- Mill inventories rise to 10-12 days from 8-10 days in Mar’26

- Billet, sponge iron prices decline, reducing cost support

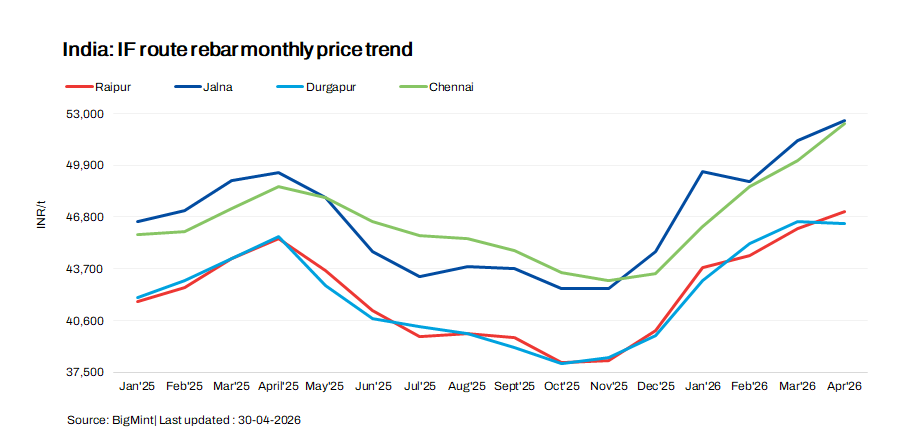

Induction furnace (IF)-route rebar prices decreased by INR 1,400-5,300/t m-o-m in April 2026 across regions, as per BigMint’s assessment. Market sentiment remained weak as buyers adopted a cautious stance following the US-Iran ceasefire announcement and resisted higher offers. Trading activity stayed largely subdued, with procurement limited to immediate requirements amid slow market movement. To support sales and sustain liquidity, mills offered discounts at elevated price levels.

Mill inventory levels increased to around 10-12 days, compared to 8-10 days in the previous month, indicating a buildup in stocks and reflecting weaker demand in the finished steel segment. Sluggish downstream bookings limited fresh orders, leading to slower offtake. Sellers primarily focused on executing earlier bookings, while new order inflows remained muted.

As per Joint Plant Committee (JPC) data, India’s rebar production through the IF and BF routes stood at 53.8 million tonnes (mnt) in FY’26, marking a significant 10% rise from around 49.1 mnt in the same period of FY’25.

Region-wise price movements

The northern region witnessed the steepest decline in April, with prices in Mandi Gobindgarh, Delhi, and Jaipur falling by INR 1,800-3,150/t. The downturn was primarily driven by extreme heatwave conditions and labour shortages amid the ongoing harvest season, which disrupted market operations and slowed construction activity.

In central India, prices in Raigarh and Raipur softened by INR 2,000-2,400/t during the month. Weak market sentiment and reduced material movement to other states continued to weigh on overall trade activity and prices.

Western India also recorded a notable correction, with prices in Mumbai, Ahmedabad, and Jalna declining by INR 3,900-5,300/t.The price gap between the central and western markets widened in April, with higher western market prices making material inflow from central and other eastern regions viable, thereby exerting downward pressure on prices. Meanwhile, persistently weak demand led to inventory accumulation in the western region, with stock levels rising to around 15-20 days, particularly in the Jalna market.

Similarly, the eastern region witnessed prices ease by INR 1,800-2,100/t in the Rourkela and Durgapur markets. The decline was mainly driven by election-related disruptions in West Bengal, along with liquidity constraints and logistical challenges, which continued to weigh on market sentiment and prices.

In south India, prices across Chennai, Hyderabad, and Bangalore declined by INR 1,500-3,700/t in April amid subdued, need-based demand. In Tamil Nadu, election-related uncertainty slowed project segment activity, while retail demand remained the primary market driver. Meanwhile, billet-to-rebar conversion spreads narrowed in both Hyderabad and Chennai during the month, reflecting weaker realisations. Additionally, inventory levels in Tamil Nadu rose by nearly 30-40% above normal levels, further pressuring prices.

Raw material price trends

The drop in finished steel prices was largely driven by lower prices of key raw materials — steel billets and sponge iron — used in IF-route rebar production.

Buyers remained cautious post-ceasefire and adopted a need-based procurement approach, as sufficient inventories built earlier reduced the urgency for fresh purchases. Consequently, trading activity and overall market sentiment remained subdued.

Considering Raipur as the benchmark, billet prices decreased by INR 300/t m-o-m to INR 42,150/t ex-works, while sponge iron (PDRI FeM 80% ±1) witnessed a sharper decline of INR 1,200/t m-o-m to INR 25,700/t ex-works.

BF rebar sentiment

Indian primary steelmakers have rolled over rebar list prices for early-May 2026 dispatches over end-April price tags, sources informed BigMint. Post-revision, list prices stood at INR 59,000-60,000/t on landed basis.

Trade-level BF-rebar prices (distributor to dealer) were stable w-o-w at INR 59,700/t exy-Mumbai, as per BigMint’s assessment on 1 May 2026. Buying interest remained weak last month in the trade channel, with buyers largely staying on the sidelines and restricting purchases to immediate requirements. Distribution channel participants reported comfortable inventory levels due to slower material offtake in recent days.

In the projects segment, prices hovered at around INR 58,500-59,500/t FOR basis. Demand remained weak with limited inquiries as buying slowed. Election-related labour shortages disrupted construction activity, delaying procurement. Buyers adopted a cautious stance amid price volatility and uncertainty.

Outlook

Rebar prices are likely to remain under pressure in May amid measured demand and inventory-led procurement. Market direction will largely hinge on supply-side dynamics, although pre-monsoon restocking activity may lend support to prevailing price levels.

Leave a Reply