- Domestic coal availability stayed comfortable via frequent auction

- Freight rates strengthened on tighter vessel availability

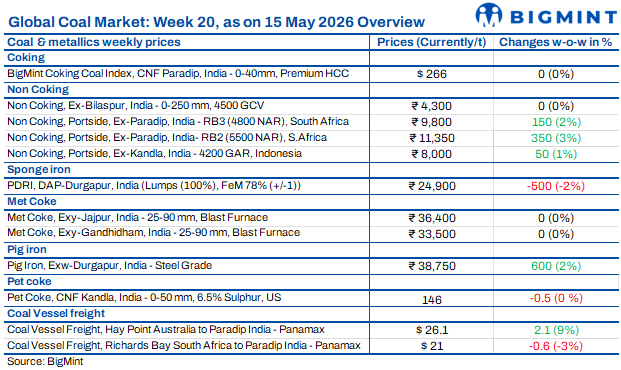

India’s coal market sentiment remained subdued this week as weak sponge iron, steel and cement demand continued limit buying activity across imported and domestic segments. Buyers largely preferred requirement-based procurement amid comfortable coal availability, rising port inventories and frequent domestic auctions. Imported coal markets stayed supported by higher freight costs and tighter global availability, but downstream industries resisted aggressive purchases due to weak margins and expectations of softer prices ahead of the monsoon season.

Indonesian coal prices climbed at ports

Indian portside Indonesian thermal coal prices increased INR 100-400/t w-o-w by 15 May, supported by rupee weakness, higher freight rates and tight spot cargo supply. The rupee hovered near INR 96/$, raising import parity costs. At Kandla, 5,000 GAR coal stayed stable at INR 10,300/t, while 4,200 GAR prices rose INR 50/t to INR 8,000/t. Lower-grade 3,400 GAR coal increased INR 250/t to around INR 6,100/t at Navlakhi. Supramax freight from East Kalimantan to Navlakhi climbed $2.1/t to nearly $21.5/t. Meanwhile, India’s thermal power plant coal stocks stood at 53 mnt, equivalent to around 17 days of consumption, keeping overall supply conditions comfortable.

Buyers resisted high import offers

South African thermal coal prices at Indian ports stayed under pressure in the week ended 14 May despite firm global cues and higher freight rates. Ex-Paradip RB2 (5,500 NAR) prices rose INR 350/t w-o-w to INR 11,350/t, while RB3 (4,800 NAR) increased INR 150/t to INR 9,800/t. However, trading activity remained weak as buyers resisted high landed costs amid weak sponge iron demand and comfortable domestic coal supply. PDRI DAP-Durgapur prices fell INR 500/t to INR 24,900/t. Domestic non-coking coal prices declined INR 250-300/t, while portside inventories rose 4.8% w-o-w to 15.87 mnt, the highest level in 25 weeks, limiting fresh import bookings and keeping sentiment subdued.

Domestic coal prices stayed stable

India’s domestic non-coking coal prices remained largely stable w-o-w amid weak sponge iron demand and comfortable supply. BigMint assessed 5,000 GCV coal at around INR 6,000/t, while 4,500 GCV material stayed near INR 4,300/t. Buyers continued restricting purchases to immediate requirements, keeping trade activity slow across major regions. Frequent CIL auctions improved coal availability and reduced urgency for spot buying, with over 20 mnt planned for auction in May under the SWMA calendar. Meanwhile, MCL’s 9 May road-mode auction showed improved participation, with around 927,000 t allocated against 4.36 mnt offered. However, lower premiums in recent SECL and MCL auctions continued pressuring overall market sentiment despite healthy participation in better coal grade.

NAPP trade stayed active in India

India’s US-origin NAPP thermal coal market remained active in early May as steady retail lifting and higher west coast inventories supported trade. Weekly lifting increased to 112,392 t in Week 19 from 91,962 t in Week 18, while port stocks rose to 435,654 t from 314,037 t in Week 17 due to higher cargo arrivals. Ex-Kandla prices for 6,900 NAR US coal declined INR 300/t w-o-w to INR 13,400/t. Offers for May-loading cargoes were heard in the low-to-mid $130s/t CFR range. However, competition from petcoke, domestic coal, Russian coal and South African material remained strong. Despite rising inventories, lifting stayed near 100,000 t/week, indicating stable downstream industrial and retail demand.

Imported met coke bookings increased

Imported BF-grade met coke prices into India remained largely stable w-o-w amid cautious downstream demand. Indonesian suppliers increased FOB offers following DGTR’s proposal to reduce anti-dumping duty on imported met coke. Three deals were reportedly concluded at $269-271/t FOB, while BigMint assessed Indonesian-origin BF-grade coke (65/63 CSR) at around $302/t CFR India, up $2/t w-o-w. Domestic BF coke prices stayed stable at INR 36,400/t ex-Jajpur and INR 33,500/t ex-Gandhidham. Meanwhile, Australian PHCC prices increased $7/t w-o-w to $240/t FOB Australia, supporting coke production costs. On the downstream side, steel-grade pig iron prices in Durgapur rose INR 500/t to INR 38,500/t, although buying sentiment remained cautious amid weak steel demand.

Coking coal prices stayed supported

BigMint’s PHCC index remained stable w-o-w at $266/t CNF Paradip on 15 May, near a three-month high, supported by higher freight rates and tightening supply sentiment. Market participants reported limited offers amid expectations of supply tightness due to mining and berthing delays at an Australian miner. Australia-India vessel freights increased $2.1/dmtu w-o-w to $26.1/dmtu from Hay Point to Paradip, while bunker prices rose $8/t to $835/t.

Coal competition pressured petcoke demand

High-sulphur petcoke prices into India declined for the third consecutive week as cement producers preferred cheaper thermal coal alternatives. Imported petcoke offers were heard around $145-150/t CFR India, while Saudi and Oman-origin cargo discussions were reported at $140-143/t CFR. However, buying activity remained weak due to poor cement demand, ample fuel coverage and expectations of further price corrections. US NAPP 6,900 NAR coal offers into India’s west coast were heard in the low-to-mid $130s/t CFR range, making coal more economical than petcoke. Buyers increasingly preferred US NAPP, Russian and domestic coal due to better pricing and availability. Despite Middle East supply disruptions, coal competition continued limiting imported petcoke demand and keeping market sentiment subdued.

Domestic petcoke market stayed mixed

India’s domestic petcoke prices remained mixed in May 2026 as weak cement demand and cheaper coal alternatives limited buying interest. IOC and BPCL kept prices stable after April hikes, with IOC road prices remaining at INR 17,660/t at Koyali and INR 18,920/t at Panipat, while BPCL held Bina prices at INR 19,000/t. In contrast, Nayara increased prices sharply by INR 1,330/t m-o-m to INR 21,000/t, while CPCL raised offers INR 1,360/t to INR 19,750/t. Supply concerns linked to refinery shutdowns and West Asia tensions supported sentiment. Meanwhile, imported US petcoke prices softened, with CNF Kandla assessed near $146.6/t amid weak enquiries and subdued industrial demand.

Coal freights remained mixed to India

Dry bulk coal freights to India showed mixed trends in the week ended 15 May as Australia-India Panamax routes increased on healthy coal enquiries and tight prompt vessel availability, while Indonesia-India Supramax rates gained amid limited tonnage in Southeast Asia. However, overall fixing activity remained slow despite firmer freight sentiment. Market participants stated that rising bunker costs continued pressuring freight rates. Bunker prices increased $8/t w-o-w to $835/t on 15 May. The Baltic Dry Index also surged 161 points w-o-w to 3,195, reaching a more than five-month high, supported by tighter vessel availability and stronger bulk cargo movement. Meanwhile, Indonesia-India freight sentiment stayed weak compared with stronger Indonesia-China demand.

Leave a Reply