- Mexico scrap market remains balanced with steady pricing

- European scrap prices firm on tight availability

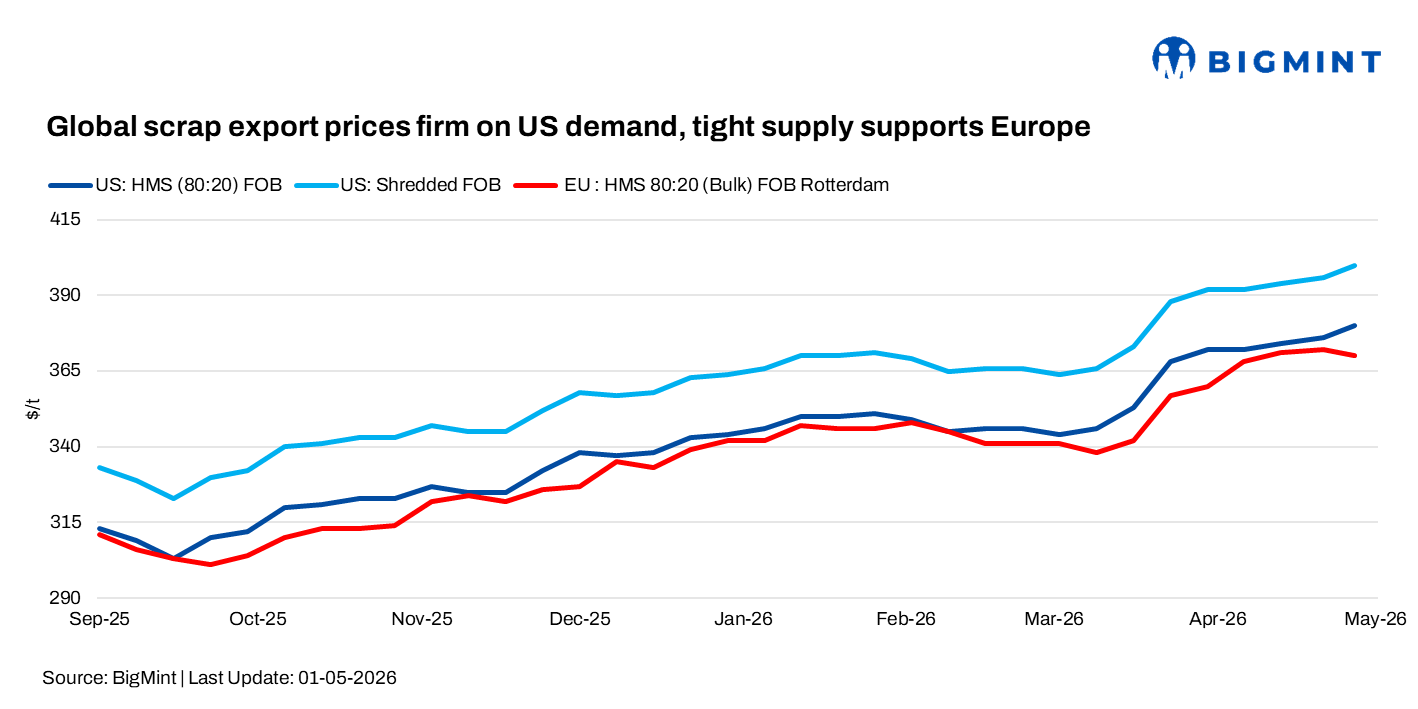

Global ferrous scrap export markets remained firm on 1 May, supported by tight supply and steady demand. The US market showed bullish sentiment, while export prices strengthened on improved Asian buying. Europe stayed supported by limited availability, though demand remained cautious, and Mexico’s market remained largely balanced.

US Ferrous scrap market sentiment turned bullish heading into May, supported by strong flat steel prices and higher mill utilisation rates. Prices remained largely stable w-o-w, with busheling at $445-450/t delivered, shredded at $430-435/t, and HMS near $380-385/t. High-grade scrap is expected to rise further on strong sheet mill demand.

In exports, deep-sea prices edged up, with US-origin HMS 80:20 at $405-410/t CFR and shredded at $415-418/t CFR. Vietnam bids near $405-408/t and Turkish imports around $412-413/t supported firm sentiment.

European Scrap prices remained largely firm during the week, supported by tight availability and steady export demand, though buying interest stayed mixed. UK/EU-origin HMS 80:20 offers to India were heard at $385-390/t CFR, with 3% impurity material near $380/t, while shredded scrap ranged at $420-425/t, reflecting cautious demand.

European suppliers raised offers to Pakistan, with shredded at $425-430/t CFR, though deals settled at $423-424/t. In Bangladesh, UK-origin PNS was offered near $440/t CFR, but buying interest remained weak due to impurity concerns.

According to market participant, “Europe, domestic prices remained firm, with Italian shredded scrap (E8) assessed at around EUR 345/t ($405/t) FOB, HMS 80:20 (E3) at EUR 310-330/t ($364-388/t) FOB, and HMS 90:10 (E2) near EUR 340/t ($399/t) FOB.”

Mexico’s the Northeast ferrous scrap market remained balanced in the week ended 1 May, with limited price movement as busheling held at MXN 7,600-7,800/t ($435-446/t) and HMS 90:10 edged up slightly to MXN 7,100-7,300/t ($406-418/t) FOB., reflecting tight supply. Sentiment stayed mixed, with expectations ranging from stability to a modest rebound in May. In the Bajio region, buying activity remained steady, with firm prices, though unclear demand signals kept overall sentiment cautious.

Outlook

Global scrap export markets are expected to stay firm, with US prices likely to edge up in May on strong mill utilisation and prime grade demand. European offers remain firm, but cautious buying may limit upside, while Mexico shows a slight upward bias.

Leave a Reply