- Firm freight continues limiting fresh scrap transactions

- Weak steel demand and rising costs pressure mill margins

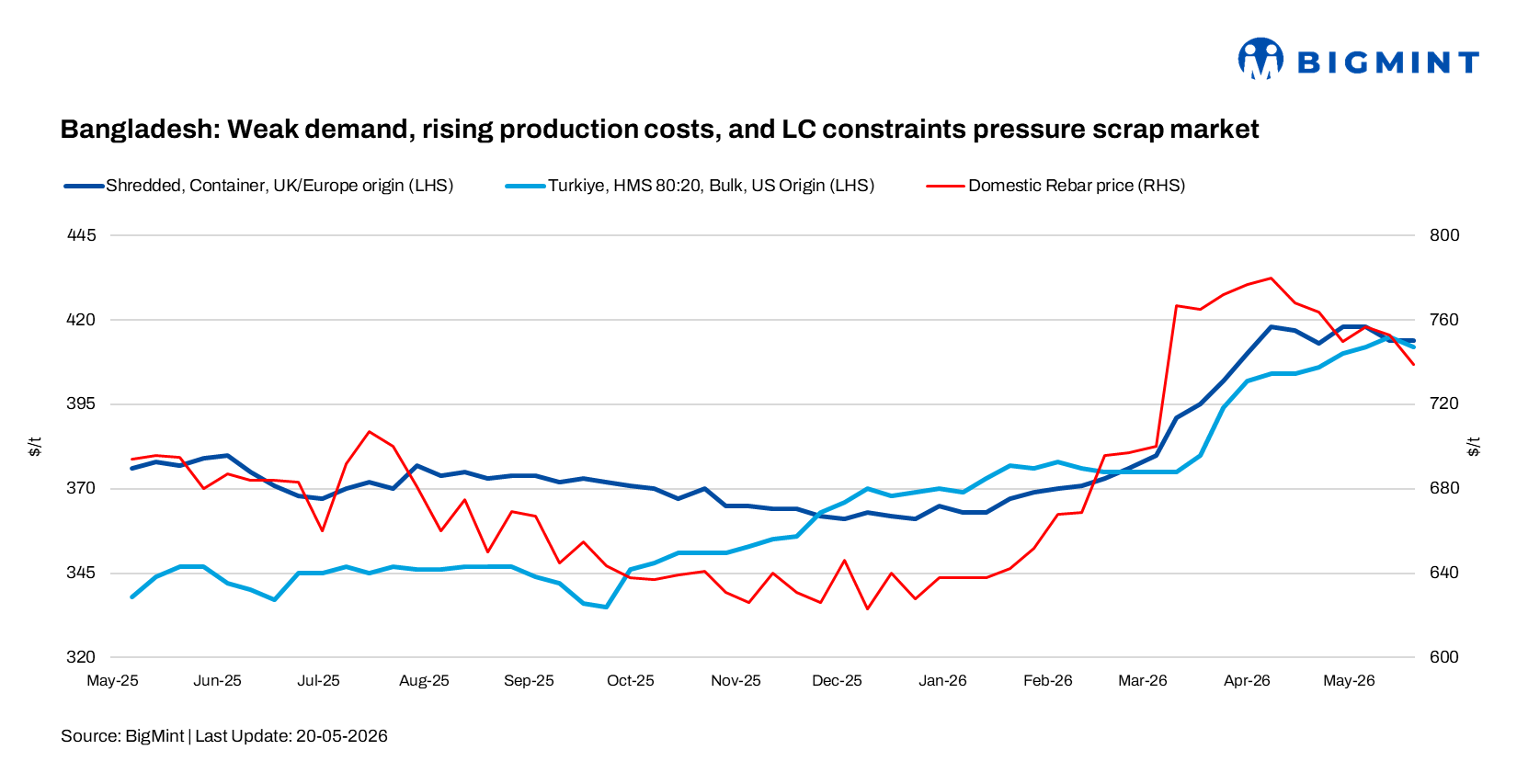

Bangladesh’s imported ferrous scrap market remained subdued during the week, with mills avoiding aggressive fresh bookings due to weak finished steel demand, rising utility costs, and persistent LC-related constraints. Market participants said higher electricity and gas costs continued to pressure steelmakers’ margins, resulting in reduced production rates and slower construction activity.

Market participants added that imported scrap procurement remained limited as many mills continued prioritising inventory management over fresh purchases due to squeezed steel margins and uncertain demand visibility.

BigMint’s weekly assessments CFR Chattogram

- European-origin containerised HMS (80:20): $389/t, down by $1/t w-o-w

- European-origin containerised shredded: $414/t, stable w-o-w

- Japanese-origin bulk H2: $405/t, inched down by $2/t w-o-w

- US-origin bulk HMS (80:20): $410/t, stable w-o-w

Buying interest remained selective, with most participants focusing only on prompt and competitively priced cargoes amid elevated freight rates and tight financing conditions.

Imported shredded scrap offers from the US were heard near $410/t CFR Bangladesh, while HMS offers were indicated around $380/t CFR. Separately, around 1,000 t of Australia-origin PNS plus HMS 90:10 cargo was reportedly sold at $403/t CFR Chattogram. A deal for 500 t of Philippines-origin GI bundles was also heard concluded at $345/t CFR Bangladesh, while another GI bundle offer at $340/t CFR reportedly failed to attract buyer interest.

Market comments

A Dhaka-based mill source said, “We have not purchased much imported scrap recently because LC availability remains tight and our production costs have increased significantly. Construction demand remains slow; so most mills are operating cautiously and limiting production.”

Another industry participant commented, “Electricity and gas costs have increased sharply over the past year, while steel demand has not recovered. Any further utility price hike will put additional pressure on already weak mill margins.”

A Chattogram based trader said, “Freight remains very expensive, making it difficult to conclude deals unless sellers reduce prices further. Buyers are active only for prompt and competitively priced cargoes.”

Domestic rebar prices in Chattogram were heard around BDT 92,000-93,000/t ($749-757/t) for major brands, while Dhaka rebar prices were indicated lower at BDT 82,000-88,000/t ($667-716/t) amid sluggish downstream demand. Local scrap prices were reported around BDT 45,000-49,000/t ($366-399/t).

Market sentiment weakened further amid concerns over potential electricity tariff hikes. The Bangladesh Steel Manufacturers Association (BSMA) recently warned that any further increase in power tariffs could force several mills to shut operations, as electricity already accounts for nearly 30% of steel production costs.

Industry participants noted that gas prices have surged nearly 300% and electricity tariffs around 30% in recent years, adding significant pressure on mills already struggling with liquidity shortages, high borrowing costs, and sluggish downstream demand.

Outlook

Bangladesh’s imported scrap market is expected to remain slow in the coming days as weak construction activity, elevated production costs, and tight financing conditions continue to weigh on buying sentiment. Concerns over potential electricity tariff hikes may further pressure steelmakers’ margins and limit production rates. While some mills may continue selective bookings for immediate requirements, high freight costs and cautious steel demand are likely to restrict large-volume transactions.

Leave a Reply