- Australia remains largest import source

- Steel mills reduce spot procurement

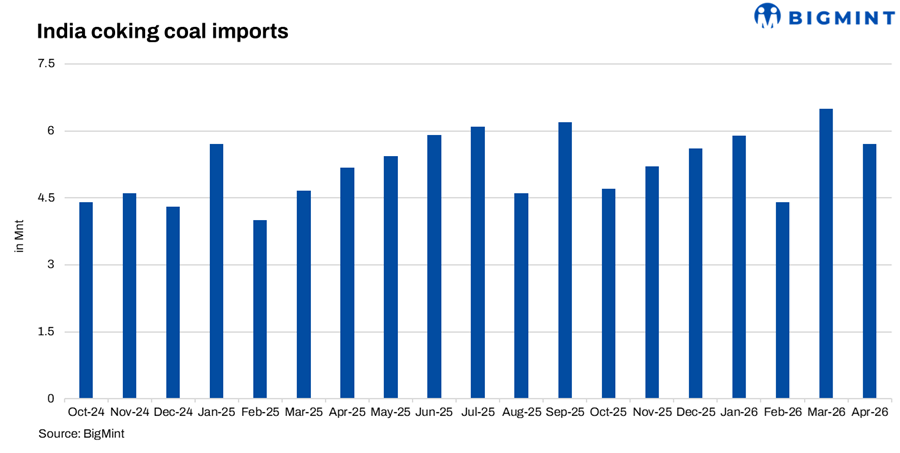

India’s coking coal imports declined 12% m-o-m to 5.7 mnt in April from 6.5 mnt in March as steel mills adopted cautious procurement strategies amid mixed steel demand and comfortable inventory levels due to higher imports in March. However, imports increased 10% y-o-y compared with 5.2 mnt in April, supported by continued dependence on imported premium coking coal for blast furnace operations. Lower arrivals from Australia and Mozambique mainly pulled down monthly import volumes, while higher shipments from Russia and the US partially offset the decline.

Australia shipments decline, Russia and US rise

Australia remained India’s largest coking coal supplier in April despite imports declining 19% m-o-m to 2.5 mnt from 3.1 mnt in Mar’26. Volumes were also down 17% y-o-y compared with 3 mnt in April’25. Market participants attributed the decline to tighter cargo availability, extended shipping delays higher freight costs and cautious buying from Indian steel mills. Delayed North Goonyella cargoes are expected to arrive in India late April/May, which may push up the volumes.

Russia emerged as the second-largest supplier, with imports increasing 13% m-o-m to 1.7 mnt from 1.5 mnt and surging 143% y-o-y from 0.7 mnt in April’25. Competitive pricing and shorter voyage durations continued supporting Russian cargo inflows.

US shipments increased 33% m-o-m to 1.2 mnt from 0.9 mnt and were also up 33% y-o-y. Meanwhile, Mozambique imports declined sharply 67% m-o-m to 0.2 mnt from 0.6 mnt and were down 33% y-o-y compared with April’25. Indonesia imports eased 50% m-o-m to 0.1 mnt, while Canadian and Colombian cargoes remained negligible during the month.

JSW Steel remains top importer

JSW Steel remained India’s largest coking coal importer in April, with imports increasing 20% m-o-m to 1.8 mnt from 1.5 mnt in March and rising 50% y-o-y compared with 1.2 mnt in April’25. Strong blast furnace utilisation and steady steel production supported higher procurement.

In contrast, Tata Steel imports declined 40% m-o-m to 0.9 mnt from 1.5 mnt, although volumes remained 13% higher y-o-y. SAIL imports also fell 38% m-o-m to 0.8 mnt from 1.3 mnt and were down 11% y-o-y compared with April’25.

Steel demand and freight costs shape market

BigMint’s Coking Coal Index, CNF Paradip, India, witnessed mixed movements during early 2026 as global supply conditions, freight costs and steel sector sentiment influenced the market. The index averaged around $250/t in Jan’26 before increasing to nearly $260.25/t in February, supported by firmer Australian PHCC prices, improving buying interest from Asian steel mills and rising vessel freights. However, the average softened slightly to around $252/t in March as Indian buyers adopted cautious procurement strategies amid weak finished steel demand and comfortable inventory positions.

Despite the temporary correction in March averages, coking coal sentiment remained broadly firm due to limited availability of premium-quality Australian cargoes and elevated replacement costs. The market again strengthened in May, with BigMint’s Coking Coal Index remaining stable w-o-w at $266/t as on 15 May. The recent support mainly came from higher bunker prices, rising Australia-India vessel freights and expectations of mining and berthing delays at key Australian coal operations. Market participants also indicated that tight prompt cargo availability continued supporting seller confidence, although cautious downstream steel demand in India limited aggressive spot buying activity.

Steel mills maintained cautious procurement during April amid mixed finished steel demand and elevated raw material costs. Trade-level BF rebar prices declined around INR 1,500/t w-o-w to INR 57,500/t ex-Mumbai during the period, reflecting weak buying interest and higher distributor inventories. Steel-grade pig iron prices in Durgapur were heard around INR 38,750/t ex-works, although procurement sentiment remained selective.

At the same time, rising freight costs continued supporting imported coking coal prices. Australia-India vessel freights from Hay Point to Paradip increased around $2.1/dmtu w-o-w to $26.1/dmtu, while bunker prices rose to nearly $835/t. Australian PHCC prices were also assessed around $240/t FOB Australia, keeping replacement costs elevated for Indian steel mills.

Meanwhile, Russian cargoes continued attracting buyers due to relatively competitive pricing compared with Australian premium hard coking coal, helping Russia increase its share in India’s import basket during April.

Outlook

India’s coking coal imports are expected to remain stable-to-firm in the near term, supported by steady blast furnace operations and dependence on imported premium-grade coal. However, higher freight costs, cautious steel demand and comfortable inventory positions may continue limiting aggressive spot bookings. Supply conditions in Australia and pricing competitiveness of Russian cargoes are likely to remain key factors influencing future import trends.

Leave a Reply