- Imported met coke prices remain stable w-o-w

- Weak downstream sentiment limits buying activity

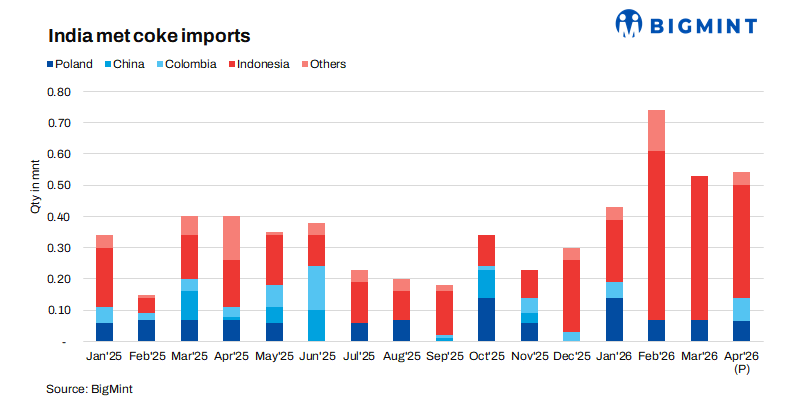

Imported coke bookings gain momentum

Following the Directorate General of Trade Remedies’ (DGTR) proposal to reduce anti-dumping duty on imported met coke, Indonesian suppliers reportedly increased FOB offer levels sharply, anticipating stronger Indian buying interest.

The market reported three deals concluded by end users at $269-271/t FOB levels. Consequently, landed costs for Indian buyers moved higher, with BigMint assessing Indonesian-origin BF-grade coke (65/63 CSR) at around $302/t CFR India, up $2/t w-o-w.

For July shipments, indicative prices are at $275/t FOB levels and discussions are ongoing. Cost-effectiveness over domestic coke has supported import bookings.

Domestic coke prices stable

India’s blast furnace (BF)-grade metallurgical coke prices remained largely stable w-o-w as of 14 May, supported by balanced supply-demand dynamics and elevated import parity levels.

In the eastern region, BF coke prices were steady at INR 36,400/t ex-Jajpur, while western India prices held at INR 33,500/t ex-Gandhidham amid firmer replacement costs and stronger imported coke offers. Foundry-grade (+90 mm) coke prices also remained unchanged at INR 36,400/t ex-Rajkot, reflecting stable procurement from the casting and foundry sectors.

Market participants highlighted that logistics and operational disruptions following the recent diesel price hike continued to affect plant and port operations. At the same time, buying activity remained cautious as traders and end-users awaited clarity on the final anti-dumping duty (ADD) decision on imported met coke.

Rising coking coal prices support coke costs

Upstream raw material costs also strengthened during the week. Australian premium hard coking coal (PHCC) prices increased by $7/t w-o-w to $240/t FOB Australia, supported by firm buying interest and tighter availability of premium-quality cargoes.

Meanwhile, China’s domestic coke and coking coal markets remained stable with a slight upward bias, backed by steady mine production, improved trading sentiment, and firm steel demand. The full implementation of the third round of coke price hikes in China improved coke plant profitability and supported stable operating rates, while higher pig iron output at steel mills sustained healthy coke consumption and low inventories.

Pig iron market reflects cautious sentiment

On the downstream side, the pig iron market reflected mixed sentiment. Steel-grade pig iron prices in Durgapur increased by INR 500/t w-o-w to INR 38,500/t ex-works, supported by stable raw material costs. However, buying sentiment remained cautious.

This was evident in SAIL Bhilai’s 11 May auction for 2,990 t of steel-grade pig iron, where the entire quantity was booked at an average realisation of INR 38,500/t ex-works. The auction price declined by INR 600/t compared to the 22 April auction, indicating subdued downstream demand, cautious procurement strategies, and continued pressure on finished steel consumption.

Outlook

India’s BF-grade met coke market is expected to remain stable-to-firm in the near term. Elevated import parity, rising coking coal costs, and firm overseas coke offers are likely to support domestic prices. However, cautious downstream buying, uncertainty surrounding the final ADD structure, and weak sentiment in the pig iron and steel segments may limit any sharp upward movement.

Leave a Reply