- Domestic met coke prices remain range-bound w-o-w

- Indian pig iron prices drop on weak market fundamentals

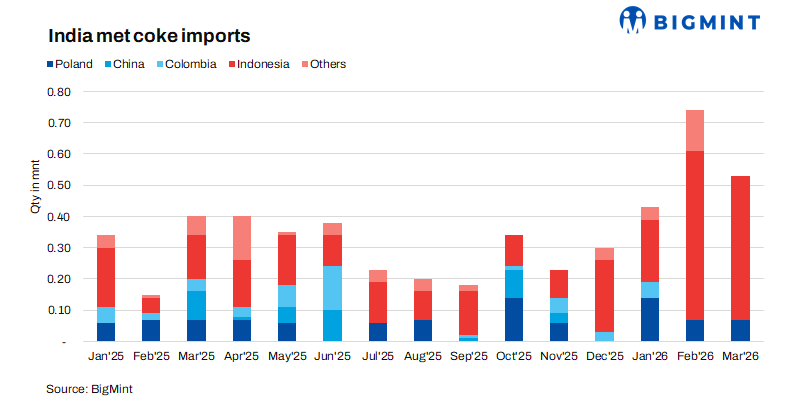

The Directorate General of Trade Remedies (DGTR) has recommended extending anti-dumping duties (ADD) on low-ash metallurgical coke imports for an additional five years. However, the proposed definitive duty range of $42.95-128.8/t is lower than the current provisional duties ($60.87-130.66/t), resulting in mixed market sentiment.

Following this, market participants indicate that Indonesian suppliers have already raised offers by around $10/t following expectations of reduced duties, alongside over 200,000 t of active enquiries are floating in market.

Import parity continues to anchor domestic coke prices. Indonesian-origin BF-grade coke (65/63 CSR) was assessed at $291/t CFR India, up $2/t w-o-w. This slight increase reinforces the domestic price floor and limits downside risks, even amid cautious demand conditions.

Domestic market scenario

India’s BF-grade metallurgical coke prices remained largely stable w-o-w as of 30 April 2026. Prices held steady at INR 36,400/t ex-Jajpur in the eastern region, while the western market saw a marginal decline of INR 200/t to INR 33,500/t ex-Gandhidham. Foundry-grade (+90 mm) coke prices were also unchanged at INR 36,400/t ex-Rajkot, indicating overall price stability across key markets.

Firm raw material cost dynamics

Upstream cost pressures remain supportive for coke prices. Australian premium hard coking coal (PHCC) prices were stable at $231/t FOB, while coal prices in China edged higher. Meanwhile, China’s coke market remained steady, with ongoing negotiations over a third round of price hikes. Stable supply, safety-related production controls, and pre-holiday restocking supported coking coal prices, maintaining a firm cost base for coke producers.

Mixed demand indicators

Demand-side signals remain somewhat mixed. While steel mills continue to operate at relatively high blast furnace utilisation levels, supporting coke consumption, steel-grade pig iron prices in Durgapur declined by INR 900/t w-o-w to INR 38,800/t ex-works. This indicates some softening in spot demand and margin pressures in the downstream steel segment.

Outlook

The Indian met coke market is expected to remain range-bound in the near term. Continued trade protection through ADD and firm import parity are likely to support prices, while stable raw material costs will prevent sharp corrections. However, any further reduction in duty levels or sustained weakness in downstream steel demand could exert mild downward pressure. Overall, prices are expected to move within a narrow band, with a slight downside bias in the short term, contingent on policy clarity and steel market trends.

Leave a Reply