- Scrap and sponge prices fall by INR 200-300/t d-o-d

- Weak finished steel demand pressures margins in Mandi

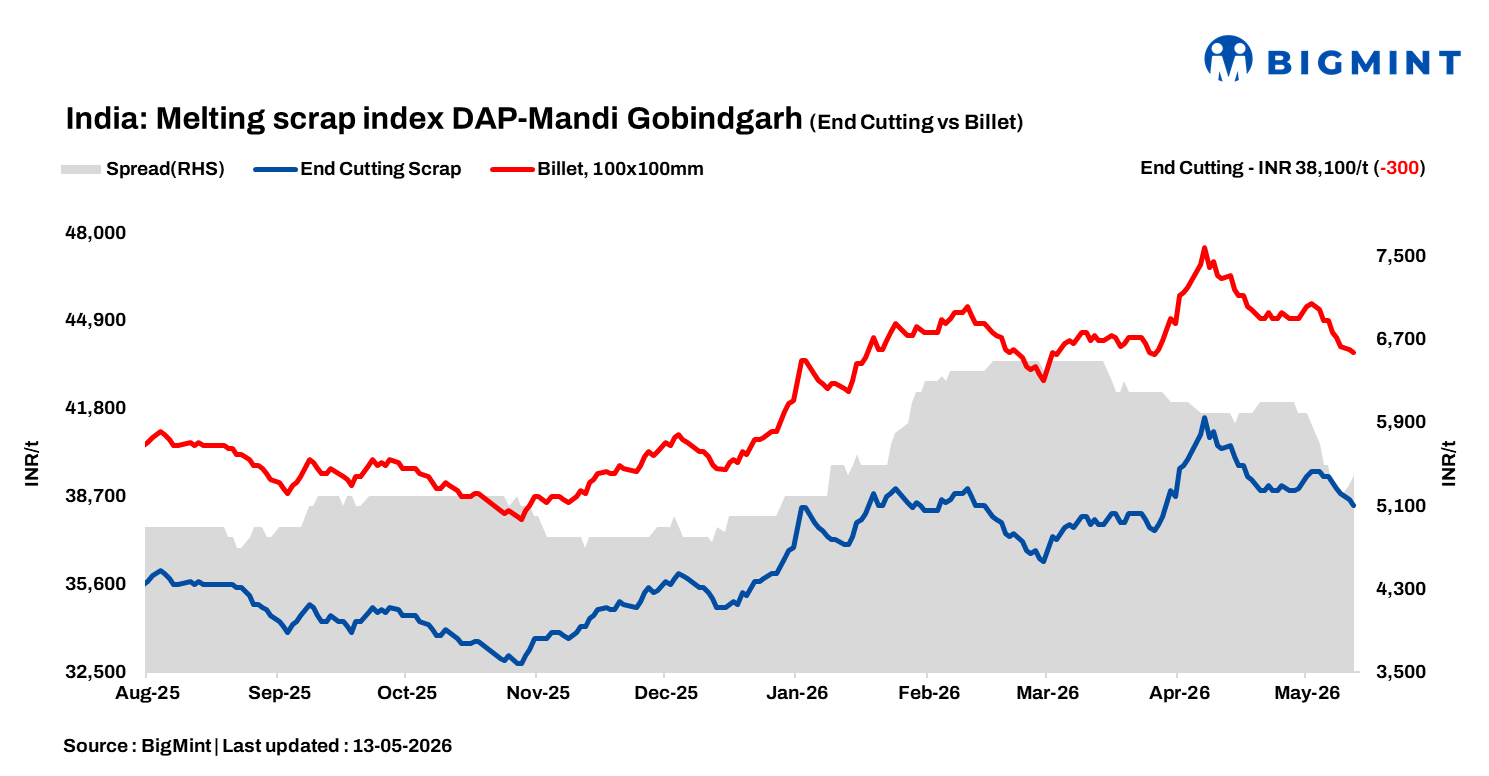

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, dipped by INR 300/tonne (t) d-o-d to INR 38,100/t DAP on 13 May 2026.

The steel market in Mandi Gobindgarh is currently experiencing a downturn, with scrap prices dipping by INR 200-300/t d-o-d as weak finished steel demand dampens overall sentiment. Market participants are prioritising cash flow, restricting purchases strictly to immediate requirements and largely abandoning bulk procurement.

This climate of caution is compounded by significant operational hurdles; mills are grappling with rising inventory pressure, liquidity constraints, and persistent labour shortages, all of which are severely compressing profit margins for local steelmakers.

Furthermore, the import market for scrap has effectively come to a standstill in the region due to poor price viability, leaving mills reliant on domestic supply despite the challenging cost environment. With the current disconnect between input costs and finished product demand, the market remains in a defensive state.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh decreased by INR 200/t d-o-d to INR 31,500/t DAP. In contrast, steel-grade pig iron prices in Ludhiana inched up by INR 150/t to INR 41,650/t DAP.

Steel market trends

In Mandi Gobindgarh, semi-finished steel (ingot) prices moved down by INR 200/t to INR 43,500/t DAP, reflecting lacklustre steel demand. In other major production centres, ingot prices declined by INR 100-650/t d-o-d.

In Mandi Gobindgarh, rebar (Fe500) prices declined by INR 200/t to INR 48,500/t exw today. HR strip (patra) prices fell by INR 500/t d-o-d to INR 44,600/t exw.

Overview of Alang market

The Alang market witnessed a correction today, with melting scrap prices slipping by INR 500/t d-o-d. BigMint assesses HMS (80:20) at INR 36,000/t ex-yard. This dip follows a broader regional trend where semi-finished and finished steel prices weakened by INR 300-500/t in the previous session due to sluggish demand. With average trade volumes failing to pick up, suppliers have responded by lowering their offers to stimulate buying interest.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,300-5,700/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $380/t, approximately INR 38,650/t (inclusive of freight). Today, HMS (80:20) prices in Mumbai remained stable d-o-d at INR 34,400/t DAP. Indicative prices of shredded from Europe stood at $395/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,650/t.

To see BigMint’s melting scrap assessment, pricing methodology and specification documents, click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply