- Alloy costs support stainless steel market sentiment

- Chinese HRC prices soften after Tsingshan price cuts

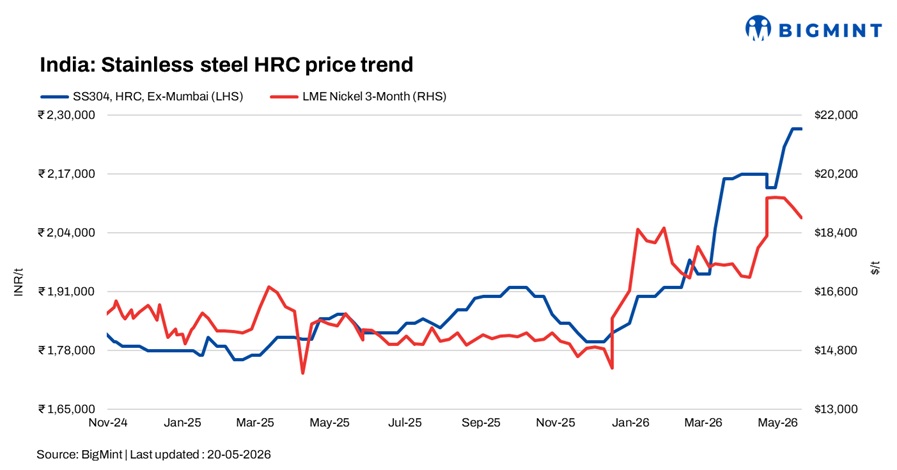

India’s stainless steel finished market witnessed mixed trends in the week ended 20 May 2026, as rising nickel and ferro molybdenum prices continued to support sentiment, while buying activity largely remained requirement-based amid persistent cost pressure and volatile raw material movements.

Market participants remained cautious due to fluctuations in LME nickel prices, which continued to keep stainless steel pricing volatile across flat and long product segments.

HRC/CRC segment supported by rising alloy costs

India’s stainless steel HRC/CRC market moved higher during the week, particularly for 316-grade products, supported by sharp increases in nickel and molybdenum costs. A major domestic stainless steel producer revised HR and CR coil prices effective 19 May, mainly due to elevated nickel prices and a sharp rise in molybdenum costs amid global concentrate shortages and strong Chinese demand.

In addition, market participants noted that rupee depreciation has increased the cost of imported raw materials, further strengthening domestic pricing sentiment. The producer raised 316 HR/CR coil prices by INR 10,000/t.

Another market participant stated that demand remained healthy, with buyers continuing restocking activity amid expectations of further price increases. At the same time, imports have slowed considerably as elevated international prices reduced the competitiveness of overseas material in the Indian market.

Globally, stainless steel HRC sentiment remained comparatively weaker than CRC products. Chinese domestic HRC prices softened following aggressive price cuts by Tsingshan, with 304 HRC prices in Foshan and Wuxi falling to around RMB 14,500/t. Meanwhile, Indonesian mills maintained relatively firm export HRC offers near $2,100-2,150/t CFR Asia, although transaction activity remained limited.

Despite Tsingshan reducing domestic CRC prices by RMB 300/t for 304 and RMB 500/t for 316L, CRC markets showed comparatively better resilience due to sustained demand from appliance, precision tube, decorative, and industrial application sectors. Indonesian CRC export offers reportedly witnessed only selective discounts of around $30-50/t, indicating mills are still attempting to protect margins.

Longs market supported by higher alloy costs

India’s stainless steel longs market also remained firm overall, supported by rising alloy costs. However, 304-series products continued to witness volatility in line with nickel price fluctuations.

As per BigMint’s assessments, 304 bright bars were reported at $4,000/t and 316 bright bars were stood at $4,000/t FOB Nhava Sheva.

Globally, indicative prices for 304 bright bars were heard at around $3,500-3,550/t FOB Europe, while 316 bright bars were assessed at approximately $4,600-4,700/t FOB Europe.

Market news

Mitsui O.S.K. Lines’ (MOL) proposed expansion in India’s shipbuilding sector is expected to support demand for marine-grade and specialty stainless steel products. Industry participants believe increasing domestic production of LNG carriers, chemical tankers, and green vessels could boost consumption of corrosion-resistant stainless steel, in line with India’s long-term stainless steel demand growth targets under the Stainless Steel Vision Document 2047.

Global market sentiment remains cautious

China’s stainless steel market remained volatile amid weak spot demand and rising inventories, particularly in the hot-rolled segment where transaction activity stayed sluggish. However, cold-rolled products showed relatively better stability due to tighter availability and continued value-added demand.

Elevated nickel and alloy costs, supported by Indonesian supply-side concerns and expectations of lower NPI production, continued to provide underlying support to the global stainless steel market.

Raw material scenario

Outlook

India’s stainless steel market is expected to remain firm in the near term, supported by elevated alloy costs, rupee weakness, and tighter import competitiveness. However, demand sustainability and global stainless steel trade flows will remain key factors influencing future price direction.

Leave a Reply