- Buyers limit purchases to immediate needs

- Ample supply intensifies seller competition

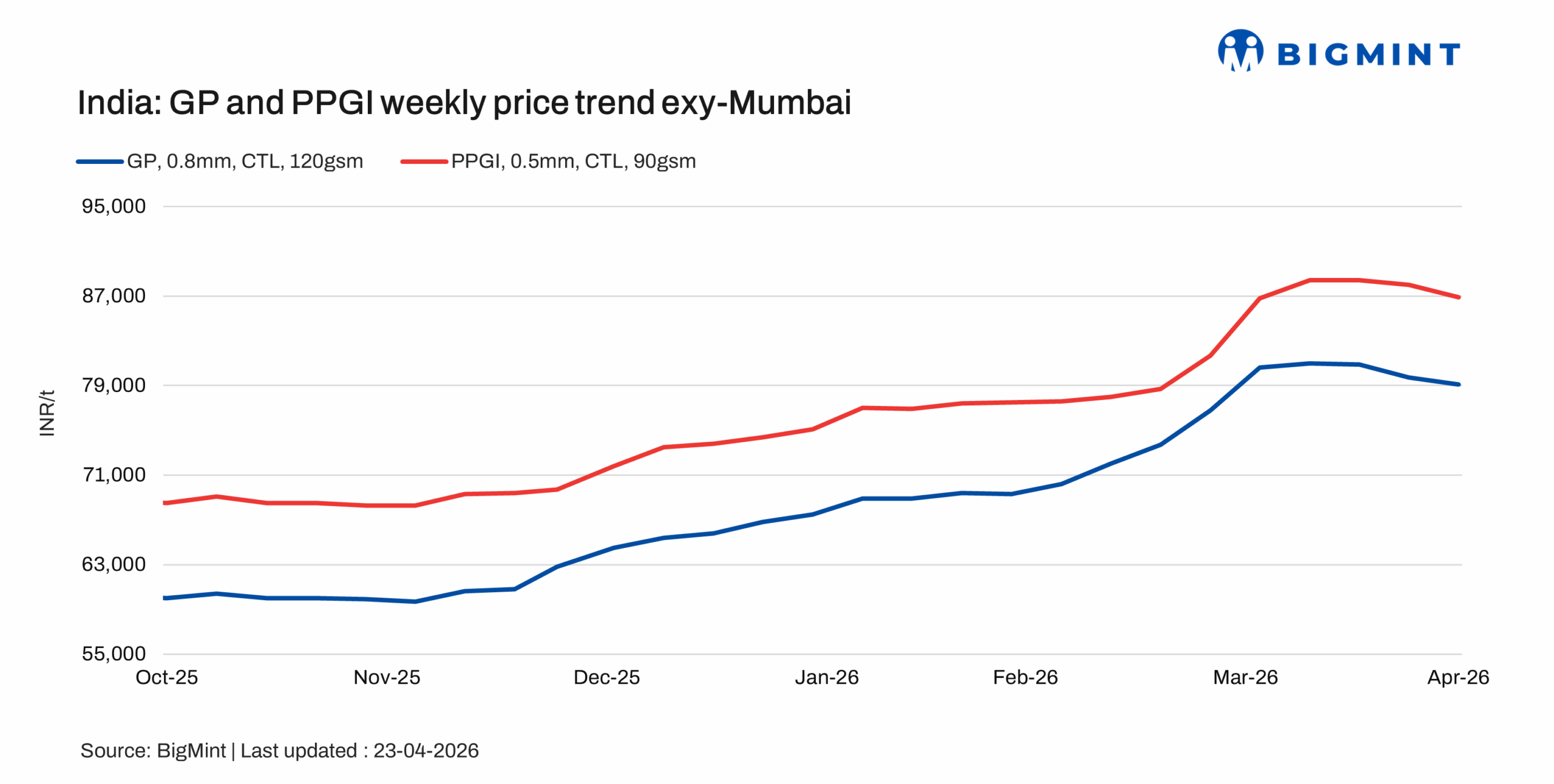

Indian coated flat steel prices (GP and PPGI) have declined by INR 500-1,000/t as of 30 April 2026, reflecting continued weakness in underlying market fundamentals. The downtrend is largely attributed to sluggish demand across key consuming regions, where buying activity has remained subdued. Market participants have adopted a cautious stance, leading to slower transaction volumes and increased price competition among traders.

Additionally, ample material availability in the spot market has further pressured prices, as sellers have been compelled to offer discounts to stimulate sales. Overall, the coated flat steel segment continues to face a soft demand environment, keeping prices on a downward trajectory.

Price updates

Galvanised plain (GP) coil (exy-Mumbai, India; 0.8mm / CTL, 120 GSM, IS 277) was assessed at INR 79,100/t on 30 April 2026, down by INR 600/t w-o-w. Tradable offer ranges were heard at INR 78,500-79,500/t, reflecting continued pressure on prices amid weak market conditions.

Pre-painted galvanised iron (PPGI) (exy-Mumbai, India; 0.5mm / CTL, 90 GSM, IS 14246) was assessed at INR 86,900/t, down by INR 1,100/t w-o-w. Market offers were reported in the range of INR 86,000-87,500/t, as mills adjusted prices in line with subdued demand trends.

Galvalume/bare galvalume (BGL) (exy-Mumbai, India; 0.5mm / CTL, 1220mm, AZ150) was assessed at INR 90,200/t ($967/t) on 30 April, remaining stable w-o-w. Offers were indicated in the range of INR 90,000–90,500/t.

Overall, coated flat steel prices witnessed a downward bias, with GP and PPGI declining during the week, while galvalume remained steady amid muted demand and cautious market sentiment.

Raw material prices

India’s zinc ingot (99.995%) prices increased by INR 3,000/t w-o-w to INR 353,000/t ex-Delhi on 29 April, supported by a recent producer price hike. The rise came despite muted downstream demand, which continued to limit stronger price momentum in the domestic market.

The uptick was primarily driven by a revision from Hindustan Zinc Limited (HZL), which raised its list prices by INR 7,700/t on 27 April, lending support to domestic sentiment. On the global front, three-month zinc futures on the London Metal Exchange (LME) trended lower during the latter half of the week, closing at $3,362/t on 28 April compared with $3,448/t on 21 April. However, a sharp decline in LME inventories to 98,225 t from 107,525 t over the same period provided some underlying support to prices.

On the substrate side, BigMint’s bi-weekly HRC benchmark (IS2062, Gr E250, 2.5–8 mm/CTL) declined by INR 1,000/t w-o-w to INR 57,900/t ($611/t) as of 28 April 2026, compared to INR 58,900/t ($622/t) on 21 April.

Similarly, CRC prices (IS513, Gr O, 0.9 mm/CTL) were assessed at INR 65,200/t ($689/t), down by INR 800/t w-o-w from INR 66,000/t ($697/t) in the previous assessment. Prices are assessed ex-Mumbai for the distributor-to-dealer segment, excluding 18% GST.

Market update

Market sentiment remained mixed during the week, with demand conditions showing limited clarity across regions, a decline in the last few days has introduced volatility in the market. Participants indicated that although demand is not severely weak, it continues to stay below normal levels, making any sustained price increase difficult in the near term.

Inventory levels remain comfortable to high across segments, with PPGI and PPGL stocks reported at over two months, while overall market inventories are estimated at around one month or higher. In other regions, demand is described as below normal but not at its weakest, supported by relatively tighter downstream supply in certain segments, which has helped maintain some level of offtake. However, HR and CR inventories are reported to be elevated, adding pressure on prices. With supply gradually getting restored, market participants remain uncertain about how long the current demand-supply balance will hold, keeping sentiment cautious.

Outlook:

The coated flat steel market is expected to remain under pressure in the near term, as the recent mill-led INR 1,000/t price increase has yet to translate into actual spot transactions, with a clear gap persisting between announced offers and executable deal levels, indicating limited buyer acceptance amid weak demand.

Over the coming weeks, market activity is likely to stay sentiment-driven, dominated by ongoing stock liquidation, cautious procurement, and competitive pricing, particularly given elevated inventory levels in PPGI/PPGL and ample spot availability. While mills may attempt to hold prices firm to establish a floor, a clearer market direction is likely to emerge through May as inventories gradually correct and buying interest stabilises; however, in the absence of a visible demand recovery across key consuming regions, spot prices may continue to face mild downward pressure despite mill efforts to support the market.

Leave a Reply