- Gujarat’s acreage falls 14% y-o-y in 2025-26, production to drop 13%

- Large carry-forward stocks from bumper 2023-24 crop caps price rise

- Cumin exports decline sharply as Chinese buyers stay on sidelines

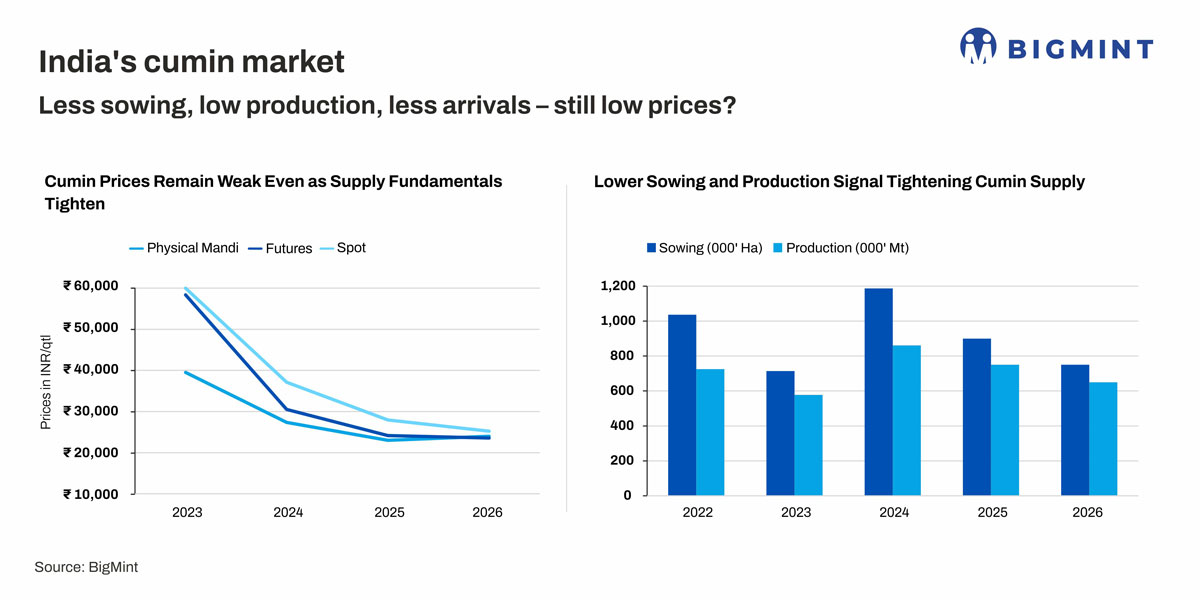

Morning Brief: India’s spot cumin (jeera) prices moved largely within a range of INR 19,500-22,000/quintal (qtl) during January-April 2026 despite lower sowing, falling production, and thinner mandi arrivals. This is because large carry-forward stocks and weak export demand continue to outweigh tightening fresh crop supplies.

Notably, year-to-date spot prices till 15 May 2026 averaged around INR 22,000/qtl, around 12% lower than the 2025 average of INR 25,000/qtl. The 2026 average is also 63% lower than 2023’s INR 60,000/qtl, though production is expected to fall to 650,000 tonnes (t) this year, the lowest since 577,000 t in 2023.

India’s cumin production tightens

India’s cumin sowing declined to around 750,000 hectares (ha) in 2025-26 from 900,000 ha last year and 1.2 million ha in 2023-24. Production is projected at around 650,000 t in 2025-26 against 750,000 t in 2024-25 (13% lower y-o-y) and 860,000 t during the bumper 2023-24 season.

The decline in 2025-26 has been driven primarily by acreage contraction in Gujarat, India’s highest-yielding cumin-producing state. Gujarat’s acreage reportedly fell nearly 14% y-o-y to around 408,000 ha due to excess soil moisture during sowing, delayed field preparation, and weaker farmer sentiment after the sharp correction from the historic 2023 rally. Relatively lower returns compared with competing crops such as mustard and castor also discouraged sowing.

Weather disruptions further affected productivity. Excess moisture impacted germination and crop establishment in several producing regions, while irregular temperatures during vegetative growth reduced yield potential. Rajasthan acreage remained relatively stable, but lower productivity there failed to offset Gujarat’s decline.

Additionally, physical mandi arrivals during January-April 2026 declined by 5% to around 209,000 t compared with 220,500 t in the corresponding period in 2025, indicating tighter fresh crop inflows across key markets.

Another important factor limiting arrivals is that many farmers are currently holding stocks instead of aggressively selling in mandis as prices near INR 19,500-21,000/qtl are considered unattractive compared with the historic highs recorded during 2023.

Why has lower production failed to lift Indian cumin prices?

Prices have remained largely subdued due to substantial carry-forward stocks and weak export demand.

The most important factor weighing on prices is the large quantity of old-crop inventory accumulated after the bumper 2023-24 harvest, when low stocks and aggressive exports pushed cumin prices close to INR 60,000/qtl. The market is currently cushioned by heavy carry-forward inventories, estimated at around 100,000-120,000 t.

Carry-forward stocks, which had fallen to just 5-7 lakh bags (1 bag is equal to 55 kilograms) during the historic 2022-23 rally, expanded significantly after exceptionally high prices in 2022-23 encouraged record sowing in 2023-24. Market participants estimated carry-forward stocks at around 16-20 lakh bags entering the 2025-2026 season.

Meanwhile, although arrivals in January-April 2026 remain 5% lower y-o-y, they are around 80% higher than the 116,800 t recorded in 2023.

Weak export demand has further limited price recovery and the absorption of large carry-forward stocks. India’s cumin exports, which surged to a record 413,900 t in 2024 during a global supply squeeze, declined sharply to around 196,400 t in 2025.

Export weakness has continued into 2026, with January-March shipments falling to just 31,200 t compared with 46,700 t in the corresponding period last year and more than 102,000 t in 2024.

China’s reduced buying activity has emerged as one of the key reasons behind the slowdown. Chinese buyers, who played a major role in the historic cumin rally, are currently relying more on domestic production and inventories accumulated during the previous high-price cycle.

At the same time, several buyers in the Middle East and Europe remain cautious due to geopolitical uncertainty, elevated freight costs, and slower downstream demand.

Global supply fundamentals otherwise remain supportive for Indian cumin. Competing origins such as Syria, Iran, Afghanistan, and Turkiye, which together account for nearly 25-30% of global cumin supply, continue to face disruptions from geopolitical tensions, weather stress, and trade-related uncertainties.

Outlook

BigMint expects Indian cumin prices to continue moving within the INR 19,000-22,000/qtl range in this quarter unless export demand recovers meaningfully or inventories decline faster than expected.

Over the medium term, however, prolonged low prices could eventually tighten the market again by discouraging acreage expansion during the next sowing season. Historically, cumin acreage has remained highly sensitive to farmers’ price realisations, raising the possibility that India could gradually move into another supply-tightening cycle once existing inventories normalise.

Leave a Reply