- Trade-level HRC, CRC prices drop marginally w-o-w

- Mill maintenance shutdowns expected to tighten HRC supply

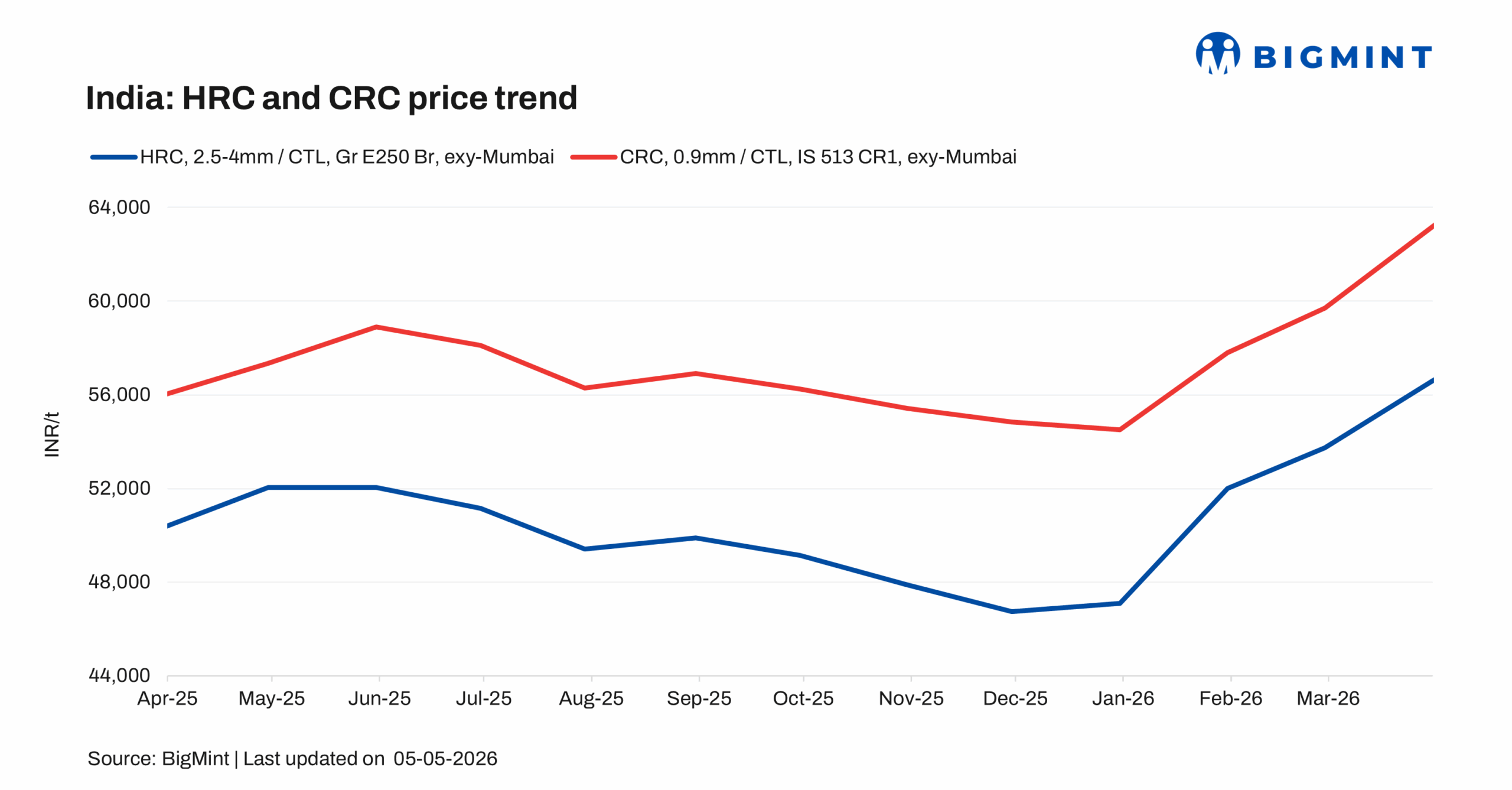

Leading Indian steelmakers have revised their mill list prices upward for early May 2026, raising both HRC and CRC prices by INR 1,000/t ($11/t). However, one mill has opted to roll over its prices, keeping them unchanged from the previous cycle.

HRC list prices (2.5-8 mm, IS2062, Gr E250 Br) are now in the range of INR 59,050-61,000/t ($620-$640/t), ex-Mumbai. CRC prices (0.9 mm, IS513 CR1) are listed at INR 66,400-68,750/t ($697-$722/t).

At the trade level, HRC prices rose INR 2,500/t ($26/t) m-o-m in April to INR 59,100/t ($621/t), up from INR 56,600/t ($594/t) in March. CRC prices posted an even sharper increase, surging by INR 3,300/t ($35/t) to INR 66,500/t ($699/t) from INR 63,200/t ($664/t) over the same period.

The price uptick is primarily driven by anticipation of scheduled maintenance shutdowns at key integrated steel mills across India. These planned outages are expected to temporarily constrain HRC production by approximately 10-15% in the near term. With supply tightening ahead of the maintenance window, mills have moved proactively to revise prices upward, seeking to manage order books and protect margins during the reduced-output phase.

W-o-w price assessment

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices inched down by INR 200/t ($2/t) w-o-w to INR 57,700/t ($606/t) on 5 May against INR 57,900/t ($608/t) as on 28 April.

CRC (IS513, Gr O, 0.9 mm/CTL) prices stood at INR 65,100/t ($684/t) down by INR 100/t ($1/t) w-o-w against INR 65,200/t ($685/t) in the same period last week. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Weekly market update

Trade-level sentiment in the Indian flat steel market remained largely subdued during the period under review, with tepid underlying demand continuing to weigh on both HRC and CRC segments. Compounding the cautious mood, a persistent labour shortage and a visible slowdown in construction activity further dampened buying interest, adding to the overall sense of restraint.

A market participant in north India informed BigMint, “Demand remains slow, with buyers refraining from fresh procurement and resisting the recently announced price hikes”.

Similar conditions were reported in the east, where a trader cited that the combination of ongoing elections and fragile market sentiment are the key factors dampening activity and slowing overall momentum.

Distributors reflected this cautious outlook, reporting minimal buying interest across the board. Although the latest round of price hike announcements has prompted a rise in offer levels in select markets, the demand-side picture remains unclear, leaving participants hesitant to commit to fresh purchases.

Additional updates

Import volumes: India’s bulk imports of HRCs touched 348,901 t as of 30 April, based on vessel line-up data. Around 1,60,146 t of additional cargoes are expected by mid-May.

Export volumes: India’s bulk exports of HRCs touched 122,721 t as of 30 April.

Outlook

Prices are expected to remain range-bound, with maintenance-driven supply tightness offering support while softening end-use demand caps any upside. Buying activity is likely to be driven by restocking needs rather than fresh consumption, keeping the market broadly balanced.

Leave a Reply