- Higher renewable generation softened power prices despite rising demand

- Heatwave-driven demand spikes exposed grid and supply vulnerabilities

The first ten days of May 2026 highlight an important shift underway in India’s electricity market. While total generation continued to expand and peak demand climbed steadily, the market experienced significantly lower electricity prices. The explanation lies in the rapid growth of renewable energy, which helped ease supply pressures and moderate exchange prices despite stronger demand.

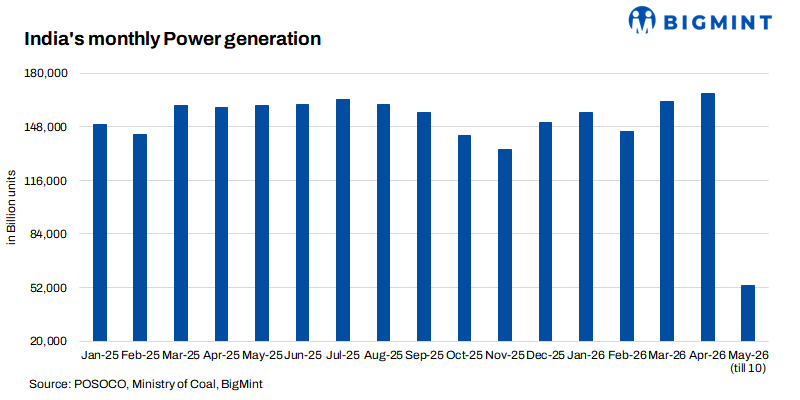

Total electricity generation during May 1-10, 2026 reached 53,353 million units (MU), an increase of 4.7% compared with 50,938 MU in the corresponding period of 2025. However, the composition of this growth tells a more meaningful story. Renewable energy sources – including wind, solar and biomass – emerged as the principal source of incremental supply, while expensive gas-fired generation lost ground.

Generation mix changes as renewables take the lead

Renewable energy generation increased sharply by 28.3% year-on-year to 9,408 MU, contributing an additional 2,074 MU to the system. This made renewables the single largest contributor to electricity growth during the period. By contrast, coal-based generation increased only modestly by 1.3%, reinforcing the view that thermal power remains the backbone of India’s electricity system but is no longer the dominant source of incremental generation growth.

Gas, naphtha and diesel-based generation witnessed the sharpest decline, falling 47.8% year-on-year. High imported LNG prices and the increasing availability of cheaper renewable electricity likely made gas-based generation significantly less competitive. Nuclear and lignite generation provided stable support, while hydropower remained largely unchanged.

The data shows that renewables accounted for the overwhelming majority of incremental growth during the period, while coal’s contribution remained comparatively limited. This changing generation mix also played a decisive role in shaping electricity market behaviour.

Stronger peak demand signals summer stress

India’s power demand continued to strengthen during the first ten days of May. Average peak demand met increased by 6.1% year-on-year to 222,371 MW, compared with 209,665 MW during the same period in 2025.

The highest single-day peak reached 228,958 MW on May 2, almost 13 GW higher than the corresponding peak recorded in early May last year. Demand remained elevated through the period, particularly during evening hours between approximately 3:30 PM and 7:30 PM, suggesting stronger cooling demand as summer temperatures intensified.

The steady increase in peak demand after May 4 suggests that India’s electricity system is entering a more intensive summer demand phase. Yet, despite stronger demand, electricity prices behaved very differently from what many market participants may have expected.

IEX prices fall despite stronger buying interest

On the Indian Energy Exchange (IEX), underlying demand remained robust. Average purchase bids increased by 32% year-on-year to 228,668 MWh, reflecting higher procurement requirements by utilities and market participants.

However, market liquidity improved even faster. Average sell bids surged by 41.6% to 474,732 MWh, creating a substantial supply cushion. As a result, average market clearing prices (MCP) fell 17.4% year-on-year to INR 2,596/MWh from INR 3,143/MWh during the same period in 2025.

The main reason for lower prices was the strong increase in renewable generation. Low-cost, must-run renewable power entered the system in greater quantities, particularly during daylight hours, increasing sell-side liquidity and preventing price escalation. Sell bids exceeded purchase bids by roughly two times on most days, maintaining surplus market conditions.

This calmer market environment stands in sharp contrast to the turbulence witnessed only weeks earlier.

April 2026: A month of extreme volatility

April 2026 was marked by unprecedented demand growth and dramatic price swings across India’s electricity market. A severe heatwave drove electricity consumption sharply higher, culminating in an all-time peak demand of 256,117 MW on April 25.

The country crossed the 250 GW peak demand threshold on four separate days between April 24 and April 28, while average monthly peak demand approached approximately 230 GW – levels never seen before.

The IEX experienced extraordinary volatility during this period. Market clearing prices ranged from a low of INR 2,013/MWh on April 5 to INR 7,577/MWh on April 25 – a nearly fourfold increase within the same month.

The most intense market stress emerged during April 24-27. On April 25, purchase bids crossed a record 1.016 million MWh while sell bids dropped sharply to just 197,000 MWh, triggering an explosive rise in prices to INR 7,577/MWh.

The reasons for this volatility were likely multifaceted. Extreme heat sharply increased air-conditioning demand, particularly during evening hours. At the same time, supply constraints may have emerged due to limitations in gas availability, hydro generation or coal logistics. Renewable energy, despite strong daytime performance, was unable to fully bridge the post-sunset demand surge.

By the final days of April, however, market conditions normalised rapidly. Purchase bids fell back to around 250,000 MWh, supply recovered, and MCP dropped sharply to INR 2,192/MWh by month-end.

A more stable market, but risks remain

The first ten days of May suggest India’s electricity market is becoming more renewable-intensive, more liquid and structurally cheaper under normal operating conditions. Renewable energy is increasingly shaping incremental supply growth, while stronger sell-side participation on IEX is helping moderate prices despite rising electricity demand.

However, April’s experience underscores an important reality. India’s transition remains uneven and weather-sensitive. On days when renewable generation weakens or extreme temperatures sharply raise cooling demand, electricity prices can still surge violently.

The challenge going forward will be managing the growing gap between strong daytime renewable output and rising evening electricity demand. Faster deployment of battery storage, greater system flexibility and improved demand-side response mechanisms will likely become increasingly important.

For now, India appears to be entering a new electricity market regime – one characterised by lower average prices and stronger renewable penetration, but punctuated by occasional periods of severe volatility whenever weather and supply conditions tighten simultaneously.

Leave a Reply