• Prices remain largely stable w-o-w across grades

• Weak steel demand and rising supply expectations weigh on sentiment

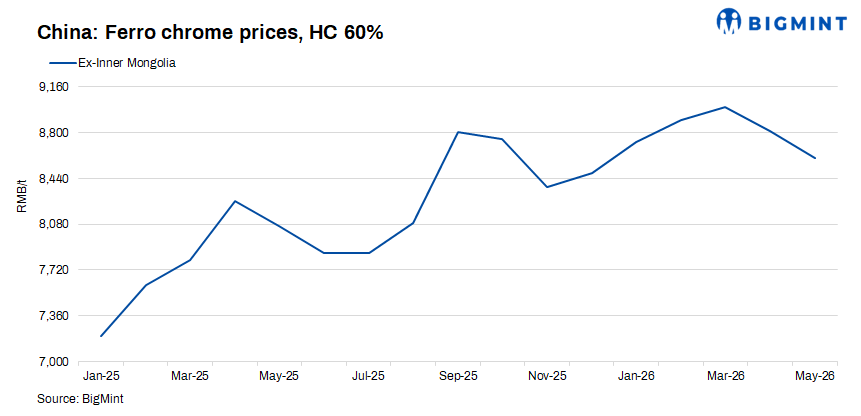

High-carbon ferro chrome (Cr:50%, C:6-8%) prices in China edged down w-o-w to RMB 8,390-8,800/t ($1,235–1,295/t) from RMB 8,490–8,900/t ($1,250–1,310/t). Medium-carbon (Cr:60%, C:1%) prices remained unchanged at RMB 13,300–13,500/t ($1,958–1,987/t), while low-carbon (Cr:60%, C:0.1%) prices eased slightly to RMB 13,900–14,200/t ($2,046–2,090/t) from RMB 14,000–14,300/t ($2,061–2,105/t), exw including taxes.

China’s ferro chrome market remained weak but stable, as firm chrome ore costs and high freight rates continued to support prices, while sluggish downstream demand and expectations of higher domestic and overseas supply capped market upside.

Market updates

Supply expectations pressure market sentiment

Market sentiment remained cautious amid expectations of increased ferro chrome output in China and higher overseas supply, particularly from South Africa and Zimbabwe. Although maintenance shutdowns at some Inner Mongolia plants offered limited support, anticipated production recovery in southern regions during the rainy season continued to weigh on prices.

Chrome ore prices remained relatively firm, supported by stable overseas offers and elevated freight costs. However, rising port inventories weakened raw material support marginally, while easing power cost expectations in southern China reduced cost-side pressure.

Weak steel demand limits transactions

Downstream stainless steel mills maintained cautious procurement despite stable production levels and improved steel margins. Mills largely relied on existing inventories and continued need-based buying, resulting in subdued spot transactions and weak bidding activity.

Although some phased procurement from carbon and special steel mills may provide marginal support, sluggish end-user demand and ample inventories continued to limit any meaningful recovery in ferro chrome prices.

Outlook

China’s ferro chrome prices are expected to remain range-bound with a weak bias in the near term. Firm ore costs and maintenance-related supply constraints may support prices, while rising supply expectations, high inventories, and cautious downstream procurement are likely to cap upside momentum.

Leave a Reply