- Australian supply delays support met coal

- Weak steel demand caps price rally

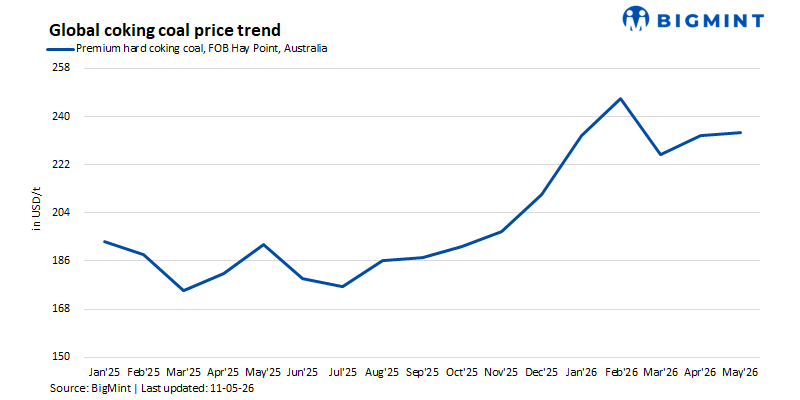

The global metallurgical coal market is navigating a landscape of tight premium mid-vol supply against a backdrop of selective demand from India and China, while European and US markets grapple with energy policies and trade shifts. Prices for premium hard coking coal (HCC) firmed mid-week before stabilizing, driven by a specific supply disruption rather than broad-based buying.

Premium HCC: Delays down under prop up FOB Australia

The FOB Australia premium low-vol (PLV) hard coking coal index reached $240/t by May 8, climbing $6-7 on the week. This upward momentum was primarily fueled by a single trade of Australian premium mid-vol (PMV) Goonyella cargo at $242.8/t FOB for a 75,000 mt shipment loading June 10-19. The widening premium of PMV over PLV from $2/t to $3/t underscores a specific tightness for mid-vol material.

Ongoing delays at the Centurion (North Goonyella) mine in Australia, which led a major producer to downgrade its full-year 2026 production outlook to 2.5mnt, have prompted traders to secure available PMV cargoes. While this supply-side issue supported the FOB market, it did not translate into aggressive buying in the CFR China segment. Chinese buyers remained cautious; while domestic Shanxi premium low-vol coal prices rose to Yuan 1,590/t ex-washplant, seaborne interest stayed muted. The prevailing spread between domestic and seaborne material offered little arbitrage incentive. A third round of coke price hikes proposed by Chinese cokeries remained unconfirmed by mills, keeping sentiment in check.

Atlantic met coal: US producers prioritise contracts

On the US East Coast, low-vol HCC edged up $3/t to $195/t FOB on May 8, supported by a trade for a 40,000 mt cargo at $194.5-195/t. Producer sources indicated that contractual obligations are taking precedence over spot sales. Interest in premium US coal remains underpinned by elevated Australian benchmarks.

An offer for a lower-priced Panamax cargo at $173/t FOB was dismissed by market participants as material with quality challenges, such as oxidation or high sulfur, underscoring the premium for benchmark-grade coal. High-vol A and B grades remained stable at $159/t and $149/t FOB USEC respectively, with ample supply noted.

Metallurgical coke: Indonesian offers climb on costs

The metallurgical coke market saw upward pressure on the supply side, with an Indonesian producer raising July-loading offers for 65/63 CSR coke to $270/t FOB from $265/t, citing higher production costs.

In China, domestic coke prices held steady as mills continued to resist a third round of Yuan 50-55/mt hikes proposed by cokeries since late April.

PCI markets: Russian material gains foothold in China

The pulverized coal injection (PCI) market is undergoing a structural shift. Trade flows for CFR China are now predominantly for Russian material, prompting Platts to propose updated specifications for its Low Vol and Mid Vol PCI CFR China assessments, effective July 1. Proposed changes include adjustments to volatile matter, ash, CV, and payment terms (to T/T at sight) to better align with Russian-origin cargoes.

In the seaborne market, Russian Low-Vol PCI trades were reported at $153/t CFR Indonesia for June and July laycans. Meanwhile, an Australian Low-Vol PCI cargo was indicated at $156.4/t FOB Australia.

Steel market feedback loop curbing raw material demand

The demand for met coal, coke, and PCI is being moderated by global steel industry conditions

- China: Steel mill profits have improved with recent increases in steel prices, leading to active restocking of domestic coal. However, high portside inventories and ample Mongolian supply mean mills see little urgency for seaborne premium grades

- Europe: Activity has dwindled as buyers wait for finalised safeguard quota volumes. Some mills are reducing shift times or favoring night-time operations for electricity cost savings. Sustained strength from renewables is also capping thermal coal burn

- India: Demand for imported met coal remains lackluster. An India-based steelmaker noted that despite tightness in prime HCC supply, there is no corresponding end-user demand at current price levels

- US: Mini-mills are running above 80% capacity , with HRC prices near 27-month highs at $1,060/st. However, mild weather and weak natural gas prices have lowered domestic thermal coal consumption.

Outlook

The seaborne met coal market is expected to remain in a state of fragile equilibrium through mid-2026. While supply constraints in Australia (diesel shortages and North Goonyella delays) provide a definitive floor for FOB prices, significant upside is limited by the “wait-and-see” stance in Europe and China’s self-sufficiency in domestic and Mongolian coal.

Ongoing geopolitical uncertainty in the Middle East will likely continue to support fuel-switching in Europe, potentially lifting thermal coal demand – and by extension, the broader coal complex – as the region enters the summer restocking phase. However, unless Indian steelmakers resume aggressive pre-monsoon procurement or the Strait of Hormuz conflict triggers further logistics-driven price spikes, the market is likely to see rangebound trading rather than a sustained rally.

Leave a Reply