- Scrap shortages lift prices across the region

- GST inspections disrupt supply chain operations

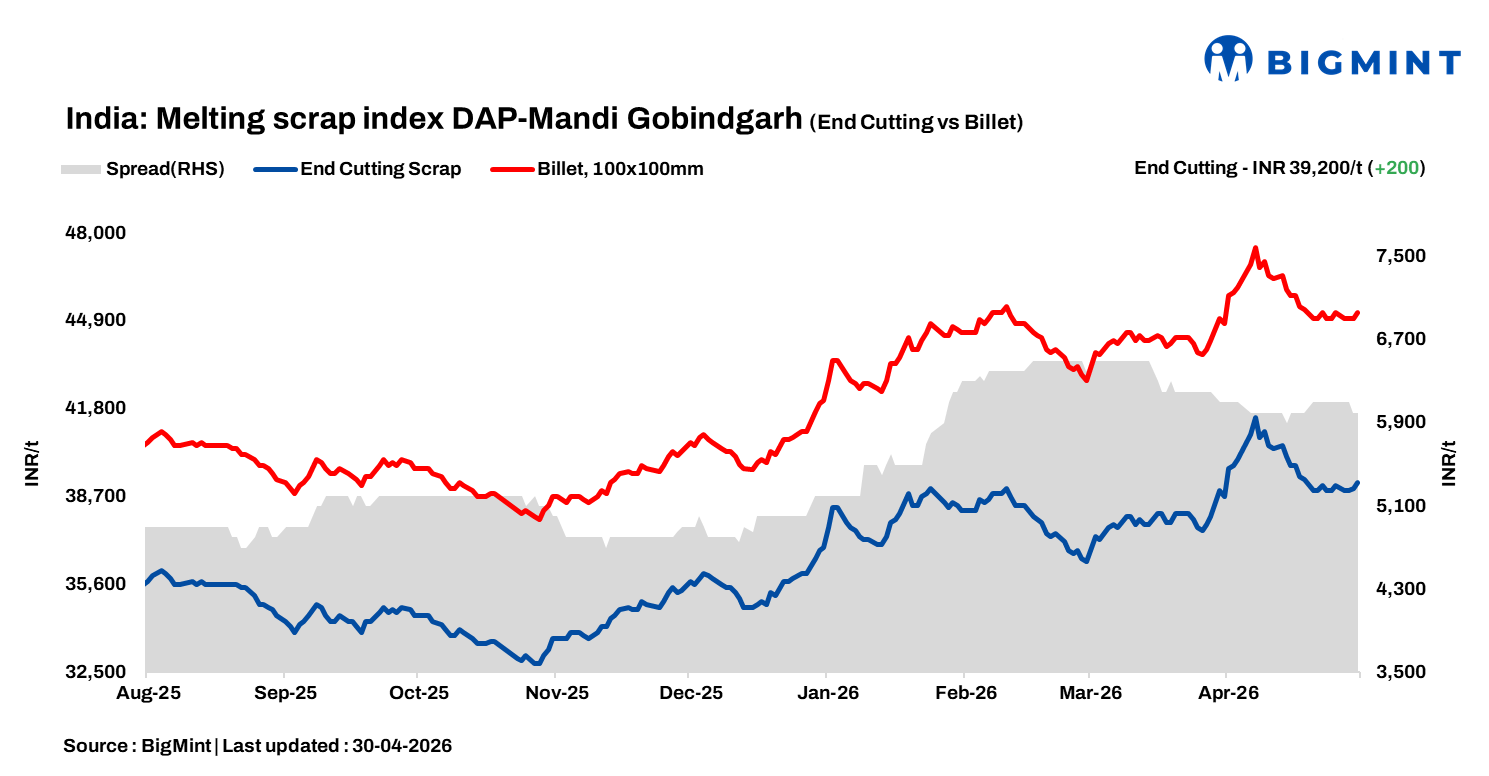

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, surged by INR 200/t d-o-d to INR 39,200/tonne (t) DAP on 30 April 2026. Scrap prices in Mandi increased by INR 200-300/t d-o-d due to slow arrival of scrap.

Mandi Gobindgarh, a key secondary steel hub, is grappling with multi-front disruptions as intensified GST inspections target major mills, with raids disturbing the routine trade flow in the region. However, steel ingot prices surged sharply amid tight supply conditions, while scrap arrivals slowed dramatically, exacerbating shortages across the hub.

Operational crises deepened with acute labour shortfalls halting loading and unloading, compounded by broader logistics breakdowns and an extreme heatwave forcing a halt in work during the afternoon session daily, rendering work impossible and stalling the supply chain further.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh remained stable at INR 32,900/t DAP, reflecting balanced demand-supply conditions. In contrast, steel-grade pig iron prices in Ludhiana increased by INR 300/t to INR 42,300/t DAP, supported by firm demand.

Steel market

In the Mandi region, steel ingot prices increased by INR 200/t to INR 45,200/t during the price reporting and normalisation phase. However, prices in other key markets rose INR 100-500/t.

Similarly, in the rebar (Fe500) segment, Mandi prices remained stable d-o-d at INR 50,100/t exw, supported by moderate demand. HR strip(patra) prices moved by INR 100/t to INR 46,800/t exw in the region.

Overview of Mumbai steel market

Rebar (Fe 500) prices on the Mumbai IF route remained largely stable today at around INR 49,500/t ex-works. Buying activity was low to moderate during the day, with procurement largely restricted to need-based requirements. Overall market participation remained limited, with only moderate enquiries reported.

Mill inventory levels have edged up slightly amid limited buying activity in the market. However, steady need-based procurement continues, and the absence of bulk bookings over the past few sessions has kept overall trade volumes moderate while mills focus on order execution.

On the raw material side, HMS (80:20) scrap was assessed at INR 35,000/t DAP, with the scrap-billet conversion spread hovering around INR 9,800/t.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,800-6,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $388/t, approximately INR 39,200/t (inclusive of freight). Today, HMS (80:20) prices in Mumbai fell by INR 200/t d-o-d to INR 35,000/t DAP. Indicative prices of shredded from Europe stood at $405/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 16,450/t.

To see BigMint’s melting scrap assessment, pricing methodology and specification documents, click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply