- Buyers resist elevated import offers

- Port stocks hit highest level in 25 weeks

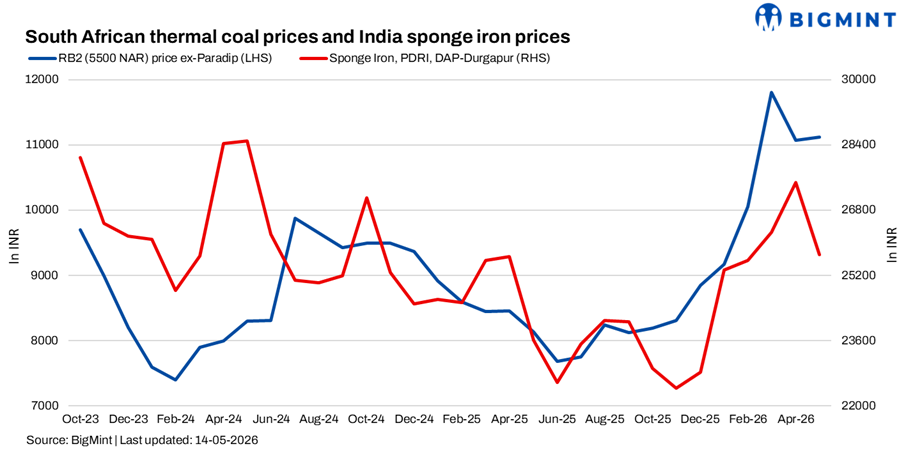

South African thermal coal prices at Indian ports remained under pressure during the week ended 14 May despite firm global energy cues, rising freight costs, and higher international offers. Market sentiment stayed weak as buyers resisted elevated landed prices amid poor sponge iron demand, abundant domestic coal availability, and rising port inventories.

As per BigMint’s assessment, ex-Paradip RB2 (5,500 NAR) prices increased by around INR 250/t w-o-w to INR 11,300/t, while RB3 (4,800 NAR) prices rose marginally by INR 50/t to around INR 9,750/t. However, despite the increase in assessed prices, actual market activity remained extremely limited with very few workable transactions in the market. Wide bid-offer disparities led to limited transactions.

Global offers soften but buyers remain cautious

Trade activity in the FOB market reflected a widening disconnect between sellers and buyers. Offers for South African 5,500 NAR coal in Panamax parcels reportedly declined w-o-w to $94-96/t FOB RBCT for June-loading cargoes, while a Supramax parcel was heard around $96/t FOB. However, Indian buyers were largely bidding in the range of $89-93/t FOB.

Despite some correction in FOB offers, Indian buyers continued resisting imports due to weak downstream economics. Market participants indicated that even when import parity calculations appeared workable for traders, buyers were unwilling to commit volumes because steel and sponge margins remained under severe pressure.

Weak sponge market limits coal acceptance

Demand conditions in the sponge iron and steel sectors continued deteriorating during the week. PDRI DAP-Durgapur prices declined sharply by INR 900/t w-o-w to INR 24,850/t amid sustained weak enquiries and muted transactions.

Participants noted that procurement activity remained entirely requirement-based, with buyers unwilling to build inventories amid falling finished steel prices and uncertain market direction. Traders stated that even at lower imported coal realisations, buyers were not showing confidence due to lack of visibility in downstream demand.

Participants highlighted that import economics remained extremely challenging this year, as rising freight and volatile FOB markets were not translating into improved domestic realisations.

Domestic coal, high port inventories pressure import prices

Domestic coal continued exerting significant pressure on imported South African cargoes. India’s domestic non-coking coal prices declined by around INR 250-300/t w-o-w following weaker premiums in recent SECL auctions and subdued industrial demand. Comfortable domestic coal availability encouraged consumers to continue favouring local material over imports.

At the same time, India’s non-coking coal inventories at major ports increased by 4.8% w-o-w in week 19 to 15.87 mnt from 15.14 mnt in Week 18. Inventories reached their highest level in the past 25 weeks, further reducing urgency for fresh cargo bookings.

Market participants stated that imported coal offers remained difficult to place amid such elevated inventories and sluggish evacuation levels.

RB3 demand emerges amid limited RB2 availability

Availability of RB2 cargoes remained tight at Mangalore, where traders indicated that fresh RB2 material was largely unavailable. As a result, some buyers shifted towards lower-grade RB3 cargoes despite subdued market sentiment.

A deal for around 10,000 t of 4,800 NAR RB3 coal was heard concluded at around INR 9,550/t ex-Mangalore during the week. Traders noted that buyers were increasingly opting for lower-grade cargoes as a cost-management strategy amid falling sponge margins and weak steel demand.

However, overall enquiries remained extremely limited, with most participants continuing to adopt a wait-and-watch approach.

Outlook

South African coal prices may continue receiving support from higher freight costs, firm oil prices, and geopolitical tensions affecting global commodity markets. However, weak sponge iron demand, elevated Indian port inventories, lower domestic coal prices, and persistent buyer resistance are likely to keep overall market sentiment subdued.

Unless downstream steel demand improves meaningfully, imported South African coal trade is expected to remain highly selective, with buyers continuing to procure only immediate requirement-based volumes.

Leave a Reply