- Coal-fired generation rises 35% y-o-y in Q1CY’26, gas-based output down by 8%

- Coal imports may cross 12 mnt in H2, Indonesia to capture 70% of higher volumes

The first definitive signs of structural gas-to-coal switching have emerged in Bangladesh, a critical bellwether for South Asian energy markets and a potential game-changer for Indonesian and South African thermal coal demand. With natural gas prices remaining much higher than pre-conflict levels, Bangladesh’s power generators have pulled the trigger on a decisive fuel shift. Coal-fired generation surged 35% y-o-y in Q1CY’26, while gas-fired generation fell nearly 8% — a divergence that BigMint believes will accelerate through Q2 and Q3, with our projections suggesting that coal imports will rise sharply by 40% y-o-y.

Coal gains ground in Bangladesh amid gas supply constraints

According to data from the Bangladesh Power Development Board (BPDB), Bangladesh’s power generation witnessed strong growth in both March and the first quarter of 2026, primarily driven by higher coal-based generation. Total electricity generation in March 2026 reached 8.3 TWh, reflecting a 9% y-o-y increase. Coal-fired generation rose sharply by 23% y-o-y to 2.6 TWh, highlighting the growing contribution of coal-based plants to the country’s power mix. In contrast, gas-fired generation declined by 16% y-o-y to 3.6 TWh, indicating reduced reliance on gas amid supply constraints and shifting fuel dynamics.

During Q1CY’26, Bangladesh’s total power generation increased by 17% y-o-y to 22.4 TWh. Coal-fired output surged 35% y-o-y to 7.2 TWh, while gas-fired generation fell by 7.8% y-o-y to 9.5 TWh. The trend underscores the country’s increasing dependence on coal-based power generation to meet rising electricity demand and offset lower gas-based output.

Notably, March coal-fired generation of 2.6 TWh represents the highest monthly figure since the Payra and Matarbari ultra-supercritical plants reached full operational capacity. The 20.5% m-o-m jump from February confirms this is not a one-off but an accelerating trend.

The price triggers (as recorded on 11 May’26)

- Spot LNG NE Asia: $16.95/MMBtu (neutral/negative short-term but still elevated historically, up 82% from February-end levels)

- Dutch natural gas futures (TTF Q3CY’26): EUR 46.70/MWh (up by around 50% from February-end, neutral/positive forward view)

- Indonesian spot coal FOB Indonesian 4200 GAR: $62.50/t (flat, but with upside risk)

- South African RB3 (5500 kcal) FOB Richards Bay: $99/t

At current LNG prices, the breakeven for gas-fired power in Bangladesh is approximately $0.12/kWh. In contrast, coal-fired generation from Indonesian 4200 (delivered DES Bangladesh @ $85/t) comes in at $0.075/kWh. This represents a massive 37.5% discount. Every $1/MMBtu move in global LNG prices widens or narrows that gap by roughly $0.008/kWh.

Supply side: Who benefits?

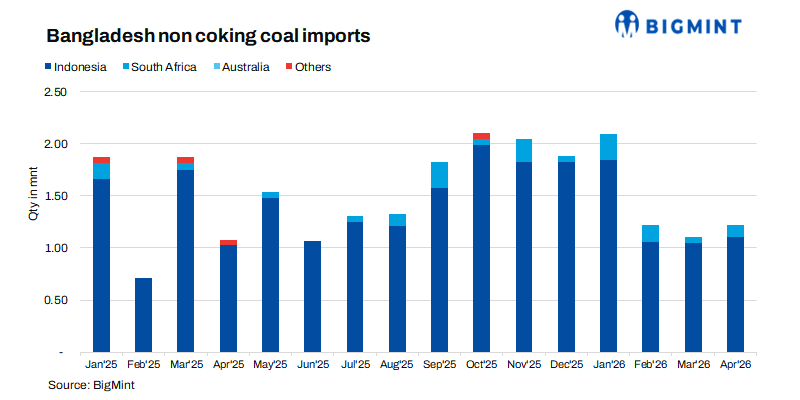

Indonesia: Bangladesh imported 4 mnt of bulk thermal coal from Indonesia in Q1CY’26, almost stable y-o-y. But BigMint expects this to rise sharply. Indonesian exports to Bangladesh typically lag by 4-6 weeks due to voyage times from East Kalimantan to Mongla/Chittagong. This raises Bangladesh’s total import forecast for H2CY’26 from 9.5 mnt to 12.5 mnt, with Indonesia capturing 70% of incremental volumes.

South Africa: While Bangladesh has favoured Indonesian low-CV coal, the new ultra-supercritical plants at Payra (1,320 MW) and Matarbari (1,200 MW) are designed for a 5,500-6,100 kcal/kg blend. This opens the door for South African RB3 (5,500 kcal) and even some Colombian material — though freight dynamics currently penalise the Atlantic basin. The premium for South African over Indonesian is currently $32/t, which is too wide for aggressive switching. For South Africa to capture meaningful market share, either RB3 must drop to $85/t FOB or LNG must rally above $20/MMBtu.

The freight angle

The Panamax 5TC index closed Monday at $20,548/day, up 18% m-o-m. This tightening is hitting Bangladesh harder than most because of the following reasons:

1. Chittagong port restrictions require lighterage or smaller vessels, reducing operational efficiency.

2. Indonesian domestic shipping obligations (DMO) limit spot Panamax availability from Kalimantan.

Utility response, tender activity

BPDB has issued three spot tenders in the past 10 days for July-September delivery. The 4,800 GAR tender awarded at $75/t FOB Indonesia implies a delivered price of $88/t DES Bangladesh, producing power at $0.078/kWh. This is aggressive but achievable.

Leave a Reply