- Global cotton consumption projected at 121.7 million bales in 2026-27

- Production forecast to decline 5% y-o-y, reducing global stocks

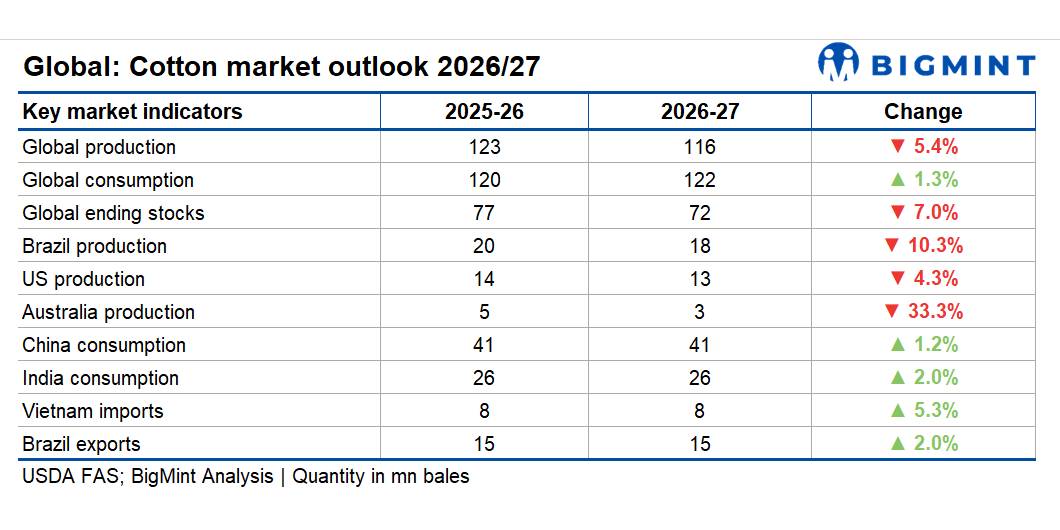

The global cotton market is entering a tighter supply-demand phase in MY 2026-27, with global consumption forecast to rise to a six-year high of 121.7 million bales while production is expected to decline to 116 million bales, according to the latest USDA outlook. The widening deficit is projected to reduce global ending stocks by 5.4 million bales to 71.8 million bales, tightening fiber availability across key producing and consuming nations.

Demand continues to remain resilient despite elevated cotton prices and broader economic uncertainty. Apparel retail sales in the US grew 8% in 2025, while China expanded textile exports into alternative markets, particularly the European Union, amid shifting trade flows linked to tariff disruptions. Traders said global apparel retailers are expected to increase inventory replenishment during the second half of 2026 after maintaining cautious buying patterns over the past year.

Global production is forecast to fall by 6.6 million bales year on year, led by lower crops in Brazil, the US, China, Australia, Pakistan, and Turkiye. Brazil’s output is projected at 17.5 million bales against 19.5 million bales last year, while US production may decline to 13.3 million bales from 13.9 million bales. Australia’s crop is expected to plunge 33% y-o-y to 3 million bales.

China’s cotton consumption is forecast at 41 million bales, up from 40.5 million bales, while India’s mill use is expected to rise to 26 million bales. Vietnam is projected to become the world’s largest cotton importer at 8 million bales.

Cotton is also gaining relative competitiveness against polyester as rising crude oil prices increase synthetic fiber production costs. ICE cotton futures have already risen nearly 13 cents since the previous WASDE report to around 84 cents/lb, while the Cotlook A-Index climbed to 92.8 cents/lb from 82.6 cents/lb within a month.

Market participants said spinning mills across Asia have started extending forward cotton coverage amid expectations of tighter nearby supplies and improving yarn demand. In the short term, weather risks, tightening inventories, and higher polyester costs are expected to keep global cotton sentiment firm.

Leave a Reply