- Pithead stocks remained significantly above normal

- Rake loading bottlenecks pressured coal evacuation

India’s coal sector began the new fiscal year on a sluggish note, with both production and despatch recording year-on-year declines in April 2026. More significantly, the massive overhang of pithead inventory that had built up to a record 152 MnT by the end of March 2026 showed only marginal improvement during the month, keeping pressure on producers to accelerate off-take in the coming months.

Total coal production (including CIL, SCCL, and Captives) stood at 74.31 MnT in April 2026, down 9% from 81.66 MnT in April 2025. Despatch to all sectors also fell by 1.62% year-on-year to 86.20 MnT. With despatch exceeding production by nearly 12 MnT during the month, pithead stocks saw some drawdown, but remain at elevated levels that continue to weigh on mining operations and mine planning.

Record closing stock sets a difficult starting point

As reported earlier by bigMint, coal stock at mine pitheads had surged to an all-time high of approximately 152 MnT as of March 31, 2026 – the highest ever recorded for the end of any fiscal year. This unprecedented inventory accumulation was driven by a combination of strong production growth in the second half of FY’26, logistical bottlenecks, and tepid power sector offtake due to milder weather conditions.

Coming into April 2026, therefore, miners faced a dual challenge: they needed to both meet monthly production targets and simultaneously draw down the bloated inventory without exacerbating the stockpile further.

Production discipline or forced cut?

The sharp 9% decline in year-on-year production in April suggests that producers – particularly Coal India Ltd (CIL) – may have deliberately tempered output to align with despatch realities. Total production of 74.31 MnT in April was also significantly lower than the monthly target, indicating that the usual push to start the fiscal year on a high note was absent.

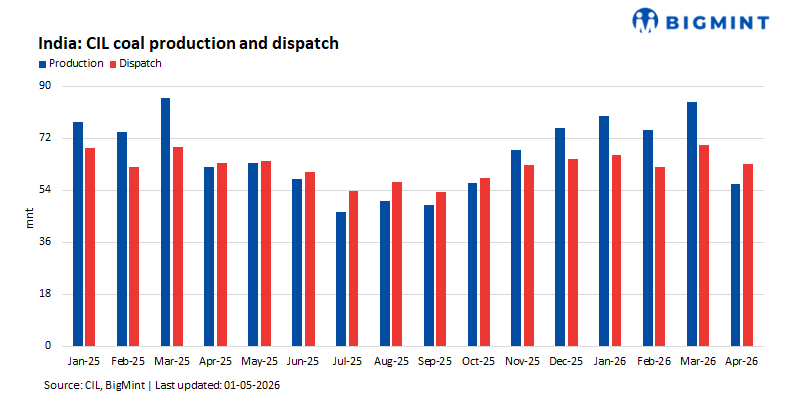

CIL, which accounts for over 75% of domestic output, produced 56.06 MnT in April 2026, missing its monthly target of 61.52 MnT and registering a 9.67% decline compared to 62.06 MnT in April 2025. This is a rare instance of CIL’s April output falling below the previous year’s level, underscoring the supply-demand mismatch that prevailed at the start of FY’27.

Among CIL’s subsidiaries, South Eastern Coalfields (SECL) was the sole exception, posting a 9.25% growth (15.32 MnT vs 14.02 MnT). In contrast, Mahanadi Coalfields (MCL) saw output drop 13.9% to 13.78 MnT, Northern Coalfields (NCL) declined by 23.67% to 9.33 MnT,

and Bharat Coking Coal (BCCL) suffered a steep 41.3% fall to just 1.99 MnT. SCCL and captive/other producers also reported lower output, down 19.15% and 2.68% respectively.

Despatch outpaces production but remains weak

Total coal despatch in April 2026 stood at 86.20 MnT, exceeding production by about 12 MnT. This gap – the widest in recent months – allowed for some reduction in pithead stocks. However, despatch itself was down 1.62% year-on-year, indicating that demand-side conditions were not strong enough to make a significant dent in the 152 MnT opening inventory.

A quick estimate suggests that with production of 74.31 MnT and despatch of 86.20 MnT, the net drawdown during April would be roughly 11.9 MnT. This would bring closing pithead stock as of April 30, 2026, to approximately 140 MnT – still an extraordinarily high level, about 30-35% above normal operating norms for this time of year.

Power sector offtake, which accounts for nearly 80% of total despatch, fell 2.22% year-on-year to 68.65 MnT. This was the primary reason behind the muted overall despatch growth. CPP (Captive Power Plants) offtake dropped sharply by 22.63% to 4.75 MnT, and steel segment despatch collapsed 35.49% to 1.08 MnT. Cement offtake also declined 21.13% to 0.78 MnT.

On a brighter note, sponge iron despatch rose 17.73% to 0.96 MnT, and the others category – which includes various industrial users – grew by an impressive 28% to 9.99 MnT. Non-regulated sector (NRS) despatch inched up 0.81% to 17.55 MnT, offering a sliver of comfort in an otherwise subdued demand picture.

Top mines underperform, adding to inventory pressure

Performance at the top 35 mines – which collectively account for a large share of CIL’s output – was underwhelming. These mines produced 41.20 MnT against a monthly target of 45.13 MnT, achieving only 91.28% of the goal. While MCL’s Bhubaneswari OC (138.7%) and SECL’s Chhal OC (137.1%) exceeded targets, several large mines lagged badly. NCL’s Block B OC achieved just 21.33% of its target, while MCL’s Jagannath OC managed a mere 1.95%.

Overburden removal (OBR) in top 35 mines stood at 105.59 million cubic meters, achieving 99.34% of target, with 19 mines exceeding 100%. The contrast between OBR achievement and production shortfall suggests that mine preparation activities remained robust, but actual coal extraction was tempered – possibly to avoid adding to already overflowing stockyards.

Rake loading remains a bottleneck

Daily average rake loading for all sectors in April 2026 was 313.1 rakes, achieving only 78.3% of the planned 400 rakes per day, and down 3% from 322.8 rakes per day in April 2025. SECL was the only major to improve (+6.65%), while BCCL saw a steep 29% decline in rake loading. For

the power sector specifically, daily average rakes dropped to 274.5 from 285.1 a year earlier, with BCCL again recording a 42% plunge.

The persistent gap between planned and actual rake loading remains a structural challenge. Even if production is moderated, the ability to evacuate coal from pitheads – especially from high-stock mines in Odisha, Chhattisgarh, and Jharkhand – will determine how quickly inventory normalises.

What does this mean for the coming months?

Closing pithead stock of roughly 140 MnT at the end of April 2026 is still nearly double the comfortable level of 70-80 MnT that miners typically target. For context, the government’s normative stock for pitheads is around 30 days of production, which for CIL alone would translate to about 55-60 MnT.

Unless despatch accelerates sharply in May and June – traditionally pre-monsoon months when power demand peaks – miners may be forced to continue moderating production well into the first quarter of FY’27. This would likely keep year-on-year production growth in negative territory for at least another month or two.

The coming weeks will be critical. Power generation data for April already shows coal-based generation up only 2.4% year-on-year, while renewables grew 22%. If this trend continues, the coal sector’s inventory overhang could persist longer than anticipated, posing a challenge not just for miners but also for logistics providers and power utilities.

Leave a Reply