- Strong Kanto tender supports Japanese scrap sentiment

- Vietnamese mills cautious amid ample inventories

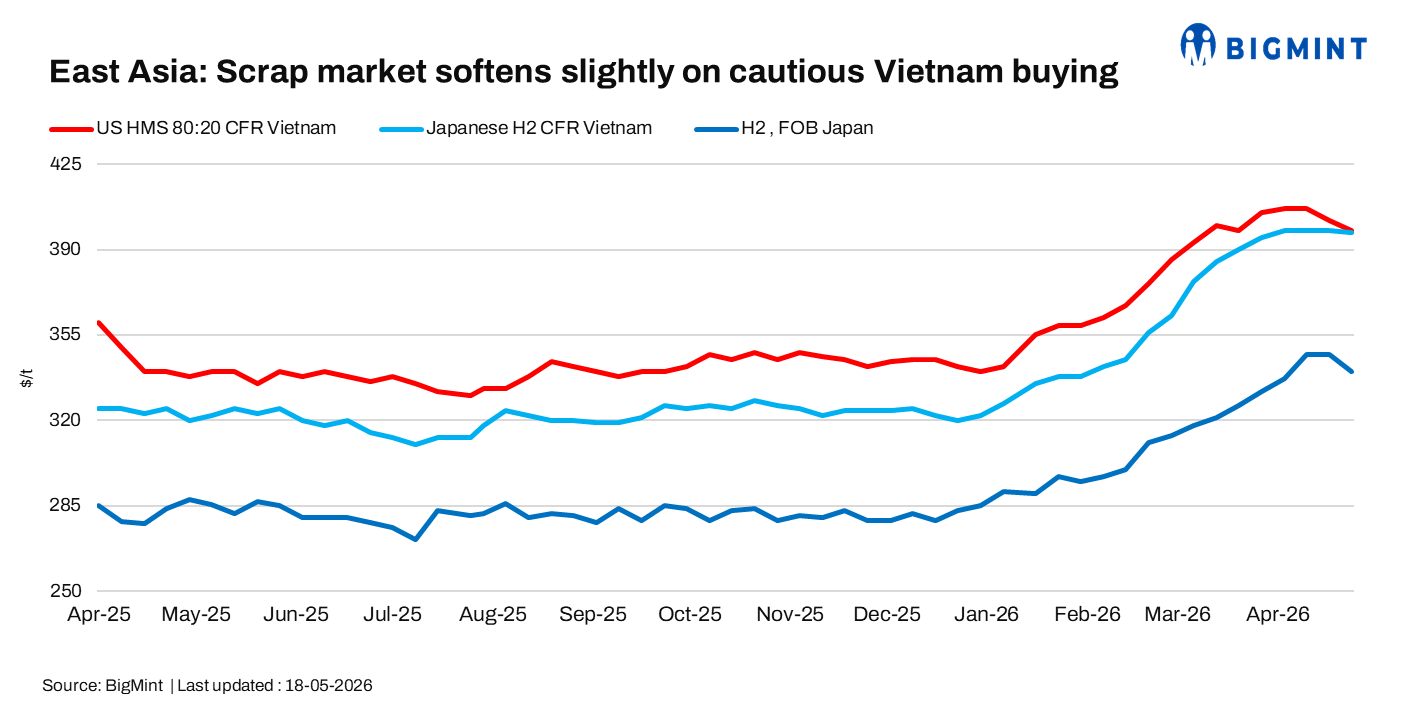

East Asian ferrous scrap markets remained slightly softer in the week ended 18 May, as cautious Vietnamese buying and more competitive deep-sea bulk offers continued pressuring import prices.

Stronger domestic demand, higher collection prices, and a firmer May Kanto tender supported Japanese domestic scrap sentiment. However, comfortable inventories and weak downstream steel demand in Vietnam continued limiting fresh imported scrap bookings.

Weekly assessments

- Japanese H2 scrap was at $397/t CFR Vietnam, down by $1/t w-o-w.

- H2 scrap was at JPY 54,000/t ($340/t) FOB Tokyo Bay, down by JPY 400/t ($3/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $398/t CFR Vietnam, down by $4/t w-o-w.

Japan

Japanese scrap export sentiment remained slightly softer during the week as cautious overseas buying pressured prices despite stronger domestic demand and higher collection prices. H2 offers to Vietnam were heard at $390-402/t CFR.

The May Kanto H2 tender rose for the tenth consecutive month to JPY 54,602/t ($347/t) FAS for a 10,000 t cargo, up JPY 273/t m-o-m, supporting exporter confidence despite concerns over weaker demand during the upcoming rainy season in Vietnam and Bangladesh.

Tokyo Steel further supported domestic sentiment by raising scrap purchase prices by JPY 1,000/t ($6/t) from 13 May, taking H2 prices to JPY 54,000/t ($340/t). H2 FAS collection prices were heard at JPY 53,000-54,000/t ($334-340/t), while H2 scrap was assessed at JPY 54,000/t ($342/t) FOB Tokyo Bay, down JPY 400/t ($3/t) w-o-w.

Vietnam

Vietnamese mills remained cautious as most buyers were already covered for June shipments and shifted focus to July requirements. Ample inventories, weak steel demand, and more competitive local scrap continued limiting imports.

Meanwhile, deep-sea bulk scrap prices softened, with US and Australian-origin HMS 80:20 offers heard at $400/t CFR Vietnam, down $4-5/t w-o-w, while bids remained at around $395/t CFR.

Outlook

Japanese scrap prices are expected to remain supported by firm domestic demand and higher collection prices. However, cautious Vietnamese procurement, sufficient inventories, and competitive deep-sea cargo offers may continue limiting export price upside in the upcoming days.

Leave a Reply