- 17 Bangladeshi yards secure IMO compliance

- Vessel availability remains limited across South Asia

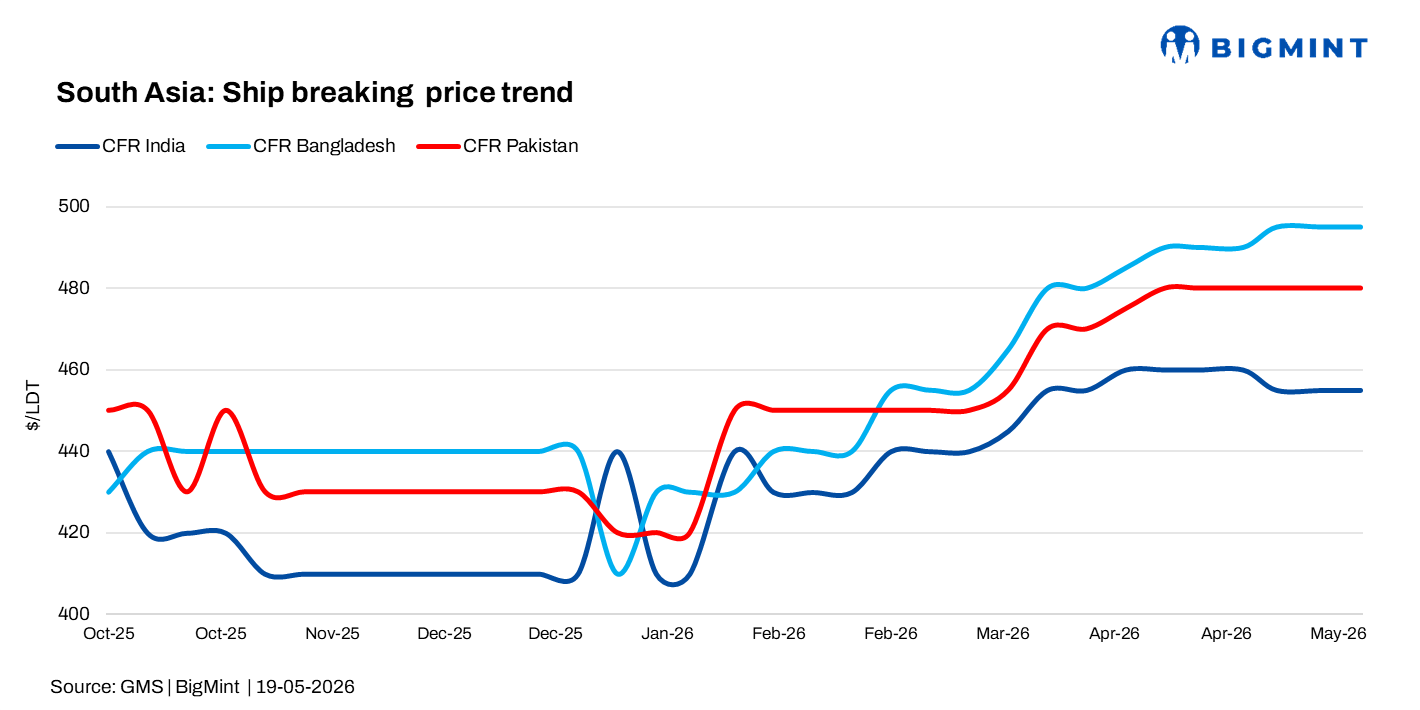

South Asia’s ship recycling markets remained cautious in week 20 as currency volatility, elevated crude prices, and tightening monsoon timelines continued to shape regional sentiment. While India faced rupee weakness, Bangladesh benefited from compliance growth, and Pakistan saw relative FX stability.

India: INR hits record low amid crude-led pressure

USD/INR fell to a fresh all-time low, extending the rupee’s weakening trend as earlier gains were fully reversed amid renewed geopolitical tensions and delayed de-escalation hopes. RBI intervention remains limited, leaving the currency more exposed to external pressures.

Elevated Brent crude prices above $100 and tightening global oil supply conditions continue to weigh on India’s import outlook. Locally, Alang steel plate prices stayed range-bound at INR 39,800-40,500/t, keeping India competitively positioned in USD terms versus regional peers. However, despite pricing advantage and strong compliance credentials, vessel inflows remain subdued ahead of the narrowing monsoon window, with sentiment largely cautious.

Bangladesh: Stable market amid firm currency, smoother LC flow

Bangladesh maintained stable market conditions, supported by a firm USD/BDT exchange rate, smoother LC settlements, and steady domestic steel plate prices at BDT 69,100-71,000/t.

The country also strengthened its global position after the IMO officially recognised 17 Bangladeshi yards under the Hong Kong Convention, making Bangladesh the world’s second-largest compliant ship recycling nation after Turkiye.

Yard owners invested around BDT 2,000 crore in environmental and safety upgrades, reinforcing Chattogram’s position as a major green recycling hub. However, vessel imports remained weak despite the rapid rise in compliant facilities.

Pakistan: PKR stabilises after rate hike amid firm sentiment

Pakistan’s rupee strengthened slightly against the USD in week 20, outperforming regional peers where both INR and TRY hit or remained near record lows. The move reflects support from the State Bank’s 100 bps rate hike to 11.5%, steady remittance inflows, and easing near-term FX pressure.

Rising oil import costs continue to strain the external account. In the ship recycling sector, Gadani prices held firm at PKR 190,000/t ($682/t), maintaining a premium over India in USD terms. However, vessel inflows remain muted as the narrowing monsoon window continues to limit activity.

Leave a Reply