- IEX prices hit ceiling repeatedly as supply tightens

- Coal stocks uneven despite ample availability at pitheads

The first seventeen days of May 2026 point to India’s power system operating under increasing stress. While the grid avoided a major breakdown, the gap between adequate supply and widespread load shedding narrowed considerably, with price signals on the Indian Energy Exchange (IEX) reflecting the tightening conditions.

What makes this period extraordinary is not any single factor. It is the confluence of three distinct pressures arriving simultaneously: an unforgiving heatwave that arrived earlier and hit harder than usual, a demand peak that shifted decisively into the late evening hours when solar generation vanished, and a coal stock position that, while adequate in aggregate terms, has become dangerously concentrated in a shrinking number of well-supplied plants.

The Generation mix: Renewables carry load

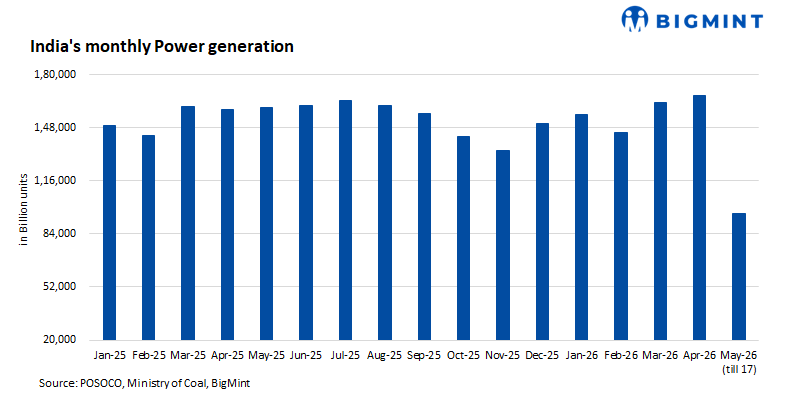

Between 1-17 May 2026, India generated 96,421 million units (MU) of electricity, a solid 6.1% y-o-y increase. However, the data also reflects changes in the generation mix alongside emerging supply-side constraints.

Coal remains the undisputed king of India’s power mix, contributing 69.3% of total generation. However, its share has actually declined by 1.6 percentage points compared to May 2025, when coal accounted for 70.9% of the mix. More tellingly, coal generation grew by only 3.7% y-o-y, significantly lagging the 6.1% growth in overall demand.

Meanwhile, generation from renewable energy sources (RES) surged by 23.4%, contributing 53% of all additional generation compared to last year. Wind and solar plants have been running at high utilisation, partly due to favourable weather conditions.

Hydro generation also posted a healthy 6.9% increase, suggesting decent reservoir levels heading into the summer. Nuclear generation grew 8.8%, a steady contribution.

However, gas-based generation collapsed by nearly 40% y-o-y to just 1,074 MU. With international LNG prices remaining elevated and domestic gas allocation prioritising the city gas sector, India’s gas power fleet has largely remained on the sidelines during this demand surge. The current demand conditions have brought this shortfall into sharper focus.

Demand and peak trends: The evening shift

The average peak demand during the first seventeen days of May 2026 was 234,500 MW, an 8.6% increase y-o-y. The maximum peak demand hit 250,296 MW on 14 May, surpassing last year’s high of 230,993 MW by nearly 20,000 MW.

However, the more important change is not the magnitude but the timing.

In a typical summer, India’s demand peaks in the afternoon, when office air conditioners, industrial loads, and household cooling all coincide. Solar generation is also at its peak during these hours, creating a natural balance. The evening hours usually see a decline in both temperature and demand.

May 2026 has broken that pattern. An intense and early heatwave has kept temperatures elevated well past sunset. In many parts of northern and central India, nighttime temperatures have remained 3-5 degrees Celsius above normal. As a result, air conditioners are running deep into the night, pushing the peak demand as late as 10:30 PM.

This is where solar generation becomes irrelevant. By 6 PM, solar output has dropped to near zero. The grid must then rely entirely on thermal, hydro, and imported power to meet a peak that is higher than last year’s afternoon peak. This “post-solar gap” is the single most important structural challenge exposed by the May 2026 data.

IEX price signals: From surplus to scarcity

The Indian Energy Exchange (IEX) has provided the clearest window into the stress. During 1-17 May 2025, the market was comfortably supplied. Sell bids totalled 6,710 GWh against purchase bids of 3,850 GWh, and the average Market Clearing Price (MCP) was a manageable INR 3,393 per MWh.

May 2026 has been a different scene.

Purchase bids jumped 28%, reflecting the surge in real-time demand from discoms caught off guard by the evening peaks. However, sell bids increased only 15%, and crucially, the clearance rate fell from 77% to 66%. Nearly one-third of all purchase bids went unmet.

The price behaviour has been extraordinary. During daylight hours, when solar generation is abundant, prices have occasionally touched zero or even turned negative. But once the sun sets, prices have routinely hit the INR 10,000 per MWh ceiling. On 11, 12, 13, 16, and 17 May, the market spent multiple evening hours at the maximum permissible price.

The implication is stark: India does not currently have enough flexible generation capacity to meet a peak that occurs after solar hours. Gas plants, which are ideal for this role, are largely idle due to fuel costs. Hydro can help, but reservoir constraints and environmental flows limit how much and how quickly it can ramp. Battery storage is still too small to make a meaningful difference.

Coal stocks: Aggregate stability, localised stress

The coal stock data, drawn from the daily reports of the Central Electricity Authority, reveals a paradox. In aggregate, the situation appears manageable. Total coal stock at power plants covered under the “TOTAL B” category stood at 53.7 million tonnes (mnt) on 1 May 2026, and declined to 52.3 mnt by 17 May — a drawdown of just 1.4 mnt or 2.6%.

However, aggregate figures can mask growing stress at individual plants.

While total stocks fell modestly, the number of plants classified as “critical” — typically those with stocks below 25% of normative requirements — more than doubled from 8 to 19. The drawdown was not spread evenly across the fleet. It was concentrated in plants that were already low, pushing them across the critical threshold.

Telangana has been the epicentre of the coal stress. On 1 May, three plants in the state were already critical. By 17 May, five of Telangana’s six monitored plants were in the critical zone, with stock levels ranging from 13% to 26% of normative. Tamil Nadu also saw its critical count increase, with North Chennai and Mettur joining the list.

The contrast with well-stocked plants is striking. NTPC’s large pithead stations — Rihand, Singrauli, Korba, Vindhyachal — continue to hold 80-140% of normative stock. These plants have drawn down little because their location and dedicated supply chains insulate them from the logistics crunch affecting others.

The Buxar TPP, operated by SJVNL, presents the most alarming data point. Its stock level fell from 15% of normative to zero per cent over just seventeen days. The plant has effectively exhausted its coal inventory and is now running on a d-o-d basis.

Connecting the dots: A system under stress

The trends across demand, generation, coal stocks and exchange prices are closely interconnected. The heatwave pushed up evening demand, which in turn exposed the gap in post-solar generation capacity. Thermal plants increased output to bridge the shortfall, leading to higher coal consumption and falling inventories at several stations.

As stock positions tightened, some generators became more cautious in offering power on the IEX, contributing to tighter supply conditions and higher exchange prices. As prices reached the market ceiling, a portion of demand remained unmet. The unmet exchange volumes likely translated into supply shortfalls for industrial users, commercial consumers and households across several regions.

The system has not collapsed, but it is operating without meaningful buffers. The evening peak has been met largely because discoms have resorted to load shedding — whether formally or through voltage reductions — and because some large industrial consumers have voluntarily curtailed operations during peak hours. The IEX data captures only the bids that did not clear.

Outlook

The next two weeks of May will be critical. Weather forecasts suggest the heatwave may persist, keeping evening demand elevated. Coal India has been asked to prioritise rakes to Telangana and Tamil Nadu, but logistics take time. The gas-based fleet remains expensive to run, and no policy intervention can change that quickly.

What the May 2026 data ultimately reveals is that India’s power sector has outgrown its current flexibility. The rapid expansion of solar generation has been a remarkable success, but it has created a new vulnerability: an evening peak that must be met by other sources. Until battery storage scales up, or until gas becomes more affordable, or until demand response programmes become more sophisticated, the evening hours will remain the most dangerous time for the grid.

Leave a Reply