- Geopolitical disruptions support scrap container rates

- Tight containers, longer transit support overall sentiment

Container freight market for ferrous scrap imports into India remains firm overall, supported by extended transit times, reliance on transshipment services, and tight availability of heavy 20-ft containers amid ongoing Red Sea rerouting disruptions and continued logistical inefficiencies across global trade lanes.

A UK-based shipbroker informed BigMint, “UK-India container rates continue to remain firm, although availability at the lower end remains uncertain due to limited cargo movement from the UK to Chennai. Similarly, UK-JNPT rates are holding, but import activity into India remains subdued as competitive domestic prices continue to outweigh import viability. In contrast, demand into Pakistan, particularly Port Qasim, is reported to be relatively stronger.”

“Market sentiment remains firm, and rates are gradually ticking upward. Freight levels elevated due to longer transit times, tight availability of containers and rising oil prices due to ongoing geopolitical disruptions. It has also impacted overall transportation costs across the supply chain, highlighted a freight forwarder.

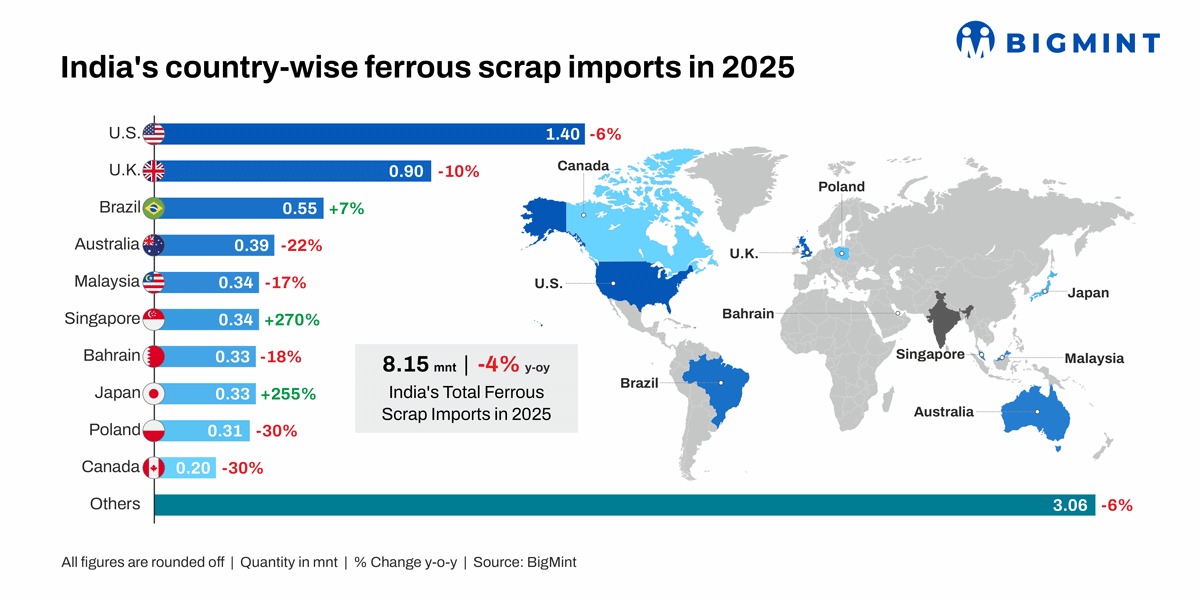

An Australia-based source informed, “Scrap bookings from Australia to India remain sluggish, as current costing levels are not commercially viable for buyers. Weak domestic scrap prices in India, compared to relatively better realisations in Far East markets, continue to limit import interest and slow booking activity.”

Route-wise updates

Why ferrous scrap container freights under pressure?

- Bunker prices rise amid geopolitical tension: Bunker prices stood at $827/t on 8 May, tracking the sharp rise in crude oil prices alongside firmer marine fuel demand, geopolitical disruption and tightening refinery margins.

- Red Sea disruptions, rerouting keep CFI firm: The Containerised Freight Index remained flat w-o-w at 1,911.40 points on 4 May 2026, with market sentiment staying firm amid Red Sea disruptions, elevated bunker prices, vessel rerouting, and tighter effective capacity due to longer transit times and port congestion.

- Transshipment routes continue to face delays: Transit times and freight dynamics are currently being shaped largely by vessel routing patterns. Direct services continue to offer relatively faster transit times, while transshipment-dependent routes are facing ongoing delays, congestion, and operational challenges.

Outlook

In the near term, freight rates are expected to remain firm to higher, supported by ongoing geopolitical disruptions, high carrier surcharges, and extended transit times. However, relatively lower domestic scrap prices may continue to weigh on import demand and keep buying activity selective.

Leave a Reply