- Rising input costs, global producers’ hikes support prices

- BIS/QCO exemption raises import flexibility, slows flats demand

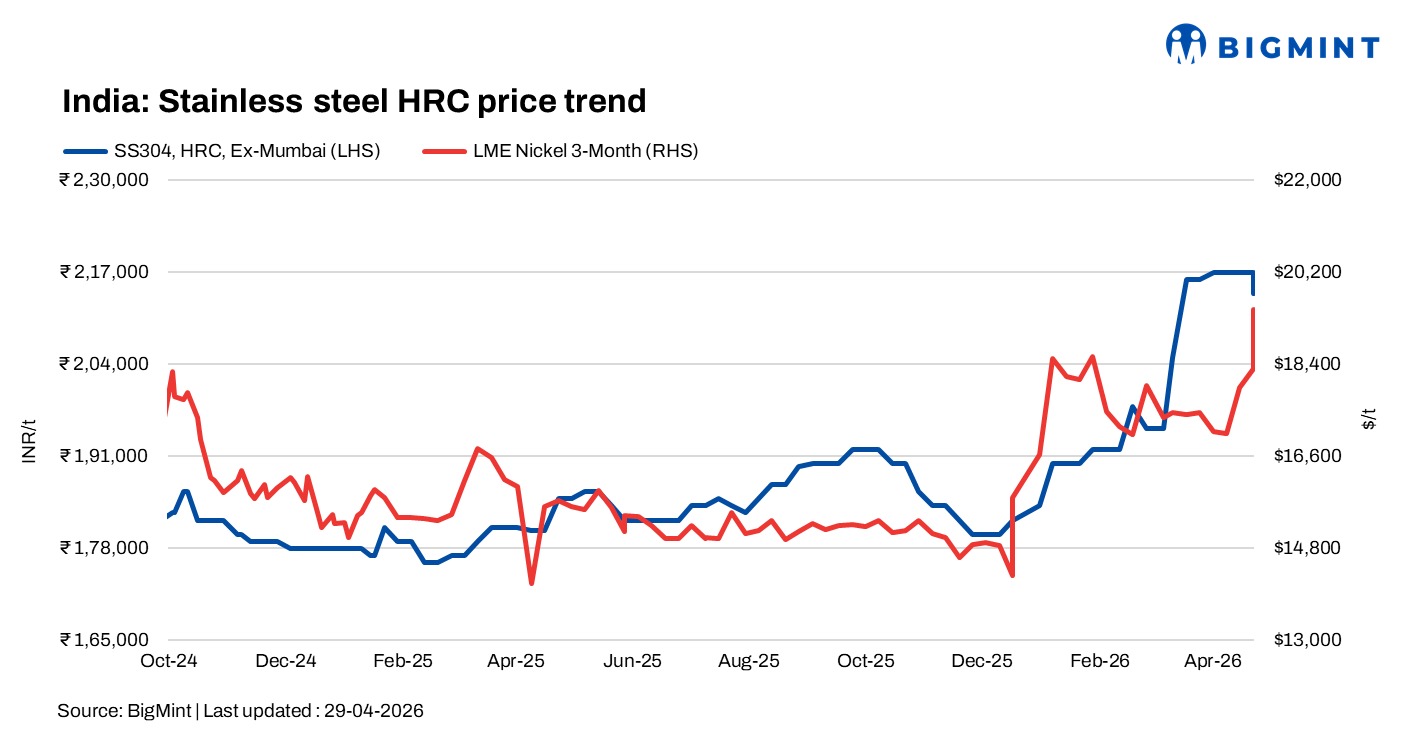

India’s stainless steel finished prices inched up w-o-w across most products on 29 April 2026 as elevated nickel and alloy costs continued to support market sentiment. This was despite cautious buying activity, especially in the 300-series segment, due to the easing of quality norms, which would allow import flexibility. At the same time, global stainless steel producers raised May surcharges, reflecting persistent cost pressures and broader uncertainty across international markets.

Benchmark nickel prices on the London Metal Exchange (LME) remained firm above key support levels, sustaining melt shop costs for stainless steel producers. Market participants noted that uncertainty surrounding Indonesian ore quotas and export policy continued to lend bullish support to nickel units. One trader said nickel may move beyond the $20,000/t mark if supply-side restrictions persist.

Finished flats face buyer resistance

BigMint’s benchmark 304-grade HRC prices declined by INR 3,000/t w-o-w to INR 214,000/t ex-Mumbai, while 316-grade HRC prices increased by INR 5,000/t to INR 375,000/t.

Demand for 300-series stainless steel remained slow as buyers resisted higher offers and delayed procurement, anticipating price corrections following the temporary exemption under QCO/BIS norms. However, some industry participants said the immediate impact on 300 and 400 series may remain limited, while the 200 series could face relatively higher pressure as previously restricted imports begin entering the market.

A market participant said the exemption allows sourcing from mills across multiple countries, improving procurement flexibility. However, it may also create downward pressure on domestic prices and increase the possibility of lower-preference material entering the market.

“No major market movement is expected until May, but buyers are closely watching import offers and currency trends,” the participant said.

Another participant noted that material that was earlier entering India indirectly through Middle Eastern routes is now likely to arrive directly after the BIS exemption, especially Japanese-origin cold-rolled coils, which could soften prices in the coming weeks.

Import offers for Chinese-origin JT HR were heard at around $1,110/t CFR, while JT CR offers were reported at $1,170/t CFR. After customs duty and additional expenses, landed costs remain elevated, limiting aggressive import-driven corrections.

A trader added that although some mills may reduce prices by INR 5,000-6,000/t, the broader market correction may remain limited to INR 2,000-3,000/t as domestic under-selling had already been taking place and global prices continue to rise sharply.

Long products supported by alloy costs

Finished longs remained firm, supported by higher alloy input costs and stable procurement from end-users.

BigMint’s benchmark assessment for 304L black round bars increased by INR 5,000/t to INR 190,000/t ex-Mumbai, while 316L black round bars also moved up by INR 5,000/t to INR 325,000/t ex-Mumbai.

Market participants said mills continued to maintain firm offers for longs as replacement costs remain elevated and alloy additions, particularly nickel and ferro molybdenum, continue to pressure production economics.

Raw material scenario

Outlook

BigMint expects Indian stainless steel prices to remain firm in the near term. While temporary BIS/QCO relief may increase import arrivals and cap gains in some flat grades, sustained alloy costs, firm nickel sentiment, and higher global mill surcharges are likely to keep overall market support intact.

Leave a Reply