- Imported zinc premiums under pressure amid weak buying interest

- Sellers cautious as galvanising demand remains sluggish

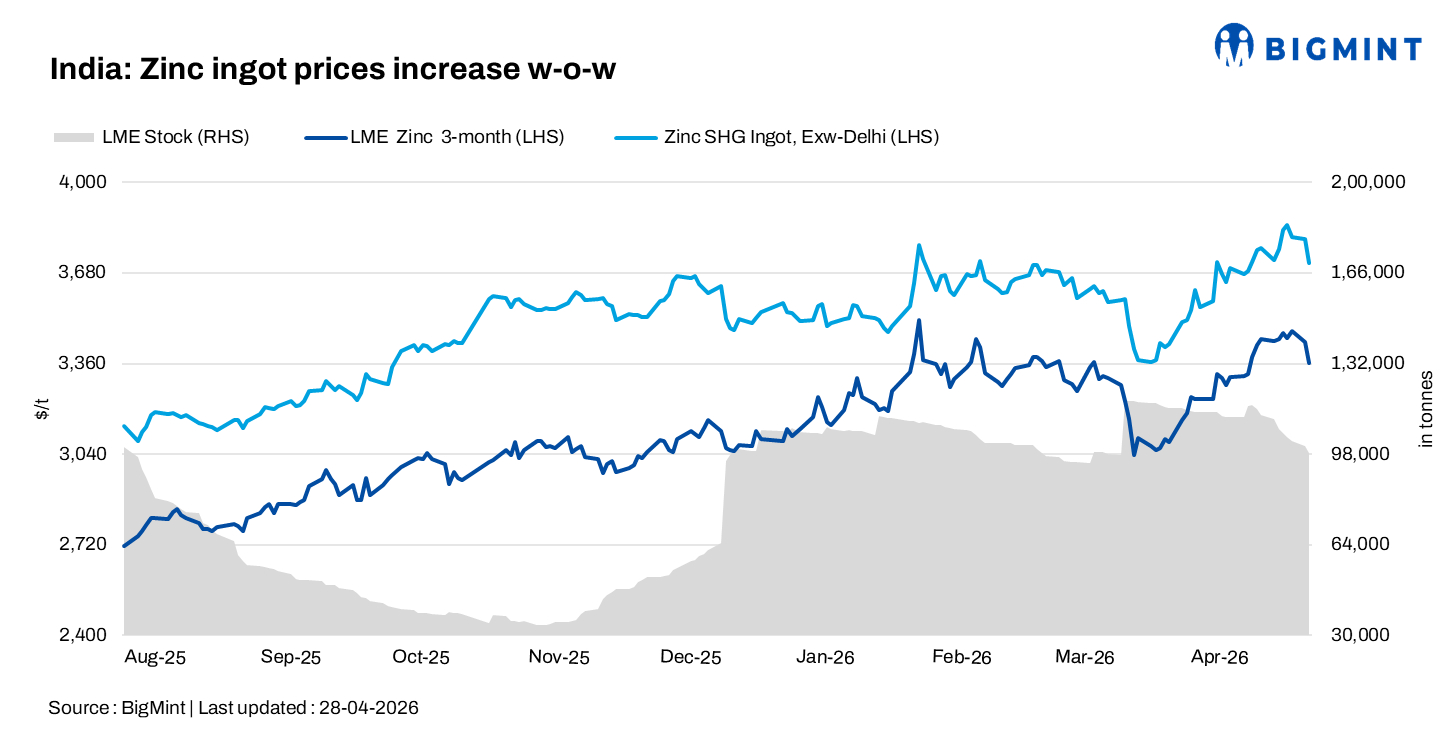

India’s zinc ingot (99.995%) prices increased by INR 3,000/t w-o-w to INR 353,000/t ex-Delhi on 29 April 2026, supported by a recent producer price hike despite muted downstream demand.

The uptick was primarily driven by a revision from Hindustan Zinc Limited (HZL), which raised prices by INR 7,700/t on 27 April, lending support to domestic sentiment.

On the global front, three-month zinc futures on the London Metal Exchange (LME) showed a declining trend during the latter half of the week, closing at $3,362/t on 28 April compared with $3,448/t on 21 April. Meanwhile, LME inventories dropped sharply to 98,225 t from 107,525 t over the same period, indicating continued drawdowns and offering some underlying support to prices.

Trading activity remains weak

Market activity remained largely subdued, with buyers continuing to procure material on a need-only basis amid weak galvanising demand.

Participants noted limited downstream activity, with sellers facing resistance in closing deals. Premiums in the import market were heard to be under pressure due to a lack of buying interest, with traders unwilling to offer aggressively at lower levels. However, some importers expect a gradual pickup in demand by mid-May.

Imported South Korea-origin SHG zinc (99.995%) was heard at $3,605-3,610/t CFR Nhava Sheva, though firm offers remained scarce. Australian-origin material was indicated at around INR 364,000-365,000/t ex-Delhi.

PMI deals were heard at approximately INR 320,000/t, reflecting continued price sensitivity among buyers.

Downstream alloy prices remained largely stable, with Zamak 3 at around INR 362,000/t and Zamak 5 at INR 369,000/t ex-works.

Coated steel prices decline

Meanwhile, India’s coated flat steel prices moved lower during the week, reflecting subdued demand conditions and cautious market sentiment.

Galvanised plain (GP) coil prices declined by INR 1,200/t w-o-w to INR 79,700/t ex-Mumbai, while PPGI prices edged down by INR 400/t to INR 88,000/t. Galvalume prices also softened by INR 200/t to INR 90,000/t.

The downtrend was driven by weak buying interest and adequate supply, although mills largely maintained pricing discipline. No firm export offers for HDGI were heard, reflecting muted overseas demand.

Outlook

Zinc prices are likely to remain largely stable in the coming week, supported by lower LME inventories and recent HZL price hikes, though weak downstream demand and soft import premiums may cap further upside.

Coated steel prices are expected to remain under pressure amid subdued consumption and sufficient supply, with demand recovery key to any price stabilisation.

Leave a Reply