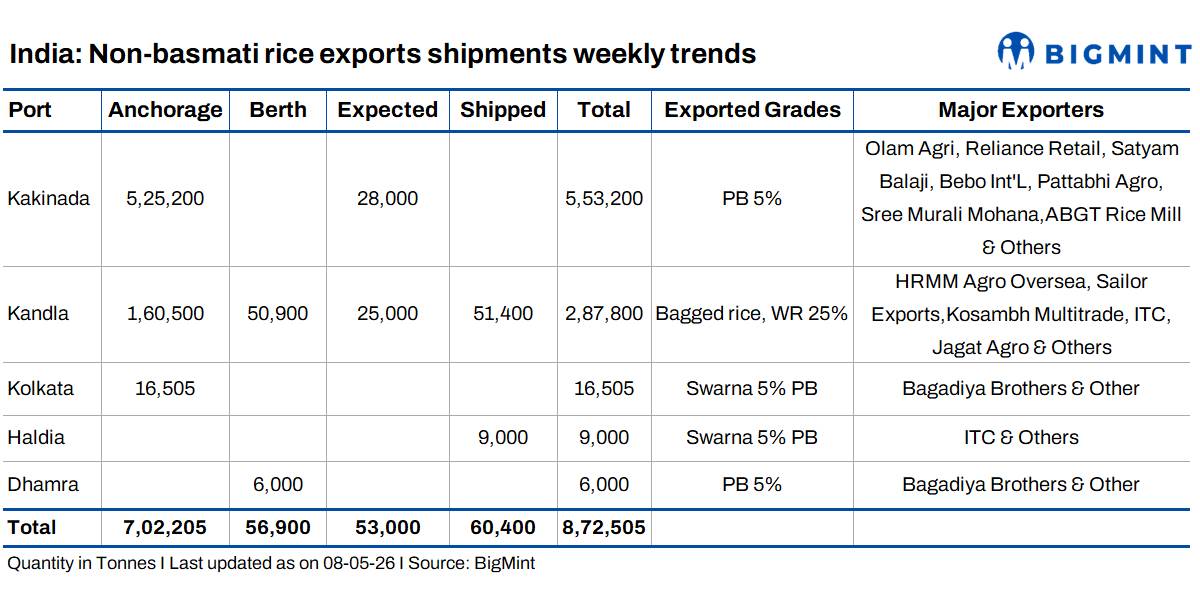

- Non-basmati rice shipments fell to 60,400 MT from 144,000 MT w-o-w; port pipeline remains high at 872,505 MT.

- Heavy anchorage at Kakinada and Kandla Port reflects slower vessel clearance.

India’s non-basmati rice export shipment activity slowed significantly this week, with vessel dispatches declining sharply despite a substantial buildup of cargo at major ports. The latest port movement data indicates growing pressure on export logistics, as lower shipment execution and rising anchorage volumes reflect softer demand and slower cargo clearances.

Shipped volumes drop sharply week-on-week

Total non-basmati rice shipments stood at 60,400 MT this week, down sharply from approximately 144,000 MT in the previous week, highlighting a notable slowdown in vessel loading activity. The decline comes amid weaker buying sentiment from key overseas destinations, particularly West African markets, where import restrictions and delayed procurement decisions continue to impact export flows. Reduced shipment pace suggests that cargo evacuation is lagging behind fresh arrivals at port, contributing to a growing vessel backlog.

Heavy anchorage buildup signals export bottlenecks

Total rice volumes currently in the export pipeline—including anchorage, berth, expected, and shipped cargo—stand at 872,505 MT, indicating substantial pending movement. Anchorage volumes alone have reached 702,205 MT, reflecting heavy cargo accumulation at ports awaiting vessel loading. Kakinada continues to hold the largest share, with 525,200 MT anchored, followed by Kandla Port at 160,500 MT. Smaller anchored volumes were also reported at Kolkata with 16,505 MT. The elevated anchorage suggests slower vessel turnaround and delayed cargo movement, likely linked to weaker buyer nominations and cautious exporter dispatch planning.

Kandla and Kakinada remain key export hubs

Kakinada remains the dominant export point for PB 5% non-basmati rice, with a total cargo pipeline of 553,200 MT. Major exporters operating at the port include Olam Agri & Reliance Retail and several regional rice exporters. Meanwhile, Kandla recorded the highest active movement, with 50,900 MT at berth, 25,000 MT expected, and 51,400 MT shipped, bringing its total cargo volume to 287,800 MT. Exports from Kandla remain focused on bagged rice and WR 25%, supported by major players such as ITC and other trading houses. Eastern ports including Haldia and Dhamra recorded smaller movements, primarily in Swarna 5% PB and PB 5% grades.

Outlook

The current mismatch between high anchorage and lower shipped volumes suggests that India’s non-basmati rice export pipeline remains congested. Unless buying activity improves—particularly from West African destinations—shipment execution may continue to lag, keeping pressure on exporters and FOB prices. In the near term, vessel movement trends, demand recovery from Africa, and pace of fresh export bookings will be key indicators to watch. Continued heavy anchorage buildup could also lead to higher carrying costs and increased pressure to offer competitive prices to accelerate cargo clearance.

Leave a Reply