- Indonesian cotton consumption projected to decline 5% in 2025-26

- Spinning mill utilisation subdued amid weak yarn offtake, rising costs

Indonesia’s cotton value chain continues to face demand-side stress, with spinning millers operating at reduced utilisation levels due to weak yarn offtake in both domestic and export markets. Despite stable macroeconomic indicators, the textile pipeline remains under pressure from cheaper imported fabrics and garments, including illegal used clothing inflows. This has continued to weigh on local yarn and fabric producers’ operations and has limited Indonesia’s lint imports.

The Ministry of Industry indicates that the textile sector, comprising over 4,100 units including around 150 spinning mills, is operating at 45-50% capacity, while cotton spinning millers are running even lower at 40-50%. This marks a decline from 57% utilisation seen in 2024, reflecting weak yarn demand and cautious procurement of raw cotton by mills.

Imports decline as mills shift to hand-to-mouth buying

Given Indonesia’s near-total reliance on imported lint, spinning millers have reduced cotton buying amid weaker yarn realisations and currency depreciation. Cotton imports are estimated to fall 2.9% to 1.92 million bales in 2025-26 and further ease to 1.9 million bales in 2026-27, reflecting lower mill consumption and higher carryover stocks.

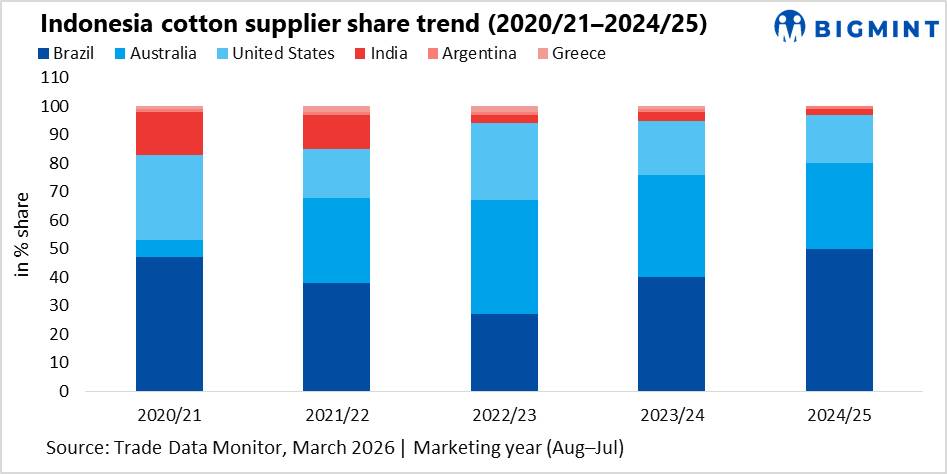

Brazil has emerged as the dominant supplier, capturing over 42% market share during August 2025-February 2026, supported by competitive pricing due to a larger crop. Australia follows with 35.6%, while the United States holds a smaller 12.6% share, partly impacted by longer shipment lead times extending up to 80 days, which affects mill procurement cycles.

Policy support offers limited relief to domestic spinners

To protect domestic spinning millers, Indonesia imposed a safeguard duty on cotton yarn imports starting October 2025, with levies beginning at IDR 7,500/kg in the first year. While this measure aims to curb cheap yarn imports and support local spinners, its impact remains gradual as demand recovery is still uneven.

At the same time, rising labour costs and a weakening rupiah — touching around 17,135 per US dollar in April 2026 — are increasing operating costs for spinning mills, further tightening margins across the value chain.

Trade flows shift amid global competition

Indonesia’s yarn exports rose 24.6% to 85,949 tonnes (t) in 2025, supported by currency depreciation and diversification into Asian markets such as China and Bangladesh. However, shipments to the United States declined sharply, indicating shifting trade flows amid tariff and demand pressures. Fabric exports also increased 18.8% to 8,562 t, led by Japan and regional buyers.

Outlook remains cautious for cotton trade

Indonesian cotton consumption is projected to decline 5% to 1.85 million bales in 2025-26 before a modest recovery to 1.9 million bales in 2026-27. While higher polyester prices and regulatory tightening may support cotton’s competitiveness, spinning millers are expected to continue operating conservatively, maintaining low inventory levels and buying on a need basis.

From an Indian trade perspective, subdued Indonesian demand and stronger competition from Brazil and Australia may limit export opportunities in the near term. However, any sustained recovery in mill utilisation or tightening of global cotton supply could reopen demand windows for Indian exporters, particularly in medium staple segments.

Leave a Reply