- Buyers continue avoiding aggressive bookings

- Weak steel demand pressures sentiment

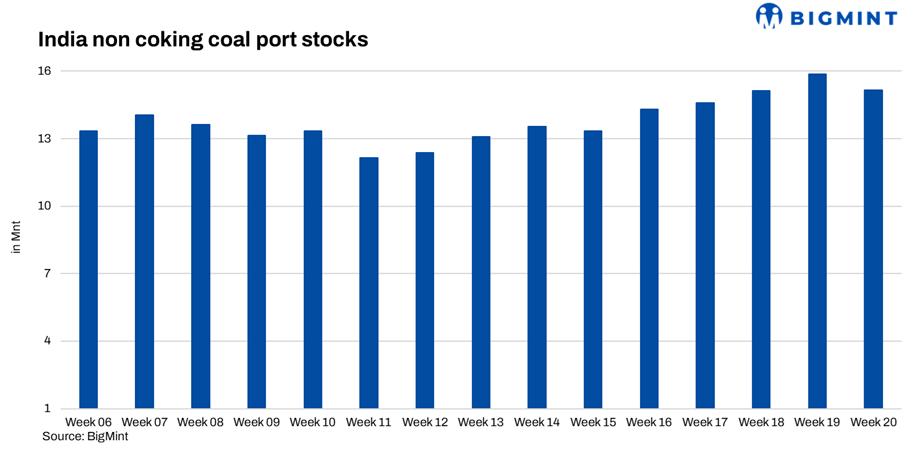

India’s thermal coal inventories at major ports declined 4.5% w-o-w in week 20 to 15.16 mnt from 15.87 mnt in week 19, indicating improved evacuation across key ports despite continued weak downstream demand. However, overall inventory levels remained elevated, reflecting comfortable supply conditions and cautious industrial procurement across imported and domestic coal markets.

Portside movement remained mixed during the week, indicating selective cargo positioning and regional evacuation trends rather than strong consumption recovery. Significant stock declines at ports such as Krishnapatnam, Tuna, Mundra and Haldia reflected improved material movement and lower fresh inflows, while inventories at Hazira, Magdalla, Karaikal and Tuticorin increased due to fresh arrivals and slower evacuation.

Participants indicated that most traders and industrial consumers continued maintaining balanced inventory positions instead of building additional stocks. Elevated inventories across major ports, combined with comfortable domestic coal availability, reduced urgency for fresh imported cargo purchases. Several buyers were also heard delaying procurement decisions in anticipation of softer demand during the approaching monsoon period.

Top inventory holders continued maintaining sizeable coal positions at ports, although movement remained selective amid weak industrial activity. Market participants stated that portside stock movement currently depended more on regional consumption requirements and logistics positioning rather than strong market demand.

Imported coal sentiment muted

Imported coal sentiment remained subdued despite firm global cues and higher freight costs. South African coal buyers largely resisted higher landed offers as sponge iron margins remained under pressure and downstream steel demand stayed weak. Limited enquiries continued across key imported coal markets, with buyers preferring immediate requirement-based purchases instead of aggressive stocking.

South African non-coking coal exports also declined sharply in April due to weaker buying interest from key Asian markets, especially India. Market participants indicated that lower Indian import bookings amid weak sponge iron demand, lower steel margins and comfortable domestic coal availability continued pressuring South African trade sentiment.

Indonesian coal sentiment remained comparatively firm due to tighter cargo availability, stronger Chinese demand and elevated freight rates. However, Indian buyers remained cautious amid high inventories and comfortable supply conditions. Market participants stated that although global coal indices stayed supported, weak industrial demand continued limiting aggressive spot buying activity in India.

Meanwhile, US-origin NAPP coal continued attracting cement sector buyers due to its cost competitiveness against imported petcoke. Buyers increasingly preferred coal blends amid comfortable fuel availability and expectations of softer cement demand during the monsoon season. Imported petcoke demand also remained weak as consumers continued shifting towards cheaper coal alternatives.

Domestic coal keeps supply comfortable

Domestic coal availability remained comfortable during the week due to frequent CIL auctions and lower premiums in recent SECL and MCL auctions. Buyers continued restricting purchases to immediate requirements as weak sponge iron and steel demand kept overall industrial sentiment subdued.

Market participants noted that regular auction volumes and elevated portside inventories continued preventing panic buying in the market. Although freight costs and international coal prices remained firm, domestic availability and cautious downstream demand continued limiting stronger imported coal movement.

Outlook

India’s thermal coal market sentiment is expected to remain cautious in the near term as comfortable inventories, weak industrial demand and sufficient domestic coal supply continue limiting aggressive procurement activity. Unless sponge iron, steel and cement demand improves meaningfully, buyers are likely to continue maintaining requirement-based purchases instead of building additional inventories.

Leave a Reply