- Tata Steel overtakes JSW Steel as largest Indian steelmaker

- Focus stays on downstream expansion than volume-led growth

- Q1FY’27 margins expected to improve q-o-q despite higher costs

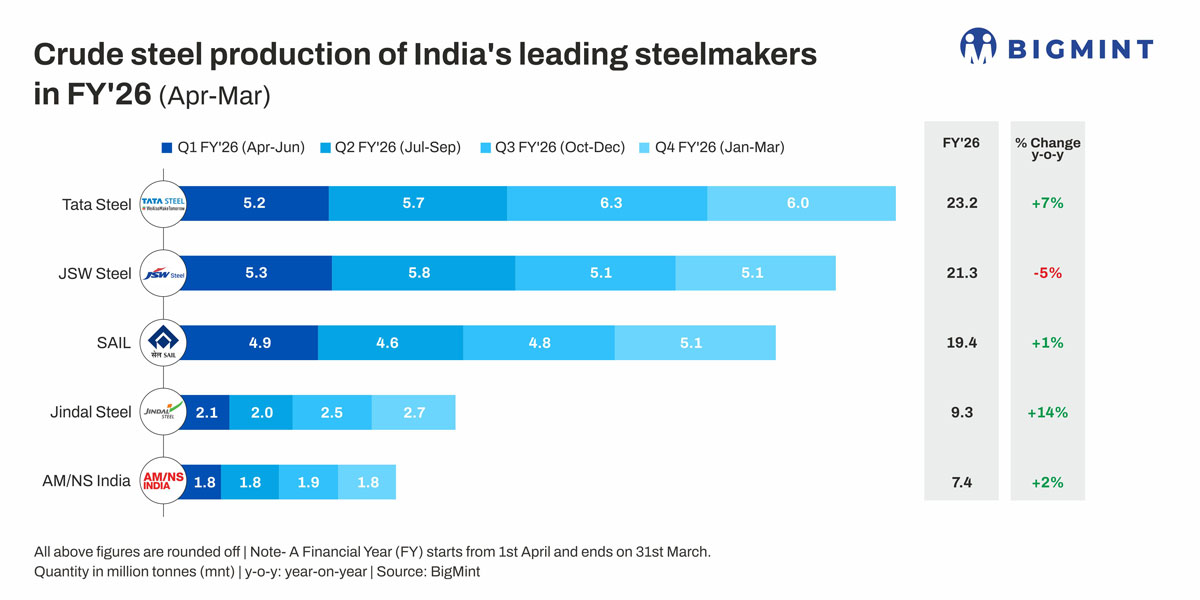

Morning Brief: India’s tier-1 steelmakers reported mixed growth in crude steel production in FY’26 even as sales increased y-o-y. Among these steelmakers, which account for roughly half of India’s crude steel output, only Jindal Steel recorded production growth above India’s overall 11% increase in crude steel output.

A prolonged demand downturn during the extended monsoon likely limited production growth during FY’26, along with slower capital expenditure disbursement. However, the broader industry narrative remains on capacity expansion, downstream integration, raw material security, and market positioning for the next decade of domestic demand growth. BigMint analyses the key themes shaping Indian steelmakers’ next phase of growth, as per their quarterly earnings calls.

Tata Steel posts mild growth, plans for downstream expansion

Considering standalone volumes, Tata Steel overtook JSW Steel to emerge as the country’s largest crude steel producer in FY’26 with output of 23.2 million tonnes (mnt), up 7% y-o-y following the Kalinganagar expansion from 3 mnt/year to 8 mnt/year. Parallelly, the company’s sales volumes rose 8% y-o-y to 22.53 mnt during FY’26.

In terms of future growth, Tata Steel is focusing on value-added and downstream capacity rather than pure upstream volume expansion. The company believes that future profitability will depend less on absolute steel volumes and more on product mix improvement and downstream penetration.

The company is attempting to structurally reduce dependence on basic grades such as hot-rolled coils (HRCs) by increasing exposure to galvanised steel, packaging steel, tubes, wires, colour-coated products, and advanced automotive grades. This reflects a wider trend emerging across Indian steelmakers as margins in basic flat steel grades remain vulnerable to Chinese exports and global steel price volatility.

The management also indicated that Tata Steel already has the optionality to expand Indian capacity to 45-50 mnt using existing sites at Kalinganagar, Neelachal, Jamshedpur and Bhushan. A future Maharashtra project could add another 6-10 mnt. However, the company intends to pursue phased, disciplined expansion rather than aggressive volume growth.

Unlike some peers, Tata Steel explicitly rejected the idea of partnering with global steelmakers for India expansion. The company is instead consolidating ownership across its businesses by buying out joint venture partners and integrating operations.

JSW Steel’s output dips, but capacity expansion plans accelerate

JSW Steel’s crude steel production decreased by 5% y-o-y to 21.3 mnt amid the shutdown of Blast Furnace 3 (BF3) at Vijayanagar for expansion purposes. Despite this, sales increased by 3% y-o-y to 22.4 mnt.

JSW Steel is pursuing an aggressive growth model. The company now targets 62 mnt of standalone India capacity by FY’32 versus an earlier 50 mnt goal. Including proposed joint ventures with Japan’s JFE Steel and South Korea’s POSCO, total capacity could approach 78 mnt.

The company expects infrastructure spending, urbanisation, manufacturing growth, and rising flat steel consumption to support annual incremental steel demand growth of 12-14 mnt.

JSW Steel also appears bullish on flat steel demand. The company believes domestic supply growth will continue to lag demand growth, particularly in higher-grade products where entry barriers and project execution timelines remain high.

While port-based assets in Paradip would offer export opportunities, JSW believes that domestic demand will remain the primary outlet for new capacity.

Unlike Tata Steel’s preference for independent expansion, JSW Steel views partnerships with JFE and POSCO as strategic tools for gaining access to advanced automotive steels, electrical steel, hydrogen-based steelmaking technologies, and decarbonisation expertise.

On decarbonisation, JSW Steel acknowledged that blast furnace-led growth will continue to dominate its Indian steelmaking operations because of domestic raw material dynamics and limited scrap availability. However, the company plans to gradually expand electric arc furnace and scrap-linked steelmaking, including the proposed Salav green steel project using DRI, scrap, and renewable energy.

SAIL lifts output, to focus on increasing capacity utilisation

The Steel Authority of India (SAIL) posted a minor 1% increase in crude steel production to 19.4 mnt, while sales rose by a sharper 12% y-o-y to 19.9 mnt.

SAIL’s FY’27 strategy is centred on increasing utilisation at existing assets before large brownfield expansions begin contributing from FY’31 onward. SAIL maintained an aggressive sales guidance of 22 mnt for FY’27 versus around 20 mt in FY’26. The company believes operational efficiencies, productivity improvements, and debottlenecking can push production to over 22 mnt in FY’27, beyond its rated crude steel capacity of 21 mnt.

Jindal Steel posts strongest hike in output, targets sustained growth in FY’27

Jindal Steel recorded the strongest growth in production, up 14% to 9.25 mnt in FY’26 due to the doubling of capacity at Angul. The company’s sales increased by a slower 9% to 8.67 mnt, indicating a slight lag between production and demand.

Jindal Steel announced an FY’27 production guidance of 11.5 mnt and sales guidance of 10.5-11 mnt, implying another year of strong volume growth.

Notably, the company indicated that flat products currently account for around 50% of sales and could rise towards 70% over time as HRC production ramps up further. However, management pushed back against concerns that the rising share of HRC could dilute realisations. Instead, downstream value-added projects and niche product development would support realisation growth over time.

AM/NS India’s production inches up, Andhra expansion in focus

AM/NS India’s production and sales rose slightly by 2% to each to 7.4 mnt and 8 mnt, respectively.

The company expects upward momentum to continue into Q2 amid favourable pricing environment. Unlike its blast furnace-based Indian peers, AM/NS India has relatively higher gas exposure because of its DRI configuration at Hazira. However, the company has implemented multi-year gas hedging programmes and currently does not expect significant cost pressure from higher prices. Additionally, gas procurement is diversified and not solely dependent on Middle Eastern supply sources.

The company also reiterated that its broader vision for 40 mnt/year of steelmaking capacity in India remains unchanged. Presently, the priority is the planned greenfield Andhra Pradesh project with proposed capacity of around 8 mnt/year. Once the first phase of Andhra is completed, the company could either expand Andhra further or revisit additional capacity expansion at Hazira.

EBITDA/t improves in Q4FY’26

Steel prices made a seasonal recovery in Q4FY’26, leading to a q-o-q surge in the EBITDA per tonne of all steelmakers. However, the Middle East conflict also lifted prices as supply concerns emerged and buyers made panic purchases, leading to a y-o-y EBITDA per tonne values, though at a more moderate pace. Spot prices of BF-route HRCs and rebars surged by 15% and 23% q-o-q, while iron ore rose a slower 7%. However, coking coal was up by 25% q-o-q.

Y-o-y, BF-route rebar prices increased 9% and HRC rose 12%. However, both iron ore, up by 17%, and coking coal, up 36%, outstripped the growth in steel prices. This explains the largely slower increase in EBITDA per tonne y-o-y.

Outlook

Industry confidence in long-term domestic demand remains strong despite global steel market uncertainty and persistent Chinese export pressure. Most large steelmakers appear convinced that India’s infrastructure-led growth, manufacturing expansion, and urbanisation cycle will support sustained steel demand growth through the decade.

Additionally, mills expect Q1FY’27 EBITDA/t to improve sequentially because steel price increases are currently exceeding the rise in coking coal, freight, and energy costs. Although construction demand is likely to decline as the monsoon arrives, flat steel continues to benefit from safeguard duties and higher import parity pricing.

Leave a Reply