- Stronger buying from China & Southeast Asia lifted m-o-m exports

- Weak developed market demand and high inventories limit growth

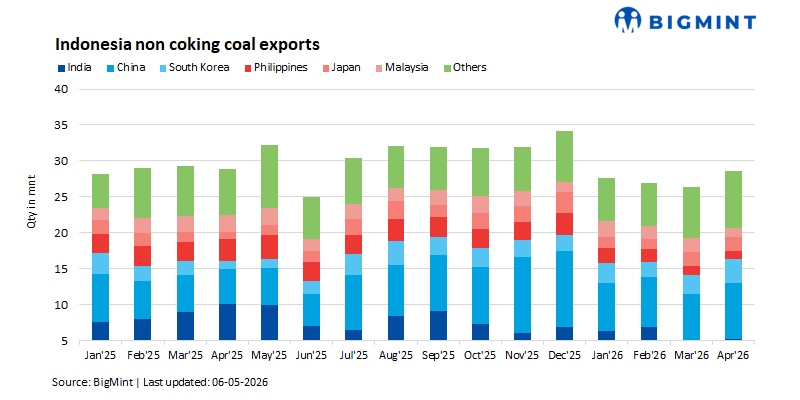

Indonesia’s non-coking coal exports recorded a moderate recovery in April 2026, increasing by 8.8% month-on-month to 28.63 million tonnes (mnt) from 26.31 mnt in March, as per BigMint data. Despite the sequential improvement, exports declined marginally by 0.9% year-on-year, indicating that global demand conditions remain largely stable but subdued.

The monthly uptick was primarily supported by improved procurement from key Asian markets and higher dispatches from major producing regions, while cautious buying persisted among some traditional importers due to adequate inventory levels and lingering market uncertainties.

Divergent demand trends across key importing markets

Demand dynamics across major destinations remained mixed during the month. China recorded a sharp 28.5% m-o-m increase in imports to 5.18 mnt, driven by steady utility demand and ongoing power sector requirements. India imported 7.87 mnt, up 5.9% m-o-m; however, volumes remained significantly lower by 21.4% y-o-y, reflecting moderated demand amid higher domestic coal availability and cost considerations.

Among Southeast Asian buyers, the Philippines and Malaysia posted increases of 24.4% and 3.1% m-o-m to 3.26 mnt and 1.97 mnt, respectively, supported by stable power generation demand.

Conversely, imports from developed Asian economies showed weakness. South Korea witnessed a 9.4% m-o-m decline to 1.15 mnt due to comfortable stock levels, while Japan saw a sharp 42.6% m-o-m drop to 1.17 mnt, although imports remained higher by 15.3% y-o-y, indicating reliance on long-term contracts rather than spot purchases. Meanwhile, shipments to other regions rose 14.6% m-o-m to 8.03 mnt, providing incremental support to overall export volumes.

Improved supply from key producing regions

On the supply side, Indonesia’s major coal-producing regions reported broadly positive trends. East Kalimantan recorded an 18.1% m-o-m increase in shipments to 13.57 mnt, maintaining its dominance as the primary supply hub, although slightly lower by 3.8% y-o-y.

South Kalimantan exports rose 3.3% m-o-m to 10 mnt, while Sumatra posted a 7.1% increase to 4.23 mnt, supported by steady demand for lower-calorific value coal. In contrast, North Kalimantan saw a sharp 29.7% m-o-m decline to 0.83 mnt, likely due to weaker offtake and potential operational constraints.

Mixed port performance reflects uneven logistics activity

Port-wise dispatch trends remained varied, reflecting uneven cargo movement across regions. Shipments from Taboneo declined by 12.4% m-o-m to 5.32 mnt, whereas Samarinda increased by 20.8% to 3.83 mnt, indicating improved loading activity.

Bunati recorded the strongest growth, surging 63.9% m-o-m to 3.72 mnt, while Balikpapan and Muara Pantai rose by 37.4% and 3.2% to 2.46 mnt and 1.63 mnt, respectively, supported by improved dispatch momentum.

Outlook: Stable exports with limited upside potential

Overall, the April rebound reflects a short-term improvement in demand, particularly from China and Southeast Asia, driven by power sector needs and the price competitiveness of Indonesian coal. However, persistent weakness in developed Asian markets, coupled with ample inventories and cautious procurement strategies, continues to constrain broader demand recovery. Going forward, Indonesia’s coal exports are expected to remain stable, with sustained demand for lower-CV coal supporting volumes, although significant growth may remain limited amid balanced supply conditions and conservative buying patterns across key importing regions.

Leave a Reply