- Australia-India vessel freights increase by over $2/dmt w-o-w

- Key Australian miner heard to be facing mining, berthing delays

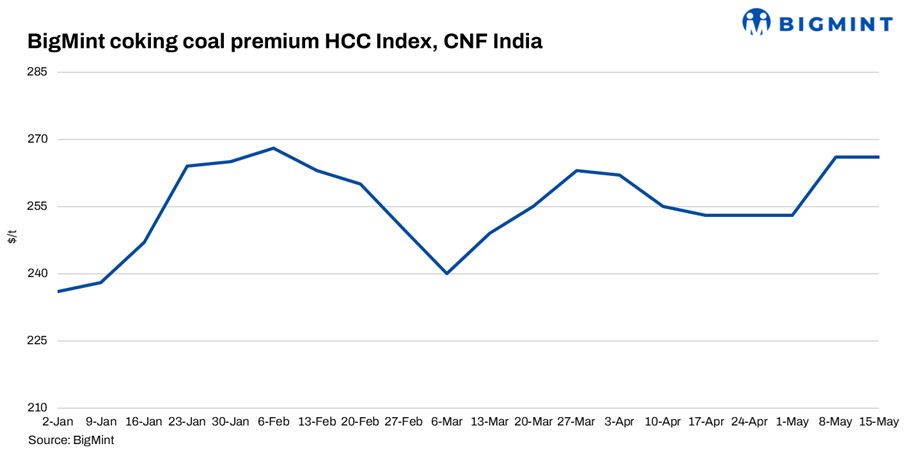

BigMint’s premium hard coking coal (PHCC) index was assessed at $266/tonne (t) CNF Paradip, India, on 15 May 2026, remaining stable w-o-w amid higher freights and tightening supply sentiment. The index remains close to a three-month high, with similar levels last seen in early February, as per data maintained with BigMint.

Market participants indicated that traders were attempting to push coking coal prices higher amid tightening sentiment. Offers were limited, and there were expectations of tight supply due to berthing and mining delays from an Australian miner.

Market chatter suggested a possible trade for Australian PHCC at around $262-264/t CFR India; however, the deal could not be independently confirmed at the time of reporting. Meanwhile, premium hard coking coal indices were heard around $239/t FOB for premium low-volatility (PLV) material.

BigMint has consolidated its PHCC CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia — normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors influencing prices

Australia-India vessel freights inch up: Dry bulk coal freights from Australia to India increased in the week ended 15 May amid healthy demand. Bunker prices rose by $8/t w-o-w to $835/t as of 15 May, from $827/t a week earlier, supported by firmer crude oil trends and steady demand across key bunkering hubs. Following this, vessel frights from Hay Point to Paradip rose $2.1/dmtu w-o-w to $26.1/dmtu.

India’s met coke prices remain supported, import bookings pick up: India’s blast furnace (BF)-grade metallurgical coke prices remained largely stable w-o-w as of 14 May, supported by balanced supply-demand dynamics and elevated import parity levels. In the eastern region, BF coke prices were steady at INR 36,400/t ex-Jajpur, while western India prices held at INR 33,500/t ex-Gandhidham amid firmer replacement costs and stronger imported coke offers. Foundry-grade (+90 mm) coke prices also remained unchanged at INR 36,400/t ex-Rajkot, reflecting stable procurement from the casting and foundry sectors.

Following the Directorate General of Trade Remedies’ (DGTR) proposal to reduce anti-dumping duty on imported met coke, Indonesian suppliers reportedly increased FOB offer levels sharply, anticipating stronger Indian buying interest. BigMint learnt that three deals were concluded by end-users at $269-271/t FOB levels. Consequently, landed costs for Indian buyers moved higher, with BigMint assessing Indonesian-origin BF-grade coke (65/63 CSR) at around $302/t CFR India, up $2/t w-o-w.

Indian BF rebar prices decline on weak inquiries, rising inventories: Trade-level BF rebar prices (distributor to dealer) declined by INR 1,500/t ($15/t) w-o-w to INR 57,500/t ($600/t) exy-Mumbai. Demand remained average across major regions, while northern India continued to witness weaker buying interest, according to sources. Higher inventory availability with distributors kept procurement cautious at prevailing prices, resulting in a mixed sentiment during the week. Meanwhile, rebar project deals were reported at INR 57,000-57,500/t ($594-600/t) on landed basis.

Outlook

Coking coal prices are likely to remain supported next week and may inch up slightly on an expected hike in freight rates.

Leave a Reply