- Rice stocks remain above 13.5 mnt buffer norm

- Moderate offtake, sluggish exports limiting surplus absorption

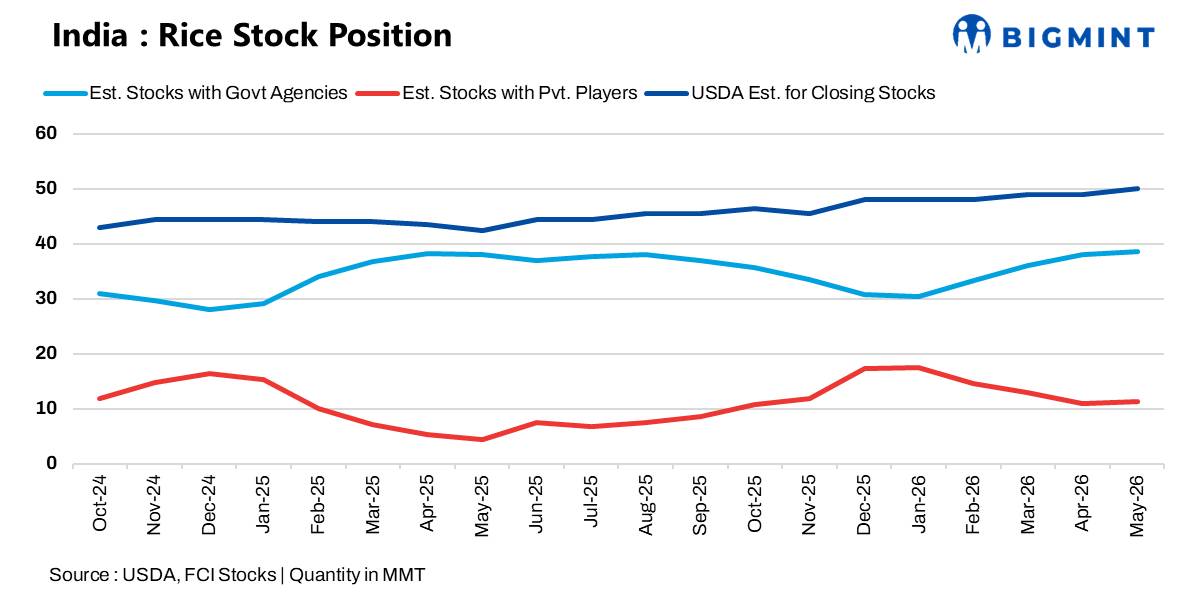

India’s rice stock position is supported by rising production estimates, slower export momentum, and increasing accumulation in both government and private channels. As per estimates, government-held rice stocks stood near 38–39 million metric tonnes (mnt) in May 2026, almost similar to May 2025 levels. However, the major shift this year has been the sharp rise in private trade inventories, estimated above 11 mnt compared with barely 4-5 mnt during the same period last year.

This indicates that surplus rice availability is no longer concentrated only with the Food Corporation of India (FCI) but has now spread across the broader supply chain. At the same time, USDA estimates suggest India’s closing rice stocks could approach 50 mnt by May 2026, versus around 42-43 mnt a year earlier, reflecting the widening gap between production growth and demand absorption.

Higher production keeps supply situation heavy

India continues to witness strong rice production cycles, with USDA estimating 2025–26 rice production at 152 mnt, up from 150 mnt in 2024–25, highlighting a steady increase in output over recent years. Higher acreage, favourable monsoon distribution, and improved yields have kept rice availability elevated across most producing states, reinforcing India’s position as the world’s largest rice producer and strengthening supply in both domestic and global markets.

However, unlike previous years, export momentum has not increased proportionately with abundant domestic availability. Global rice demand has remained relatively cautious, driven by competitive pricing from other Asian origins, weaker buying interest from key African markets, and continued freight volatility.

At the same time, many international buyers are maintaining hand-to-mouth purchasing strategies, limiting large forward commitments and contributing to slower export movement. Looking ahead, the upcoming kharif 2026 season may face downside risks from fertiliser-related supply disruptions, rising input costs, and possible El Niño-induced weather irregularities that could affect monsoon distribution and planting progress.

Ethanol diversion emerging as major absorption channel

With surplus rice stocks continuing to build up, ethanol production has increasingly emerged as an important alternative demand channel for absorbing excess supply. The government has been allocating rice from central pool stocks toward ethanol manufacturing to support the national blending programme, with FCI increasing rice allocation for ethanol production to 72 LMT. This reflects growing confidence in surplus rice availability and a continued push to support ethanol blending targets without significantly disrupting food supply balances.

The diversion has become particularly important at a time when export demand remains inconsistent, domestic consumption growth is gradual, and FCI-held inventories remain well above prescribed buffer requirements. However, market participants note that ethanol alone may not be sufficient to absorb the scale of surplus being generated annually if production continues to rise.

Storage concerns intensifying

One of the biggest concerns emerging from the current stock situation is storage management. Despite continuous allocations under welfare schemes, Open Market Sale Scheme (OMSS) operations, and ethanol diversion, rice inventories remain significantly above prescribed buffer norms.

Higher stockholding levels are creating increasing pressure across the storage and supply chain ecosystem. The burden on covered warehouse capacity has intensified, forcing greater reliance on open storage arrangements that raise concerns over effective stock management and weather-related risks. At the same time, higher inventory levels are adding to FCI’s carrying costs, while prolonged storage periods pose challenges for maintaining grain quality and efficient stock rotation ahead of the next crop arrivals.

Buffer norms far below current availability

India’s mandatory rice buffer requirement remains significantly lower than actual stock availability. Against a prescribed rice buffer norm of 13.5 mnt, current rice stocks stand at around 38 mnt, well above levels required for food security and public distribution needs.

This gives policymakers considerable flexibility to increase ethanol allocation, expand OMSS operations, encourage exports when global demand improves, and manage inflation through timely market intervention. However, maintaining such elevated inventories also increases the fiscal burden through higher storage, handling, and carrying costs.

Outlook

India’s rice market is likely to remain supply-heavy in the near term unless export demand improves significantly, domestic production moderates, or ethanol consumption expands more aggressively to absorb excess stocks. With USDA continuing to project higher ending inventories and domestic production remaining robust, effective storage management and timely stock liquidation may emerge as key policy priorities for the rice sector over the coming quarters.

Leave a Reply