

In Apr’26, aluminium prices remained elevated despite some correction from peak levels, continuing to hover above $3,600/t amid persistent geopolitical uncertainties and lower exchange stocks. However, easing supply panic and improved physical market activity limited further upside during the latter half of the month.

Outlook

Global primary aluminium market conditions are expected to remain firm in the near term amid elevated LME prices, declining exchange inventories, and continued geopolitical uncertainties across the Middle East. While stable production trends in China, Europe, and Oceania are supporting overall global output, disruptions across the GCC region and logistical risks around the Strait of Hormuz are likely to continue influencing regional supply flows and physical market conditions.

Continued pressure on exchange stocks and uncertainty surrounding Middle East supply chains are expected to support physical premiums and keep aluminium prices firm in the coming months, although stable operating rates across major smelting hubs may help prevent severe global supply disruptions.

Leave a Reply