- Imports surge as domestic ADC12 prices rise

- Scrap shortage and West Asia disrupt supply chain

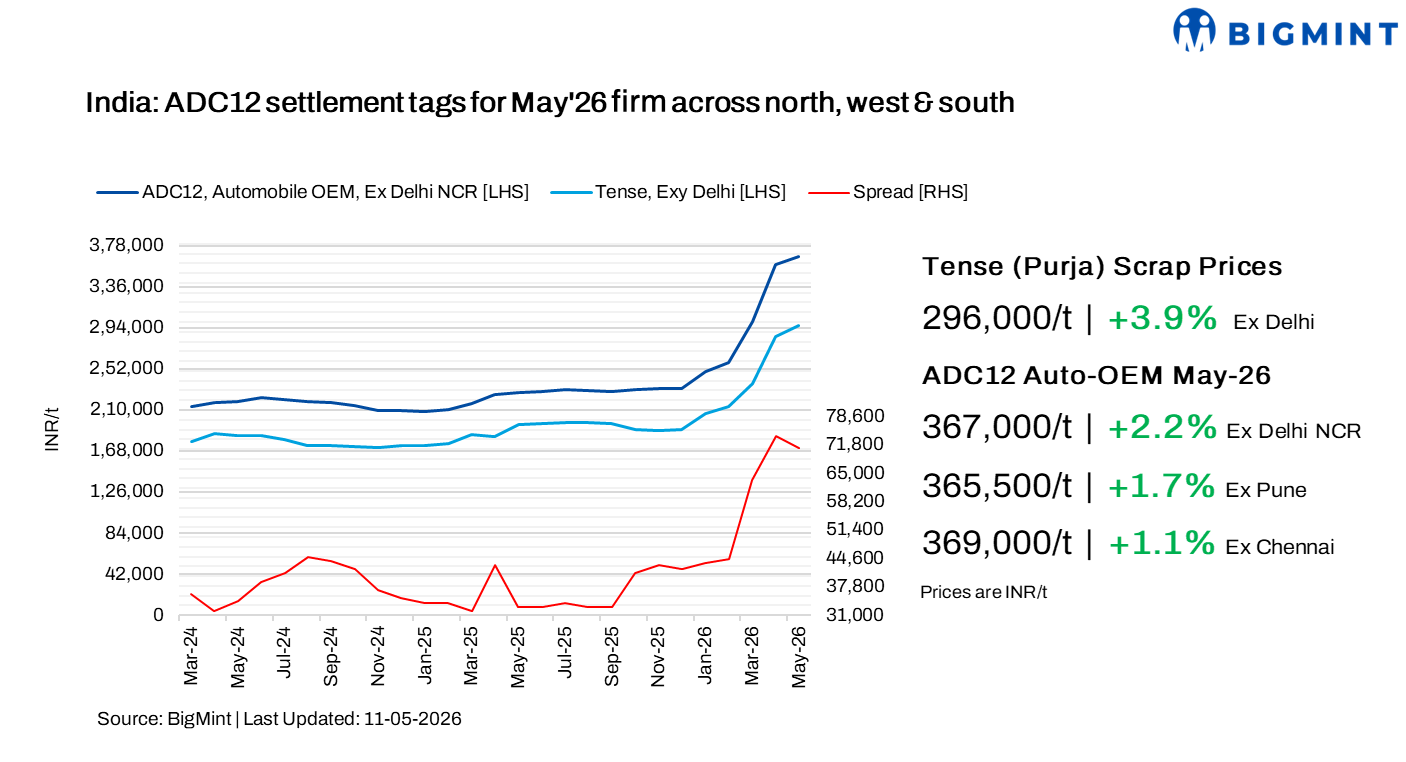

The spread between scrap and semi-finished products widened further, averaging around INR 70,000-71,000/t in Delhi NCR and INR 60,000-61,000/t in Chennai region. The expansion was mainly driven by a sharp rise in ADC12 prices, while scrap prices recorded only a limited increase.

Market insights

ADC12 prices across key Indian markets have remained firm amid rising raw material costs. Price stood at:

- Chennai: INR 368-370/kg

- Delhi: INR 367/kg

- Pune: INR 365-366/kg

Despite higher input costs, ADC12 prices in Chennai have largely stagnated as buyers continue to resist further hikes. Deals for 30-day payment terms were heard in the range of INR 368-373/kg, while offers were quoted as high as INR 375-380/kg. However, buyers have been actively negotiating, limiting upside momentum.

In contrast, Delhi market prices witnessed an uptick, particularly following price hikes announced by major automakers, reportedly up by INR 44,100/t.

A secondary producer indicated that market participants are anticipating a potential slowdown in ADC12 demand following Prime Minister Narendra Modi’s speech on 10 May 2026, which emphasized work-from-home practices, virtual meetings, and reduced fuel consumption.

The industry believes these measures could temper near-term passenger vehicle demand, particularly in urban markets where daily commuting significantly influences vehicle usage. Reduced office travel may delay replacement cycles for entry-level and mid-segment cars, while lower corporate travel spending could also weigh on fleet demand.

In addition, the government’s emphasis on conserving foreign exchange and discouraging non-essential consumption may make consumers more cautious toward discretionary spending, including automobile purchases. However, the impact is expected to be moderate rather than severe, as India’s long-term car demand continues to be supported by rising incomes, aspirations for personal mobility, and relatively low vehicle penetration levels.

Alloy imports plunge m-o-m

Imports: Meanwhile, India’s ADC12 alloy ingot imports recorded a sharp increase, rising 265% y-o-y in Q1CY’26 to 2,007 t compared with 550 t in Q1CY’25. As domestic ADC12 prices continued to rise, buyers increasingly turned their attention to imports from FTA countries such as Malaysia.

Exports:In Q1CY’26, outbound volumes from India stood at 3,566 t, declining by 2.6% from 3,661 t in Q1CY’25, as strong domestic demand continued to absorb most of the available supply. Tight availability of ADC12, coupled with rising consumption, prompted suppliers to prioritise domestic allocations over exports.

Raw material trends

In May, imported aluminium scrap prices moved higher, supported by firm average prices on the London Metal Exchange (LME) at around $3,531/t, amid tight global supply, volatile market conditions, currency pressures, and ongoing geopolitical tensions in the Middle East, which continued to elevate freight and insurance costs.

In line with imported scrap trends, domestic aluminium scrap prices — particularly casting-grade material used in ADC12 production — also strengthened, as availability tightened, especially in southern India.

Among key imported grades, US-origin Tense increased by $98/t m-o-m to $2,750/t, while UK-origin Wheel scrap rose by $132/t to $3,479/t.

Meanwhile, China-origin silicon metal 553 prices decreased by $23/t, rising to $1,350/t on a CFR Mundra basis, amid oversupply and weak downstream demand in China.

Outlook

ADC12 prices are expected to remain range-bound and stabilize in the near term, as cautious buyer sentiment and resistance to higher prices continue to cap further gains. Automotive demand remains steady, but elevated price levels are keeping buyers cautious. Import parity constraints and logistical hurdles are likely to limit overseas inflows, sustaining domestic support. However, upside appears capped, with prices expected to consolidate at elevated levels amid cautious consumption trends and evolving mobility-related demand signals.

Leave a Reply