- Market gains momentum post-holiday, buyers cautious

- Export realisations rise, domestic prices decline

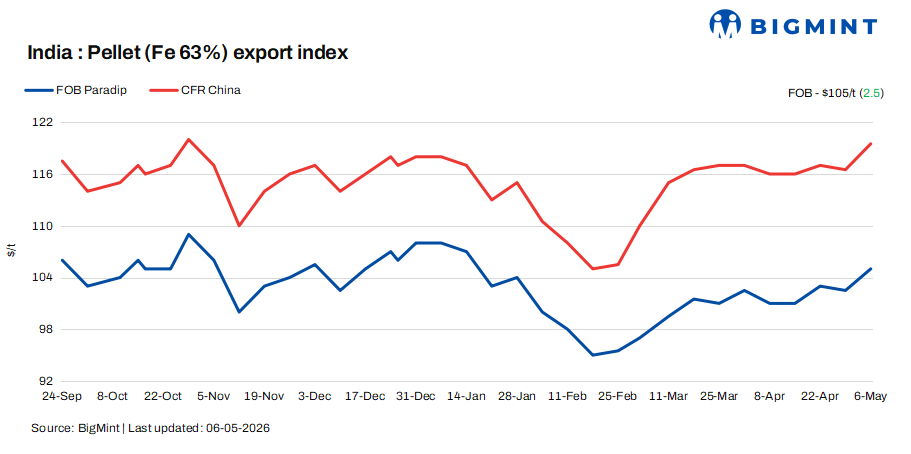

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index increased by $2.5/t w-o-w to $105/t FOB east coast on 6 May. Export market inquiries momentum as the Chinese market resumed post Labor Day holidays, but no transaction was reported in the seaborne market.

Sentiment remained positive backed by positive Chinese macroeconomic data, and expectations of healthy steel production levels in May. However, the overall tone remains slightly cautious with pellet inventories from 34 major ports standing at around 6.98 million tonnes (mnt).

Prices and trade update

No major export deals in pellets were observed in the market, as the market resumed shortly with buyers not yet fully operational after holidays. In contrast, some activity was observed in the domestic market, but it was relatively much weaker due to reduced domestic demand and the continuous drop in pellet prices.

According to sources, an east coast-based pellet producer scheduled a tender for their Fe 62.5% pellets, but the tender has not yet closed. This tender may provide clarity regarding the price fluctuations in the market.

Market updates

With markets reopening after the Chinese Labour Day holidays, sentiment has shown early signs of improvement. An international trader said, “Some optimism has crept back into the market, and we have started seeing a few fresh offers coming in after the holiday pause, indicating a gradual return of activity.”

Even so, market participation is still in the early stages of recovery. Another trader noted, “The market has just opened, and buyers are yet to return in full. We may start seeing bids or deal closures only after a couple of days, once participation improves and a clearer direction emerges.”

On the domestic front, pellet prices have continued to soften amid weak downstream demand, with buyers largely sticking to need-based procurement and avoiding aggressive stocking. In contrast, NMDC increased iron ore fines and lump prices by around INR 200-250/t across grades for May delivery. This is likely to push up input costs for pellet makers, which could gradually shift producer interest towards export markets in search of better realisations.

Notably, pellet exports have remained subdued over the past 2-3 weeks; however, a gradual pickup is expected as market activity normalises post-holidays. Overall, elevated iron ore and pellet inventories in China continue to keep buyers cautious, even as the market begins to regain some traction post-holiday.

Domestic vs export market

Export realisations (Fe 63%) were recorded at INR 7,750/t ($82/t) on 5 May, reflecting an improvement of INR 250/t ($2.5/t) w-o-w amid a wider spread between INR and USD. However, domestic realisations (Fe 62.5%) fell by INR 100/t ($3/t) w-o-w to INR 8,150/t ($87/t) exw. As a result, the spread between domestic and export prices stood at INR 400/t ($4/t), narrowing by INR 300/t ($3/t) w-o-w.

Rationale

- No confirmed deal from India’s east coast was recorded in this publishing window for T1 trade, and, therefore, this category was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Eleven (11) indicative prices were received, and nine (9) were considered for the calculation of the index and given a balance 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices edge up w-o-w: The benchmark iron ore fines Fe 61% index rose by $1/t w-o-w to $109/dmt CFR China on 5 May. Seaborne iron ore prices stayed rangebound as market participants awaited the return of Chinese buyers after the Labour Day break. Trading remained thin, but anticipated restocking and seasonal steel demand in May are expected to lend support, along with cost pressures stemming from volatile freight rates.

DCE iron ore futures prices remain firm w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2026 contract closed at RMB 812/t ($119/t) on 6 May, rising by around RMB 29/t ($4/t) w-o-w.

Vessel freights remain firm w-o-w: Iron ore freights stood firm w-o-w at $14.3/dmt on 5 May. From India to China, overall vessel availability remained tight.

Outlook

BigMint expects export prices to remain in a similar narrow range and market sentiment to improve gradually, with some deal closures likely over the coming week as buyers return. However, high inventories may keep gains limited in the near term.

Leave a Reply