- Lower auction premiums pressure prices

- Frequent auctions improve coal availability

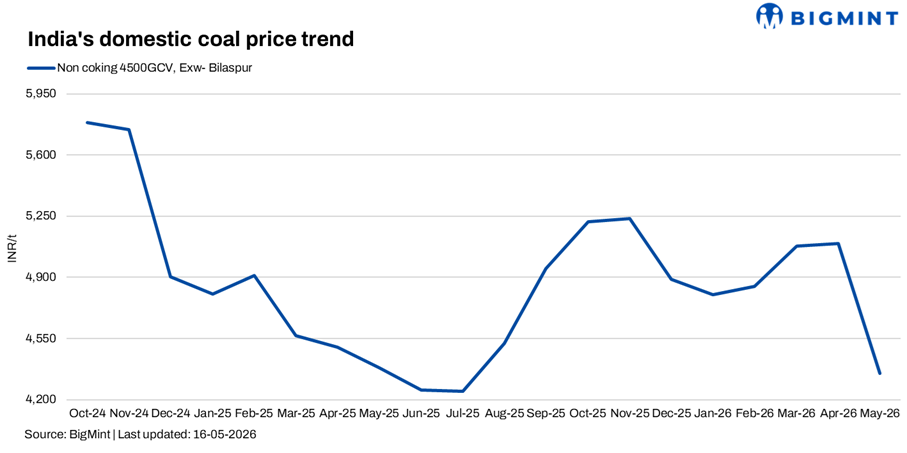

India’s domestic non-coking coal prices remained largely stable w-o-w amid subdued buying activity and comfortable coal availability. As per BigMint’s assessments, 5,000 GCV coal prices were heard at around INR 6,000/t, while 4,500 GCV material remained near INR 4,300/t.

Market participants stated that weak sponge iron and steel demand continued to pressure the domestic coal market, with most buyers restricting procurement to immediate requirements. Trade activity remained slow across major coal-consuming regions, while buyers continued resisting aggressive price increases despite occasional firm offers.

Participants also noted that lower premiums in recent SECL and MCL auctions kept overall domestic market sentiment under pressure, as regular auction volumes ensured sufficient coal availability in the market.

Frequent auctions improve coal availability

Coal India subsidiaries continued conducting frequent e-auctions during May, improving overall coal availability and limiting panic buying sentiment. As per the May 2026 Single Window Mode Agnostic (SWMA) auction calendar, CIL subsidiaries collectively planned to auction more than 20 mnt of coal during the month across rail and road modes.

Market participants stated that regular auction schedules and comfortable domestic supply reduced urgency for fresh spot purchases. Buyers remained highly selective and price sensitive, especially for lower and mid-grade coal.

However, despite comfortable coal availability, logistics continued to remain a major concern for private consumers.

Concerns regarding diesel availability also emerged in the market. Participants indicated that if the diesel shortage situation persists, domestic coal offers may increase in the coming weeks due to rising transportation costs.

MCL auction sees improved participation

Mahanadi Coalfields Limited’s road-mode non-coking coal auction held on 9 May reflected improved participation compared with the previous auction. Around 927,000 t were allocated against offered volumes of nearly 4.36 mnt, more than double the allocation recorded in the previous 30 April auction.

G12 coal dominated allocations with relatively healthy premiums, while G8 continued attracting the highest premium levels due to sustained demand for better-quality coal. G11 also witnessed strong participation, whereas G14 premiums remained subdued, reflecting cautious bidding sentiment in lower grades.

Buyer participation broadened across industrial and trading segments, with companies such as Rungta Mines, JSW Energy, Tata Steel, Sanish Ventures, and Vedanta Ferro Alloys Corporation actively participating across G11, G12, G13, and G14 grades.

Despite improved auction participation, market sentiment largely remained balanced, with buyers continuing selective procurement strategies amid weak downstream steel and sponge iron demand.

Outlook

Domestic coal market sentiment is expected to remain cautious in the near term amid subdued industrial demand and comfortable coal availability. Frequent CIL auctions and lower premiums are likely to continue limiting sharp price increases.

However, logistics-related challenges such as rake shortages and possible diesel supply issues may support offers in some regions if transportation costs rise further. Buyers are expected to continue requirement-based procurement until stronger recovery is seen in sponge iron and steel demand.

Leave a Reply