- Mid-grade coal records strong premiums

- Weak sponge iron margins pressure demand

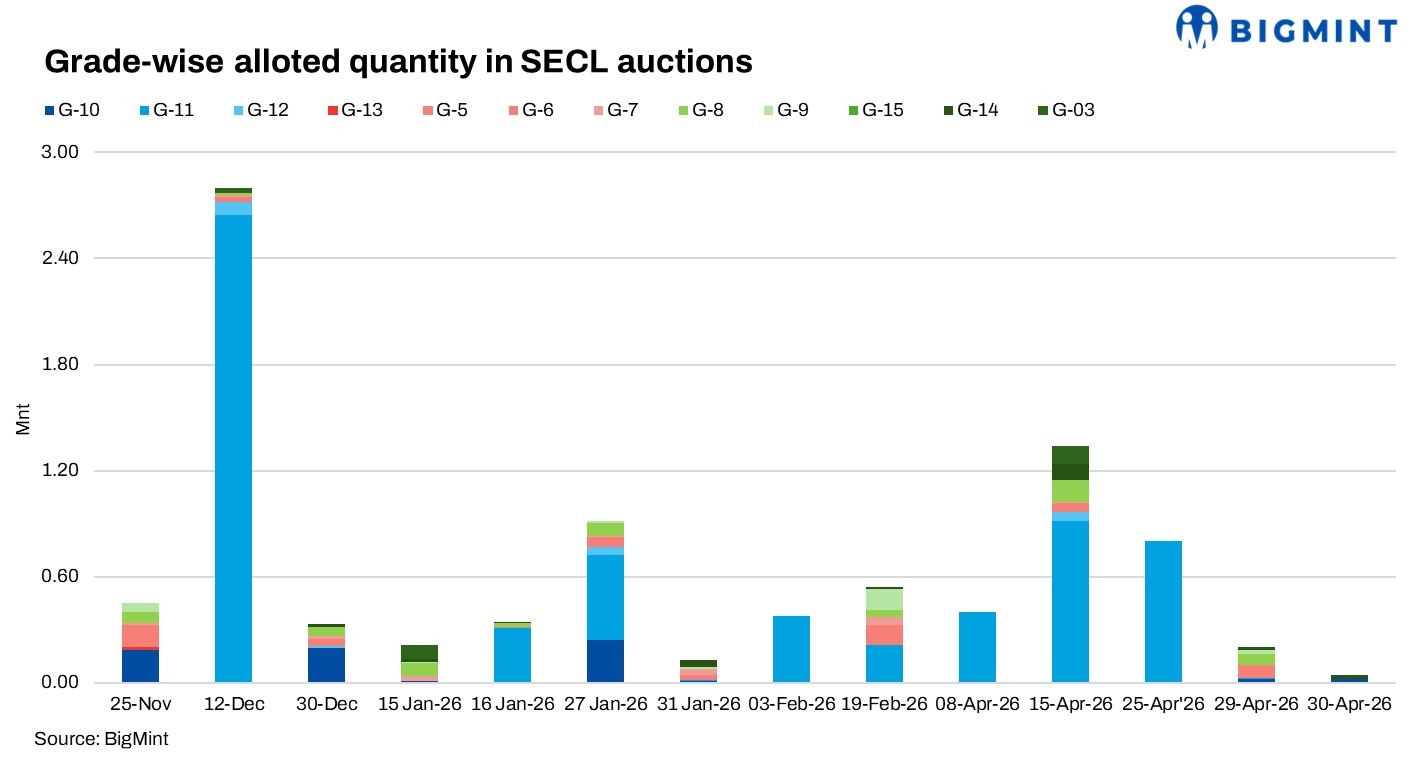

SECL’s recent non-coking coal auctions, conducted between 25 and 30 April 2026, reflected mixed market sentiment, with selective demand visible across mid-grade coal segments while lower-grade material witnessed relatively subdued participation. Buyers largely remained cautious amid weak sponge iron and steel demand, comfortable domestic coal availability, and liquidity pressure across industrial sectors.

25 Apr auction sees strong premiums for selective grades

In the 25 April auction, SECL allocated around 159,100 t across grades G4, G6, G8, G9, G11, and G15. G6 coal from Amera OC recorded one of the strongest responses, with winning prices averaging INR 5,795/t against a notified price of INR 2,761/t, translating into a premium of around 110%.

Similarly, G9 coal from Jagannathpur OC witnessed a premium of nearly 130%, with prices rising to INR 3,457/t against the notified price of INR 1,506/t. Vijay West UG G4 coal was booked at INR 5,065-5,105/t, reflecting a premium of around 55%. Meanwhile, G8 coal from Amagaon OC and Bangwar UG recorded premiums of around 73-76%, indicating relatively better participation in mid-grade non-coking coal.

Among buyers, Swastik Energy and Mineral Beneficiation emerged as the largest participant with 20,000 t allocations, followed by Agarwal Fuel Corporation with 18,900 t. Mivaan Steels, Arpa Fuel and Kalyani Minerals were also among the key buyers.

Bulk industrial demand dominates 29 Apr auction

The 29 April auction remained heavily dominated by G11 coal from Kusmunda OC, with around 804,000 t allocated in total against an offered quantity of 804,000 t, indicating complete absorption of the auctioned volume.

Winning prices averaged INR 1,741/t against the notified price of INR 1,184/t, resulting in a premium of around 47%. However, Gevra Road Siding material witnessed relatively weaker bidding, with premiums limited to around 20%.

Large industrial consumers dominated participation in this auction. Jindal Power secured 100,000 t, Bharat Aluminium booked 84,000 t, while Nu Vista, Vedanta Lanjigarh, and Param Mitter Ventures also secured sizeable volumes. The strong allocation reflected continued demand from power, aluminium, and cement sectors for lower-grade fuel coal amid stable industrial consumption.

Lower-grade coal sees muted participation in latest auction

In the 30 April auction, SECL allocated around 42,800 t against an offered quantity of 279,000 t, indicating relatively weaker participation and cautious buyer sentiment.

G10 coal from Jampali OC witnessed stronger bidding, with winning prices averaging around INR 2,930/t against the notified price of INR 1,360/t, reflecting a premium of nearly 115%. However, G14 coal from Baroud OC saw limited aggression, with premiums restricted to around 20%.

Singhal Steel and Power emerged as the largest buyer with 20,000 t allocation across G10 and G14 grades. Maruti Minerals, Singhal Steel Private Limited, Yuvraj Trading Company, and Shri Shyam Ispat were among other active participants.

Weak downstream market keeps sentiment cautious

Market participants indicated that despite selective strength in certain grades, overall buying sentiment remained cautious due to weak sponge iron margins and subdued steel demand. Requirement-based procurement continued to dominate market behaviour, while comfortable domestic coal availability restricted aggressive bidding across several auctions.

Participants also noted that buyers largely preferred selective grades offering better blending economics and operational flexibility. Lower-grade coal continued to face resistance amid subdued industrial activity and adequate inventory availability.

Outlook

SECL auction premiums are expected to remain largely stable in the near term amid cautious industrial demand and comfortable domestic coal availability. While selective grades may continue attracting stronger participation due to blending requirements, weaker sponge iron and steel market conditions may limit aggressive bidding across broader coal categories.

Leave a Reply