- Tight Pacific tonnage, active Australian enquiry support Panamax

- Weak thermal coal activity, ample Supramax supply weigh on Asia

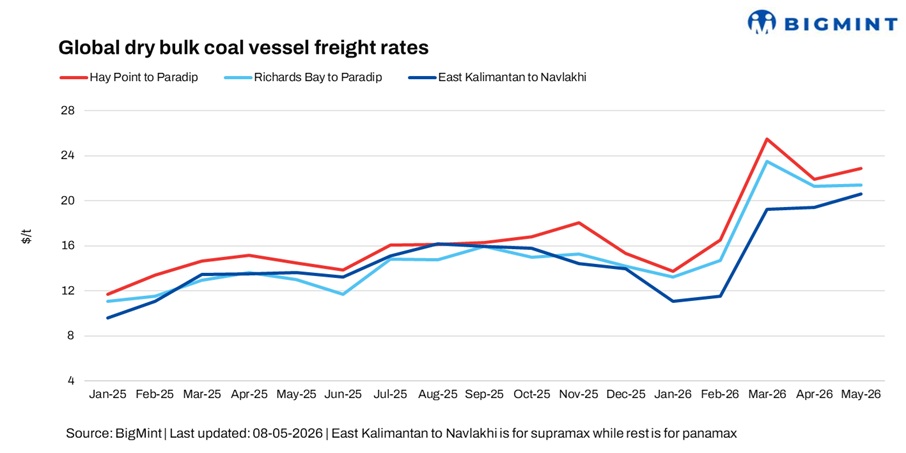

Dry bulk coal freight to India showed mixed trends in the week ended 8 May, with Panamax routes remaining firm across the Pacific and Atlantic basins, while Supramax routes stayed under pressure due to muted cargo activity and ample vessel supply in Asia. Market sentiment remained cautious, with selective fixing and uncertainty limiting stronger momentum.

“Market is uncertain. Bunker prices have again gone up,” mentioned a shipbroker highlighting growing cost pressure on freight markets.

In the Pacific, Panamax sentiment improved on tighter prompt vessel availability and stronger Australian mineral enquiry, with owners showing greater resistance on fresh discussions. Market participants noted that active Australian coal and mineral stems continued to support freight levels, although charterers remained cautious on higher ideas.

Meanwhile, the Supramax segment in Asia remained subdued amid slow post-holiday trading and oversupply of prompt vessels. Limited thermal coal cargo availability further restricted fresh fixing activity across Southeast Asian routes.

An Indonesian coal trader said, “Indo-India has started to firm a bit. There is enquiry but charterers are asking too low compared to owners’ ideas,” reflecting the gap between charterers’ bids and owners’ expectations.

Indicating selective participation in the spot market, another source added, “Thermal coal cargo activity remains limited, with only major players active in the market.”

Route-wise updates

Market highlights

- Bunker prices firm sharply w-o-w: Bunker prices rose by $48/t week-on-week to $827/t as of 8 May, up from $779/t a week earlier, supported by stronger crude oil trends and firm demand across major bunkering hubs.

- Brent crude futures decline sharply w-o-w: Brent crude oil (July 2026 contract) was last assessed at $100.78/bbl on 8 May, down by $10.03/bbl from $111.08/bbl a week earlier, amid weaker market sentiment and easing concerns over near-term supply tightness.

- Baltic index gains w-o-w: The Baltic Index surged by 348 points w-o-w to 3,034 as of 7 May, driven primarily by strong gains in the Panamax segment, which climbed 203 points to 2,195, while the Supramax index edged down marginally by 4 points to 1,521, reflecting mixed sentiment across vessel classes.

- DCE coke futures decline w-o-w: Coke futures on the Dalian Commodity Exchange fell by RMB 13/t ($1.91/t) week-on-week to RMB 1,828/t ($268.62/t) as of 8 May, reflecting slightly weaker market sentiment amid cautious trading activity.

Outlook

Coal freight to India is expected to remain mixed in the near term. Panamax routes are likely to stay supported by tighter prompt tonnage and steady Australian enquiry, while Supramax sentiment may remain under pressure due to ample vessel supply and limited thermal coal cargo movement across Asia.

Leave a Reply