- NMDC increased iron ore prices, while weak downstream demand continued pressuring pellet and sponge markets.

- Rebar and semi-finished steel prices declined amid rising inventories, subdued demand, and cautious market sentiment.

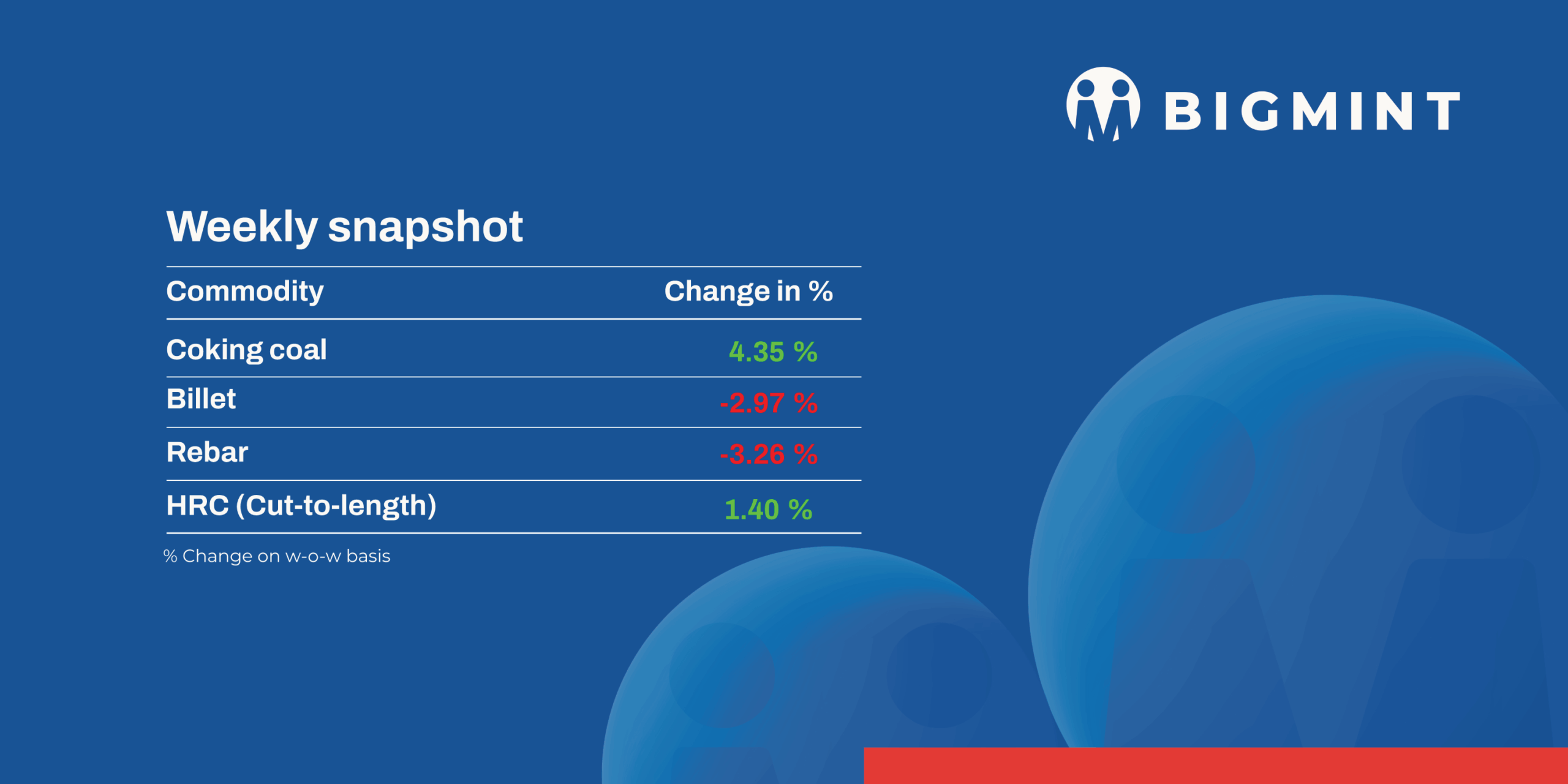

Indian steel markets witnessed mixed trends this week as weak long steel demand pressured prices, while flat steel markets strengthened following mill price hikes.

Iron ore and pellet

- India’s largest merchant iron ore mining company, NMDC, announced its list prices of iron ore CLO (calibrated lump ore) and fines on 6 May 2026, BigMint learnt from sources. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 6,150/tonne (t) ($65/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,700/t ($49.5/t). Prices are on FOR basis from the miner’s Bacheli complex and exclude royalty, DMF, and NMEDT. Prices of all grades increased in the range of INR 200-250/t.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, declined by INR 50/t ($0.5/t) w-o-w to INR 10,000/t ($106/t) DAP on Friday. Pellet prices in the region remained mostly stable during the mid-week session, with limited trade activity observed after NMDC increased iron ore prices for May deliveries. Market participants stated that the hike in iron ore prices lent some support to pellet offers, though weak downstream steel market sentiments continued to weigh on overall demand.

- BigMint’s Indian low-grade iron ore fines (Fe 57%) export index increased by $3/t w-o-w to $65/t FOB east coast on 7 May’26, supported by stronger Chinese buying after the Labour Day holiday. Fresh trading activity and higher-priced deals lifted sentiment in the seaborne market.

Coal

- South African thermal coal prices at Indian ports declined w-o-w amid weak sponge iron demand, high inventories, and limited buying interest. As per BigMint’s assessment, ex-Paradip and ex-Vizag RB2 5,500 NAR declined by INR 100/t to around INR 11,000/t, while RB3 4,800 NAR dropped by INR 150/t to around INR 9,650/t. India’s South African non-coking coal imports fell sharply by 43.4% m-o-m to 1.97 mnt in April. Weak sponge iron prices and rising port inventories of 15.14 mnt further pressured imported coal demand.

- India’s domestic non-coking coal prices dropped by around INR 250-300/t w-o-w following lower premiums in recent SECL auctions and subdued buying activity. As per assessments, 5,000 GCV coal prices declined to around INR 6,000/t, while 4,500 GCV eased to nearly INR 4,300/t. Weak sponge iron and steel market sentiment kept procurement largely need-based. Comfortable domestic coal availability and muted industrial demand continued to pressure overall market sentiment.

- India’s BF-grade metallurgical coke prices remained largely stable w-o-w, supported by firm import parity and higher Indonesian offers. BF coke prices held at INR 36,400/t ex-Jajpur, while west India prices increased marginally by INR 200/t to INR 33,500/t ex-Gandhidham. Indonesian-origin BF coke rose by $9/t to around $300/t CFR India, while Australian PHCC prices increased by $9/t to $240/t FOB Australia. However, weaker downstream demand and falling pig iron prices at INR 38,150/t ex-works Durgapur limited further upward movement in met coke prices.

Ferrous Scrap

- Imported scrap market remained subdued throughout the week, with weak steel demand, poor mill margins and preference for domestic scrap continuing to restrict buying activity. Market participation stayed limited, while persistent bid-offer gaps kept most buyers away from fresh bookings. Early-week activity was further impacted by the UK and European bank holiday, reducing fresh offer availability.

- Selective trades were concluded for competitively priced cargoes, including Somalia-origin HMS 80:20 at around $365/t CFR Mundra and Africa-origin LMS near $320/t CFR Mundra. Offer levels across origins largely remained above workable buyer levels, with Australia-origin HMS 80:20 heard at $370-390/t CFR, UK-origin HMS at $350-370/t CFR, and UK-origin shredded near $395-415/t CFR.

- Market participants noted that limited African export availability, rising domestic consumption in supplier countries and continued preference for lower-priced material kept sentiment cautious. Buyers largely remained focused on immediate requirements, while overall trading activity stayed slow amid subdued downstream demand.

Semi Finished

- India’s semi-finished steel market witnessed a downtrend this week. As per BigMint’s assessment, Billet prices declined by INR 500-1,700/t across regions, with the steepest correction recorded in the central markets of Raigarh and Raipur, where prices fell by INR 1,700/t and INR 1,200/t, respectively. Buying activity remained subdued, leading to only need-based procurement amid weak finished steel demand across pan-India markets.

- Sponge iron prices continued to decline across all regions, falling by INR 200-1,300/t ($1–10/t) w-o-w, with the sharpest correction seen in the Durgapur region amid muted demand and limited enquiries. Manufacturers attempted to hold price levels; however, overall pressure in the market was driven by very few enquiries and the dominance of only need-based buying. Persistent weakness in finished steel demand kept procurement and trading activity subdued, maintaining a cautious sentiment. Traders also quoted lower-side offers in line with the soft market tone.

- On the export front, Indian DRI offers declined marginally, reflecting subdued overseas demand. Offers to Nepal eased by $4/t to $332/t CPT Raxaul, while Bangladesh-bound prices remained unchanged at $345/t CPT Benapole. Limited enquiries and cautious buying sentiment in export markets resulted in restricted trading activity, with deals concluded at comparatively lower price levels.

Finished long steel

- IF-rebar: Induction Furnace (IF) rebar trade prices declined across major markets this week amid subdued demand and cautious buying sentiment. Weak downstream demand and slower construction activity pressured market sentiment, prompting mills to lower their prices and offer discounts to support sales and clear inventories.

- Buying activity remained largely need-based, while slower fresh bookings led to inventory accumulation, with stock levels rising to around 10-12 days by early May.

- In the near term amid cautious buying activity and elevated inventory levels. However, seasonal pre-monsoon restocking may provide limited support to prices.

- On a week-on-week basis, rebar prices declined by INR 400-1,500 per tonne across key regions, with the sharpest drop observed in the Raipur market, according to BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 44,300-44,700/t exw Raipur, INR 48,200-48,700/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 46,400-46,800/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 44,500-45,000/t ex-Raipur.

- BF-rebar: In BF route rebar, prices declined by INR 500-1,000/t due to rising inventories and weak demand. Current trade level price in Mumbai is INR 59000-59500/t However, the market is expected to remain stable following increased construction activity after elections in five states.

Flat steel

-

- Leading Indian steelmakers have revised their mill list prices upward for early May 2026, raising both HRC and CRC prices by INR 1,000/t ($11/t). However, one mill has opted to roll over its prices, keeping them unchanged from the previous cycle.

- BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) increased by INR 900/t w-o-w to INR 58,700/t as of 08 May 2026, compared to INR 57,800/t on 01 May.

- Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 65,500/t, marking a w-o-w increase of INR 300/t from INR 65,200/t during the same period last week.

- The Mumbai market has witnessed an uptrend as mills have increased their price lists for early May, supported by expectations of tighter supply due to upcoming maintenance shutdowns.

- India’s bulk imports of HRCs touched 348,901 t as of 30 April, based on vessel line-up data. Around 1,60,146 t of additional cargoes are expected by mid-May.

- India’s bulk exports of HRCs touched 122,721 t as of 30 April.

- Indian HRC export activity remained subdued during 28 April–5 May 2026, with Europe and Middle East trade impacted by regulatory uncertainty, logistical disruptions, and geopolitical tensions. EU bookings stayed muted despite slightly higher offers, while Middle East trade remained constrained by shipping issues and regional tensions.

Leave a Reply