- Citigroup forecasts copper may reach $15,000/t by year-end

- Chinese scrap inflows disrupted amid new regulatory measures

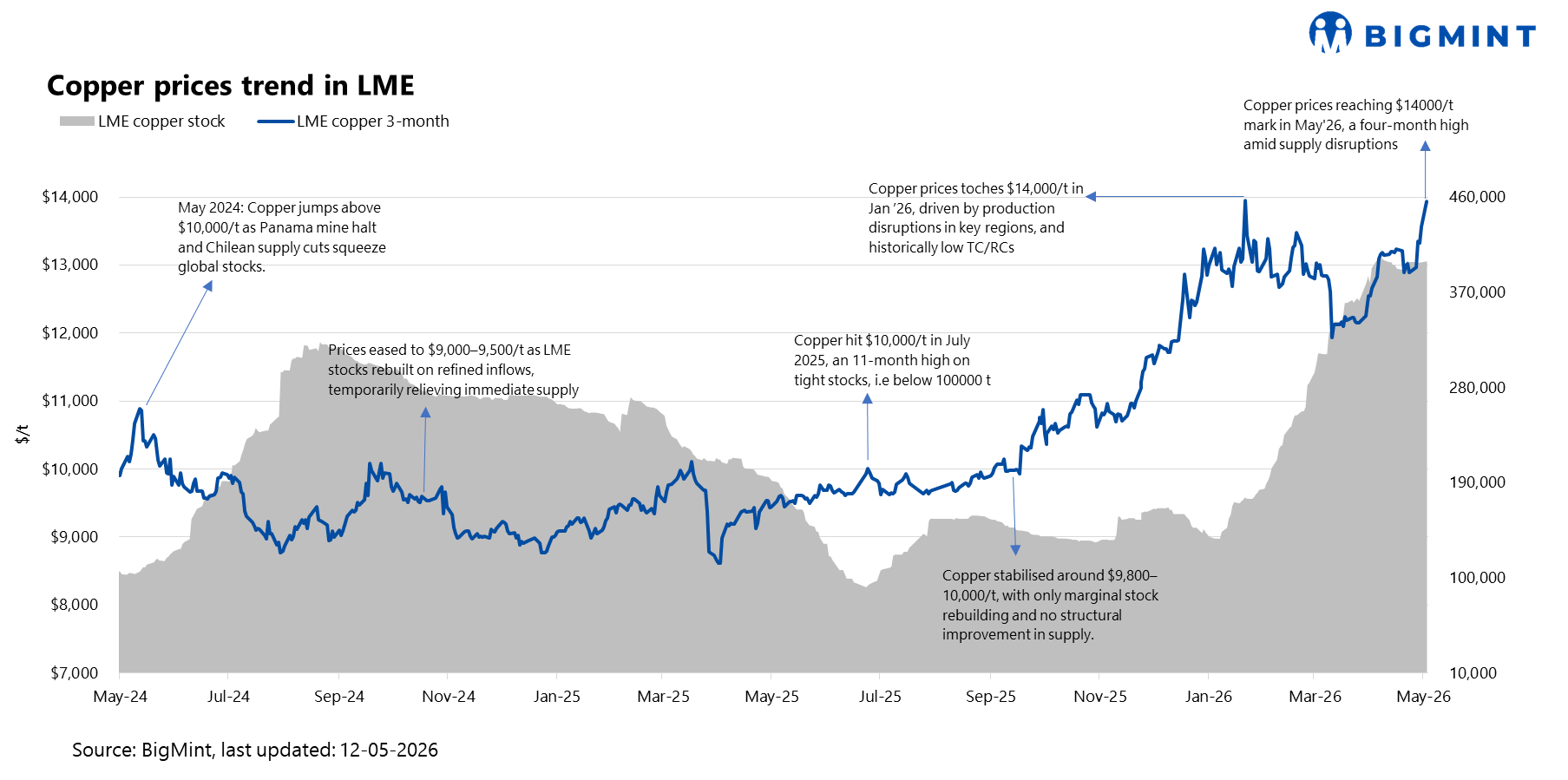

Copper prices on the London Metal Exchange (LME) extended their rally, with three-month copper closing at $13,637/t on Monday, 1.7% higher than last week’s close, as persistent supply concerns and resilient market sentiment continued to support gains. On Tuesday, prices climbed further and moved closer to the $14,000/t mark, reaching a four-month high, despite heightened geopolitical tensions and broader macroeconomic uncertainty.

Despite the ongoing US-Iran conflict, continued disruption around the Strait of Hormuz, elevated oil prices, and weakening global growth expectations, the red metal climbed to its highest level since late January. Investors appeared less concerned about immediate escalation risks, with broader risk sentiment stabilising across global markets. All major LME base metals posted gains d-o-d, reflecting confidence in tightening fundamentals rather than geopolitical fear-driven volatility.

Supply-side disruptions remained a key driver. Continued constraints in copper concentrate availability, pressure on treatment and refining charges (TC/RCs), and tighter scrap supplies supported bullish sentiment. In China, regulatory action on metals-backed financing has disrupted scrap flows, narrowing the traditional discount between scrap and refined copper and adding further supply tightness.

Analysts also pointed to longer-term structural demand support. Rising copper consumption from the energy transition, artificial intelligence infrastructure, electric vehicles, and defense manufacturing continues to offset concerns around weak cyclical demand. Citigroup maintained its constructive outlook, indicating copper could potentially reach $15,000/t by year-end if supply tightness persists and market sentiment improves.

Overall, copper’s resilience signals continued strength in global industrial metals markets, although elevated prices may keep downstream buyers cautious in the near term.

Can downstream copper manufacturers absorb higher costs as concentrate tightness pushes refined copper prices higher? How vulnerable is India’s copper supply chain to prolonged scrap and concentrate tightness? With LME copper crossing $13,500/t, how resilient will cathode demand from India’s wire and cable sector remain?

Join the discussion at BigMint India Non-Ferrous Week 2026 on 9-10 June in Mumbai.

Leave a Reply