- Imported offers strengthen amid global supply tightness

- Nickel volatility keeps buyers cautious this week

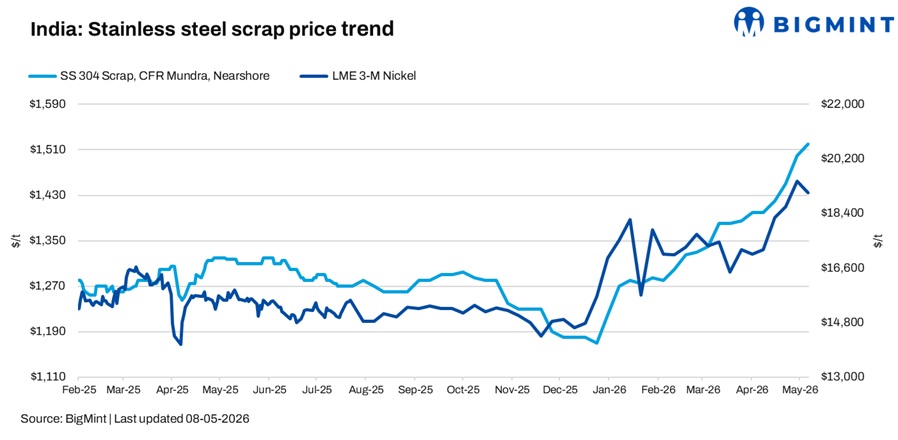

India’s stainless steel scrap market remained firm in the week ended 8 May, supported by tightening global availability, stronger import offers, and continued procurement interest from domestic mills. However, market sentiment turned cautious after London Metal Exchange (LME) nickel prices retreated from the $20,000/t mark touched earlier this week, prompting buyers to adopt a wait-and-watch approach towards the end of the week.

Domestic scrap availability remained limited across key trading hubs, while mills continued to actively secure material amid firm stainless steel production schedules. Market participants noted that bid-offer gaps widened during the week as suppliers held back inventories expecting further upside, whereas buyers resisted aggressive price hikes after nickel volatility increased.

On the other hand, 316 scrap availability remained tight in the market, amid higher molybdenum costs, moving offers higher side.

BigMint’s benchmark domestic 304-grade stainless steel scrap prices increased by INR 8,500/t week-on-week to INR 146,500/t DAP Delhi. Meanwhile, 316-grade scrap rose sharply by INR 8,000/t to INR 265,000/t, supported by higher alloy costs and limited market availability. Utensil scrap prices remained stable at INR 71,000/t, reflecting relatively balanced demand-supply conditions in the lower-grade segment.

Import offers also moved higher during the week amid firm international market sentiment and rising production costs globally. BigMint’s imported 304 scrap assessment increased by $20/t w-o-w to $1,520/t CFR Nhava Sheva, while 316 scrap rose by $35/t to $2,835/t. Prices for 201 and 430 grades remained unchanged at $730/t and $660/t, respectively.

Global insights

China’s stainless steel scrap market moved higher this week after the Labour Day holiday, supported by strong mill demand, firm stainless steel prices, and the continued cost advantage of scrap over high-grade nickel pig iron (NPI). East China 304 scrap off-cuts were assessed at RMB 10,800-10,900/t ($1587-1,602/t), while Foshan prices rose to RMB 10,450-10,750/t ($1,536-1,580/t). Market participants noted that healthy steel mill margins and elevated production schedules continued to support raw material procurement sentiment despite ongoing tax invoice constraints.

LME Nickel

On the raw material side, LME three-month nickel prices declined to around $19,070/t on 8 May, down 1.6% week-on-week from $19,385/t on 1 May, after touching a two-year high earlier in the week. Despite the correction, nickel sentiment remains supported by Indonesia’s mining quota cuts, revised HPM pricing mechanism, and elevated sulphur and freight costs, which continue to tighten global nickel supply expectations.

Outlook

India’s stainless steel scrap market is expected to remain firm in the near term, supported by tight domestic availability, elevated import offers, and sustained mill procurement. However, continued volatility in LME nickel prices and cautious downstream buying may restrict aggressive spot transactions. Market participants will closely track Indonesia’s nickel policy developments and global alloy price trends for further direction.

Leave a Reply