- Prices up on strong demand & tight supply

- Outlook firm, but upside limited by demand resistance

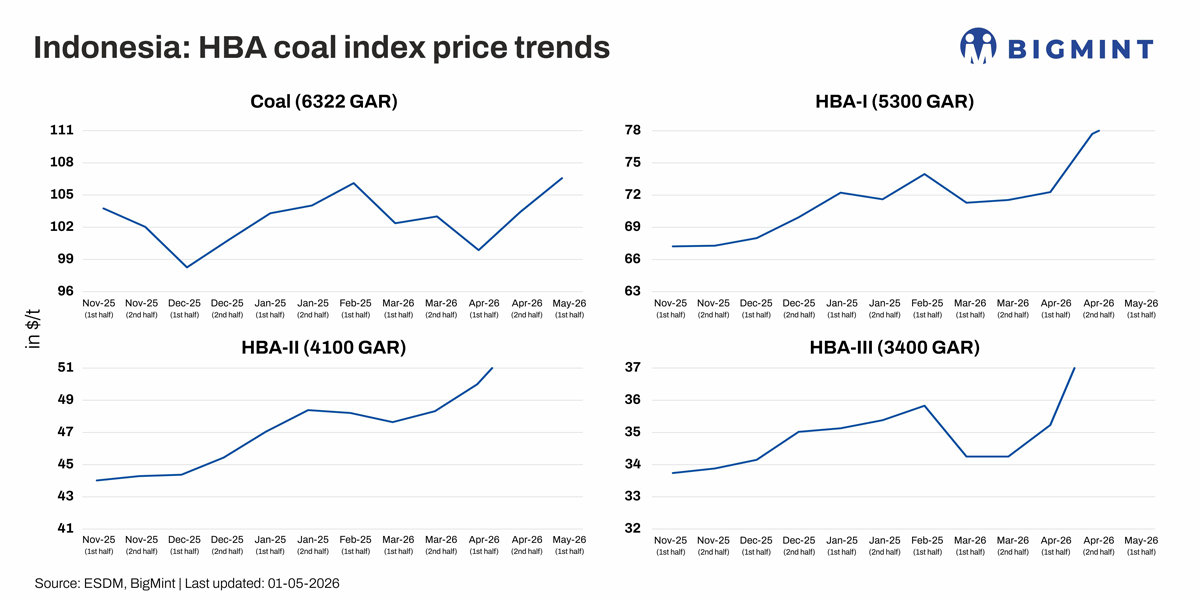

Indonesia’s Harga Batubara Acuan (HBA) thermal coal benchmarks for the first half of May 2026 moved higher across all calorific value (CV) segments. The uptick reflects strengthening international demand, constrained spot availability of Indonesian cargoes, and sustained procurement interest from key Asian importers ahead of the summer consumption cycle.

High-CV segment strengthens on utility-led demand

The HBA benchmark for 6,322 kcal/kg GAR coal increased by around 3% to $106.57/t for first half of May’26 as compared to second half of Apr’26, marking a six-month high. The rise was primarily driven by consistent offtake from power utilities across Asia, particularly in China and Southeast Asia, where higher-CV coal remains essential for efficient and stable baseload generation. In addition, firm international coal prices and relatively steady freight conditions lent support to higher benchmark realizations.

Mid-CV gains on balanced demand from cost-conscious buyers

The HBA-I index for 5,300 kcal/kg GAR coal rose by 2.4% to $79.56/t, returning to levels last seen in early May 2025. The increase reflects resilient demand from price-sensitive markets such as India and Vietnam, where mid-CV coal offers an optimal balance between cost and calorific efficiency. Limited availability of spot cargoes further tightened the market, exerting upward pressure on prices.

Lower-CV segment outperforms on supply tightness and affordability

Lower-calorific coal segments recorded relatively stronger gains during the period. The HBA-II benchmark for 4,100 kcal/kg GAR coal surged by 5.3% to $55.66/t, the highest since the index’s inception, supported by steady procurement from industrial users and smaller power producers across South and Southeast Asia.

Meanwhile, the HBA-III benchmark for 3,400 kcal/kg GAR coal edged up by 1.2% to $38.76/t, also reaching an all-time high, driven by robust demand from highly price-sensitive markets increasingly shifting towards lower-cost fuel alternatives.

Outlook

HBA benchmarks are expected to maintain a firm to mildly bullish trajectory in the near term, underpinned by peak summer demand across Asia, ongoing restocking by utilities, and continued tightness in spot Indonesian supply. However, the pace of further gains may be moderated by factors such as potential demand-side resistance at elevated price levels, weather-related shifts in power consumption, and any changes in Chinese import policies. Freight stability and currency movements will also remain key variables influencing price direction in the coming weeks.

Leave a Reply