- Improve bids resulted in fixtures at elevated levels

- Healthy volumes and prompt vessels support rates

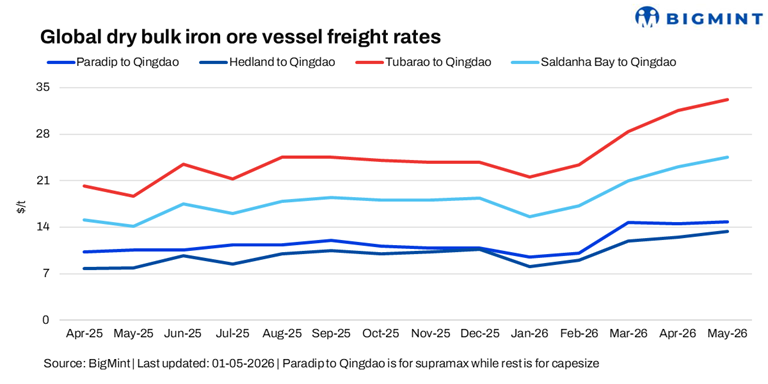

Dry bulk iron ore freight rates gained w-o-w supported by steady bulk cargo flows and relatively balanced tonnage availability. While cargo volumes remained healthy, charterers are showing measured fixing interest-partly due to near-term uncertainty and holiday-led caution-preventing any sharp spike in rates.

Capesize sentiment remained firm-to-positive, with freight rates trending higher despite subdued spot activity, as pre-holiday cargo coverage and limited prompt vessel availability supported market confidence. In the Pacific, thin trading and fewer fresh iron ore cargoes were offset by continued miner interest, keeping downside limited, while steady coal volumes added underlying support.

In the Atlantic, sentiment stayed cautiously firm, with South Atlantic rates inching higher on marginally improved bids ahead of the Labor Day break, even as North Atlantic demand remained relatively muted.

A shipbroker stated, “Sentiment remains on the softer side ahead of the upcoming May Day holidays, with charterers holding back on fresh cargoes in anticipation of weaker market activity and potential freight corrections in the near term.”

Route-wise updates

Market highlights

- Baltic index gain w-o-w: The Baltic Dry Index gained 13 points w-o-w to 2,686, driven by improved iron ore cargo activity in the Pacific supporting Capesize rates, alongside steady minor bulk demand lending support to Supramax sentiment, with Capesize up 12 points to 4,327 and Supramax rising by 3 points to 1,525.

- Brent crude futures gain w-o-w: Brent crude oil (July 2026 contract) was last assessed at $111.08/bbl on 1 May, gained by $6.5/bbl w-o-w, supported by heightened geopolitical tensions tightening supply expectations.

- Bunker prices increase w-o-w: Bunker prices increased by $16/t w-o-w to $779/t as of 1 May, supported by higher crude oil prices, firm refining margins, and sustained marine fuel demand ahead of holiday-related supply tightening.

- DCE iron ore futures surge w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) surged by around RMB 11.5/t ($1.7/t) w-o-w to RMB 796/t ($116.5/t) on 1 May, supported by improved steel demand expectations in China, restocking activity ahead of holidays, and resilient iron ore consumption from mills despite earlier market uncertainties.

Outlook

Iron ore freight is expected to remain firm in the near term, supported by steady Chinese demand and consistent cargo flow from major exporters, with post-holiday activity likely to improve fixing momentum. However, gains may be gradual as vessel availability increases slightly and charterers remain cautious, keeping the market stable with limited downside risk.

Leave a Reply